Business

-

Beacon provides Debenture Trustee, Security Trustee, AIF Trustee, Trustee to ESOP, Securitization Trustee, Bond Trusteeship Services, Escrow Agent and associated services.

-

In AIF trustee they serve 200 out of the 1433 AIFs (~15% market share).

-

In Securities Trustee Beacon serves as custodian for syndicate loans mostly project financing to manage assets on behalf of lenders check covenants, exercise rights on behalf of lenders and in Securitization Trustee Beacon handles direct assignment of loans for CDOs/ loan pools of auto and micro finance acting as collection and payment agents (servicer) and maintain timely payouts.

-

In Debenture and Bond Trustee Beacon handles regulatory compliance, including filings with the ROC, SEBI, and stock exchanges to maintain transparency and track non-financial covenants outlined in transaction.

-

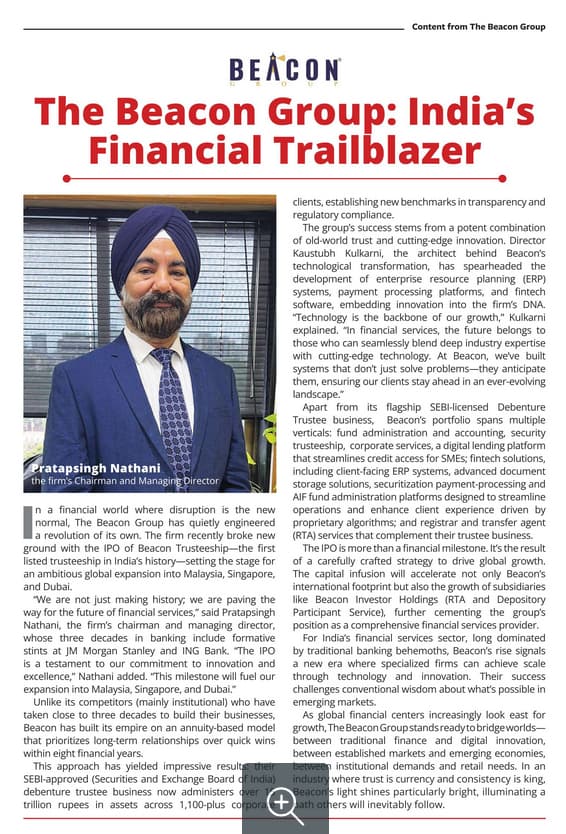

The company has very high quality management team, founder Pratapsingh Nathani launched the Loan Syndication franchise at JM Morgan Stanley, Post the JM-MS split, within JM Financial he was involved in marquee transactions in Leveraged Finance for an Auto ancillary & a large telecom tower company M&A Finance at JM Financial. he also ran the Loan Syndications & Debt Capital Markets at ING Vysya Bank. Other Board members and Senior management are from Axis Trustee and IDBI Trustee.

-

The Securities Trustee and Securitization Trustee business have grown very fast in the last 3 years (partially because of low base). There is trend among banks to outsource the monitoring of loans above 50 Cr. to these companies, this started 5-7 years back and has escalated in recent years.

-

Tailwinds like SEBI making it mandatory for large companies to have 25% of their fresh borrowing needs with a maturity of more than 1 year funded from the corporate bond and reduction in minimum investment size from 10 lakhs to 10K has helped the bond market grow.

-

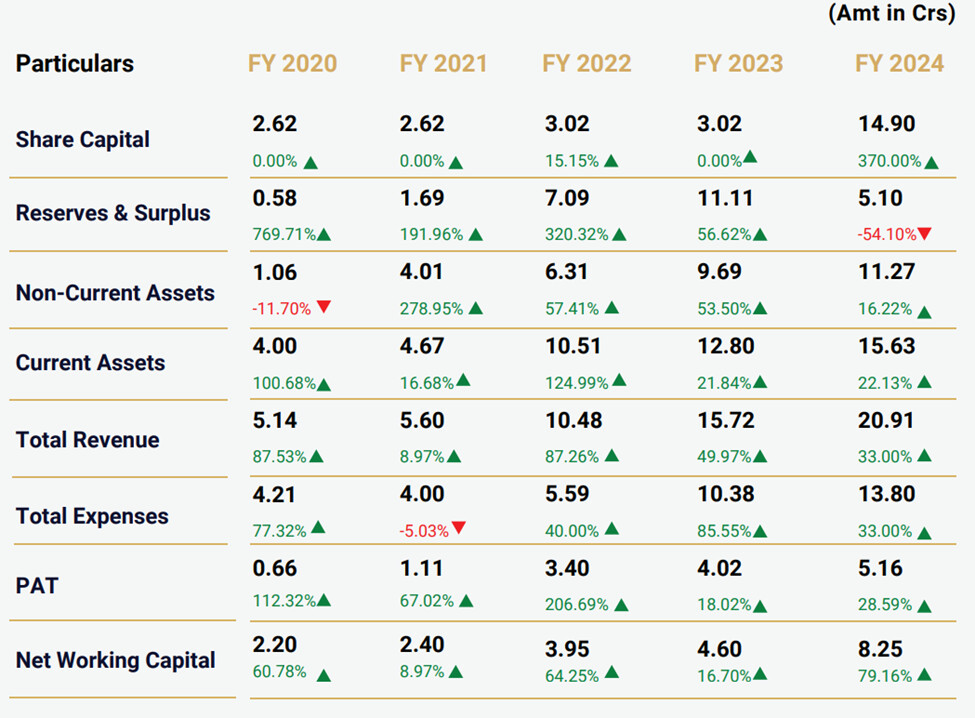

While the bank backed incumbents have been in this business for 30 years and reached to the stage of ~50 Cr. + top line, newer entrant like Orbis and Beacon have grow substantially well, Beacon has grown from 0 to 21 Cr. top line in last 9 years with last 4 years being profitable.

-

The clientele of Beacon includes PSU like IRFC, NTPC, Hudco, IREDA and Corporates like IIFL, Bank of Baroda, Nomura and Indiabulls.

-

It’s very like that the market is not very large and they might hit a ceiling after certain stage. The management is cognizant of this and is trying their hand on new avenues of growth for eg - Trustee Subsidiary in Mauritius and Dubai, applying for RTA and DP license to accompany the services currently provided, the management is also guiding that the share of non debenture and bond related business will become 75% from current ~40%.

-

Their pricing is on par in some cases a bit higher(~20%) than the competitors, they also provide software automation do fund accounting to gain more wallet share.

-

The industry leaders have 60%+ EBITDA margin and 40%+ PAT Margins, beacon could reach to this stage given they do not price their services at a discount and subsidise other business verticals from cash flow of trustee services.

Risks

-

SEBI has come up with a consultation paper where they want the regulated business like trustee for bond and AIF and non regulated businesses like securities trustee to be carved out in a separate entity.

-

The promoter have guided they will merge other business of the promoter group Kratos Fund Accounting and Beacon Payroll into the listed entity, Kratos had Revenues & PAT of 4 Cr and 76 lakhs respectively in FY 24, the promoters have multiple other business related to capital markets.