hi, is there any rerating on the cards for bayer crop science after resuming its ankaleshwar unit and selling off the surplus land at thane. awaiting ideas… thanks shailesh

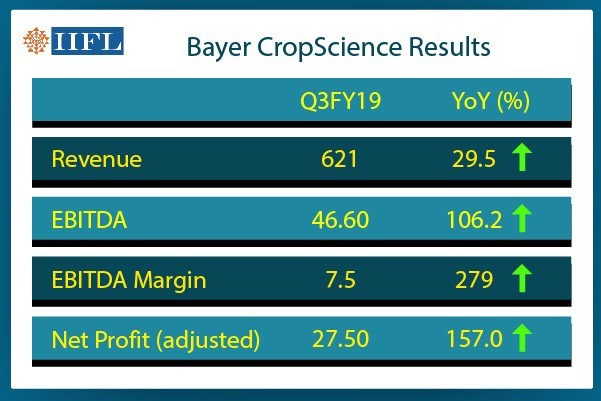

There is a 600% increase in EPS …NPM increased from 6% to 41%.

Can someone explain above numbers and its cause. Is there one time thing on balance sheet to justify it ?

Key AGM highlights by Capital Mkt

Higher sales of newer products together with increase in emphasis on exports are driving sales and profitability of the company. This phenomenon is expected to continue in coming years as well.

Management continues to remain optimistic about FY’15 as well, particularly in exports. Exports share of around 20% of total sales would remain in coming years.Launch of new products will continue in FY’15 as well.

Despite delayed monsoon and about 17% monsoon deficit than normal, due to higher MSP and higher irrigated lands, farmers are in better position and are ready to pay a premium for better agro chemicals and fertilizers. However a better monsoon generally makes company’s work easier.

Key highlights of AGM by Capital Mkt

Higher sales of newer products together with increase in emphasis on exports has resulted in a 15% growth in net sales and higher operating margin for FY’15.Exports is hovering around 18%-20% of total sales and management expects it to remain around that level, given the emphasis of Parent on domestic market.

Crop protection business will remain a challenge for FY’16. Given a back to back bad monsoon and lower MSP prices have weaken the sentiments of rural India. While the company through new products and higher penetration will see a growth in FY’16, it will be an overall difficult year for the company and the industry as well.

Seeds business (about 16% of total sales) has continued to do well for the company and so is for the industry. Management expects the seeds business to further do well in FY’16, given lower penetration in the market for organized seeds in India.Some farmers are ready to pay premium for agro chemicals and fertilizers, but generally, a better monsoon and sentiment helps in doing the job of company in a much easier way than in a bad sentiment and overall challenging condition.

Thankyou for the information. The Buyback by company at Rs 4000 speaks of confidence in business in times to come. Its a kind of stock you never want to sell.

Disc: - Invested 2 yrs back

Well i don’t think buyback has anything to do with confidence here in this case,as promoters will also participate in toto, like they had done in Dec 2013 @Rs:1580 ,even though,at that time mkt rate was higher.Hence majority of shares were tendered by them were accepted.

Came across an article on the Bayer Monsanto Merger Updates with the appointed date for the merger set at 1st April 2019.

INDIA MERGER UPDATES OF BAYER AND MONSANTO

1 Like

86% increase in Net profit in Q1,2021 for Bayer Crop Science - Monsanto Buy-out seems to have definitely boosted the performance of Bayer… Monsanto is the Seed specialist of the World and Bayer well known for its crop protection science along with Digital Farming and E-commerce channels has played out well.

Considering its parent Bayer, Germany holds 71.4% stake, Indian Govt’s Agri Push, buyout of the American seed company Monsanto, future only looks bright for this company.

Mr D. Narayan MD, CEO of Bayer crop science outlines the business prospects of his company:

(1) Importance of agriculture for food security

(2) Govt’s Priority for improving rural livelihoods

(3) The Govt has understood that Agriculture is going to be the backbone of Indian economy and the government’s transformational agri-reforms will provide farmers wider access to sell their produce beyond their local marketplaces and achieve better price realization.

(4) Bayer will continue to support Indian farmers through access to seeds & crop protection inputs, product innovation and crop advisory.

(5) Distribution channel through E-Commerce apart from traditional distribution partners

(6) Digital Farming

https://in.finance.yahoo.com/news/bayer-cropscience-advances-strong-q1-043600499.html

https://www.cropscience.bayer.com/innovations/data-science/digital-farming

2 Likes

An analytical report on Bayer Crop science from the brokerage house - Prabhudas Liladhar!

I have been trying hard to find as much information as I can about the firm, but surprisingly there are very few reports or sources available to read up on this firm.

It has a huge global vintage, is a debt free MNC, has decent ROCE, and the sales growth has been good in the recent past. Plus with the merger with Monsanto(which was a huge company by itself) effective FY20 onwards, growth should be good going forwards also. The Govt. is also focussing on the sector as well.

The drawback could be that this would be a seasonal business and a couple of low monsoons will impact the business(a lot?).

Will be grateful if people can share more insights or point me to a right information source. Thanks.

Yes, it is a MNC stock rarely discussed, analysed by anlysts…The promoters never appear in TV or media since they don’t need to raise capital or pledge their shares and their intention is not to jack up their stock price artificially… Attaching few links on Bayer crop science which may give you some insight … A lot of info is available in annual report of Fy2020 available in the net…

Agriculture drives the Rural Economy and Rural Economy accounts for 45% of our GDP…

And our Agriculture is monsoon dependent…if monsoon fails in a particular year , not only Bayer Crop, we have a dozens of very popular Agrochemical/ Seeds / Fertiliser stocks may not perform well - Rallis, PI, Bharat Rasayan, UPI, Excel now Sumitomo, Godrej Agrovet/ Astec life science, Dhanuka, Kaveri seeds, Coromandel,Tata Chemicals …list is endless …

It is not only the agro chemical/ seed/ fertilisers stocks there are many more sectors will also get indirectly affected if Rural economy gets affected …Tractors, 2 wheelers, Paints , FMCG, Rural Focus NBFC and banks who lend rural farmers…

Why agriculture - there are many business/sectors which are Cyclical and Seasonal … Cement, metal, consumer Durables , Automobiles… the only exception perhaps is the Pharma exports and IT exports…that too again both may carry a lot of regulatory risks…

Once upon a time, all analysts advised to invest in PVT sector banks and NBFC like Bajaj finance as it was believed that these were secular growth Stories…now though we find a lot of headwinds … we say if you believe India has to grow, finance and bank stocks can not be ignored…

Similarly, if India has to grow , Agriculture and rural economy can not be just ignored as it accounts for 45% of GDP…

Therefore , equity investment is always advised for long terms in fundamentally sound stocks for years together to get the best returns averaging out of ups and downs of the business cycle… … Or else one needs to be a smart trader to make money who could enter and exit on or before Quarter QoQ results or expecting a tailwind or head wind which keeps changing …

Discl: invested for long term…may be biased… please apply due diligence before buying …

3 Likes

Thanks for the reply. Had already gone through the annual reports from their website, will go through the remaining links.

Thanks again.

Bayer is no longer a standalone Agro-chem company…

With Monsanto in its portfolio, It is an integrated Agri Company which deals with not only crops protection , but also deals with the entire range of seeds for crops and vegetables , fruits…

So there would be demand for its products throughout the whole year…

https://www.cropscience.bayer.in/en/Products-H/Brands/Seeds-and-Traits/Seed-Seminis-Vegetables.aspx

While the company name indicates that it deals with Crop science , they are also into professional Pest control including mosquitoes and vector Management for house holds, commercial establishments , plants , offices, Groceries stores etc…

https://www.cropscience.bayer.in/Products-H/Pest-Management.aspx

4 Likes

Bayer Crop Science Reports 35% jump in Net profit in Q2 2021 YOY.

1 Like

Bayer is giving opportunity now and on every declines. This space will get rerated on any agri reforms.

What’s the rationale to support the enthusiasm?

Hi

While I hold a similar positive view on Bayer Crop Science (BCSL), I have to admit it is difficult to find strong data to justify this. A couple of comments from my side from a fundamental analysis perspective that may add to your thinking

-

BCSL financials are a little muddled due to the following - merger with Monsanto implies only the results from FY20 onwards is relevant (financials before that not directly comparable), large one-off disputed tax settlement of ~Rs 127 crores in FY21 (Q3) has depressed FY21 EPS by approx Rs 13, special dividend of Rs 125 seems to be propping up the dividend yield

-

Looking at historical valuations - relative valuations (PE) seem below long term averages and my bottom-up valuation (read next point for conviction in valuation) at a 15% discount rate is ~Rs 4500 - so there seems to be some valuation comfort (definitely on the relative valuation - although the PE is quite high for the business growth even though the E might be relatively low today for points mentioned above). Overall business theses is as you say - large MNC - so governance, no debt, leader in crop protection - potential upside as agri industry opens up

-

The big challenge is there is very little visibility on the business evolution (and I am not sure I have the best capability to understand the underlying business). The level of disclosure from the company is not great - the most recent investor pack gives a high level break-up of revenues between crop protection and seeds (I could not even find this in the annual report) and they held an investor call (not sure if this is a new phenomenon but I had to request an invite for this). While they highlighted the challenge in the current quarter being around the seeds business (corn specifically), the plan to get out of this funk is not really clear. The crop protection business seems to be doing fine (and is now 85% of revenues). Hence the confidence in the bottom up valuation is quite limited (as it is just the output of some conservative revenue and margin numbers in Excel). The have very broadly articulated their strategy of focusing on small-holder farmers (Better Life Farming ecosystem) - but can’t say they clearly articulate how this translates into revenues / margins

-

As a disclosure, I am invested in BCSL and have fully sized my position (is ~5% at invested value - so non-trivial). I have had to bend several of my own rules to get here given that I am trusting the management without necessarily having the insight into the underlying business. I see it as a relatively low risk part of my portfolio (so don’t expect multi-bagger growth on this). Upsides possibly exist if there is a general uplift to the agri economy (and therefore greater willingness to use better quality input), and having access to a broad global portfolio of products - but difficult to put numbers on this.

Would also welcome any view on the business insight and possible evolution.

2 Likes

Their pharma / healthcare business in west is competitive. Is there any unlisted pharma entity in India? or is there any strategy to bring healthcare business to India?

Note: I have only tracking qty