Background

BDH, set up in 1990, manufactures pharmaceutical formulations. Mr S C Kachhara, the Joint Managing Director, managing operations. Products include formulations for anticancer, antifungal, anti-malarial, and other treatment, in the form of tablets, capsules, injectables, and external preparations. Promoters hold around 55.4% stake in the company as on March 31 2018.

Business:

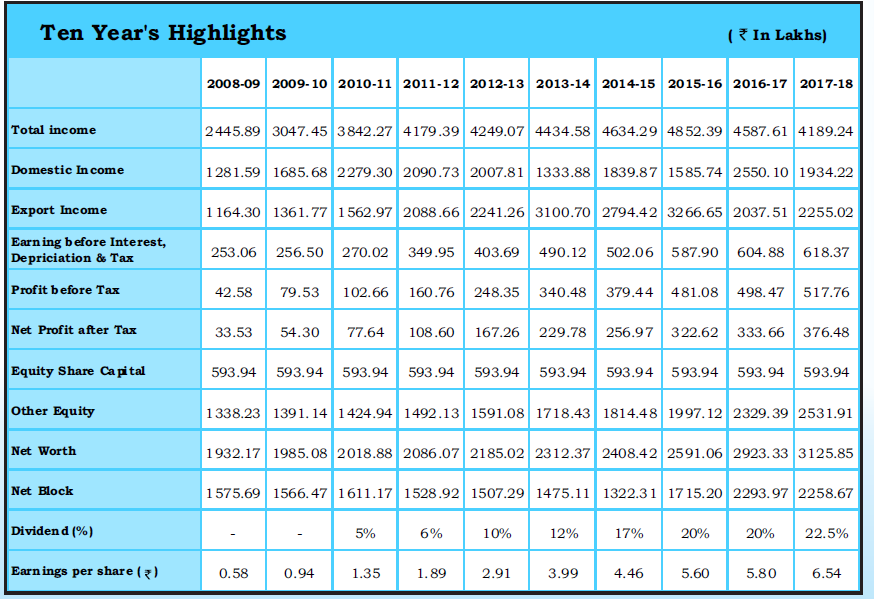

The company work as formulator for various pharmaceutical formulators. It supplies formualtors to various domestic large pharmaceutical companies and also work as contract manufacturer for Rest of World market (Non-regulated market excluding developed market like US/EU/UK). Over the period, the company had focus on improving margin which resulted in almost 10 fold jump in profit over decade with just doubling of turnover over same period. As per Crisil Rating rationale, IPCA account for 35% of revenue.

The company is recognized star export house. It has one formulation facility which has ISO certification and approved by WHO. As per discussion in AGM, the company is already utlising peak capacity in Kandivali unit.

Power business

The company has also spent around Rs 8 Cr on setting up two wind turbine of 0.8 MW each at Jaisalmer District in Rajasthan. The project was envisaged to provide IRR of around 14-15% with assumption of PPA at around Rs 5.50-6 per unit along with Tax benefit. However, there were some issue about PPA pricing and hence company is not able to generate any cash flow despite major capex. The management is currently exploring alternatives to utilise these assets productively. However, given the decline in tariff revenue, the power capex is unlikely to result in any significant profit for the company in my opinion.

Agro products

The company is also entered into agro products business. The planatations of cashew, mango and cocoanut grafts has been completed. The warehouse at Kudal, Sindhudurg district would be required after of couple of years when the crops would ready for harvesting. Hence, the company has been leasing out warehousing facility which is reported in lease rental in FY18 P&L account.

Financial analysis

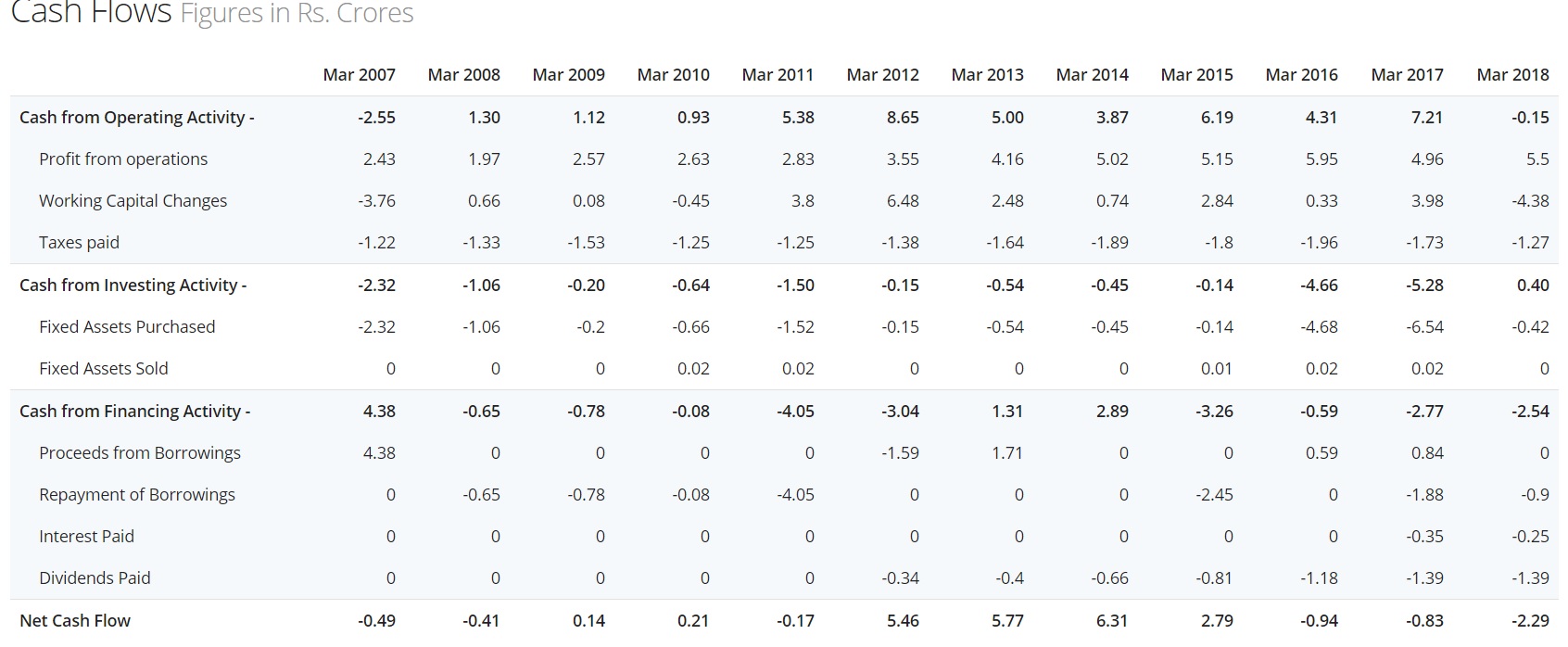

Despite small size, the company has managed to improved profitability and cash flow over a period.

The increased profit and positive cash flow assisted company to constantly improve dividend payment over decade which increased from nil in FY09 to Rs 2.25 per share during FY18 (almost 35% payout ratio).

Screener data for last 10 years:

https://www.screener.in/company/524828/

Credit rating rationale:

Future prospects

In the AGM held of Sep 25 2018, the management was asked to explain growth prospect and utilisation of cash and equivalent on balance sheet. The management said that they are considering capex of around Rs 100 Cr after 2-3 years. The current cashinvestment of around Rs 17 Cr (Net cash of Rs 10 Cr after adjusting Rs 7 Cr of working capital facility). The company intends to accumulate around Rs 25 Cr (from internal cash flow over next 2 years) and then would look at capex of around Rs 100 Cr. They are started searching for suitable location and would announce capex at appropriate time.

Till new facility is operational, the company would continue to operate from Kandivali Facility. However, there is limited scope for volume growth from Kandivali facility as same has reached peak capacity utilisation. Hence, for next 2-3 years, the revenue growth would be more from price growth and improving product mix.

Positives:

Moderate valuation: The company is trading at PE in single digit. Further, the management has been sharing cashflow with minority shareholder by way of distribution of dividend (payout ratio more than 30% over last 8 years).

Lower gearing: The management has managed well the growth in profit by prudent utilisation of existing facility and not allowed debt equity ratio to increase. Further, even for future planned capex, the management indicated that debt equity ratio would not exceed more than 1 times despite the capex.

Negatives:

Limited growth potential: Given that current capacity is fully utilised and past attempts of company in power and agro products are yet to contribute meaningfully to bottom-line, the growth would be primarily driven by superior product mix and price inflation. There is very limited scope for volume growth for the company till it start new facility.

Small size: The company is very small to undertake capex to move into bulk drugs as well as Developed market. The company intends to operate in Rest of World segment which is highly competitive. Further, as per Crisil Rating press release, the company has high dependence on Ipca with almost 35% sales. That would be major risk factor and would also limit margin expansion for the company in medium term.

Poor capital allocation: The recent capex in Power business (almost 8 Cr of Total Gross block Rs 35 Cr as on March 31 2018) has not resulted desired return. Further, the efforts in agro products would also yet to yield any meaningful contribution.

Catch 22 problem: The future capex of Rs 100 Cr (capex needed for new facility of minimum economy size) also appear very large in context to current operation and cashflows. Even after 25-30 Cr accumulation cash over next 2-3 years from internal generation, the balance Rs 70 Cr debt for capex may result in additional interest outflow of Rs 7 Cr (resulting cash loss at current cash profit of Rs 4.5 Cr during FY18). Hence, the company is facing major issue with growth. while growth would not come without capex, minimum capex of Rs 100 Cr has would put different set of challge on debt serivicability and cashflow given the small size.

Disclosure: I have very small tracking position in the company. The investor shall do its own due diligence before making any decision. I have attended AGM of the company and there is scope for miscommunication at my side in AGM. Investor shall take note of that limitation.