Fine tune my investment strategy along with boarders

Disclosure of my holdings

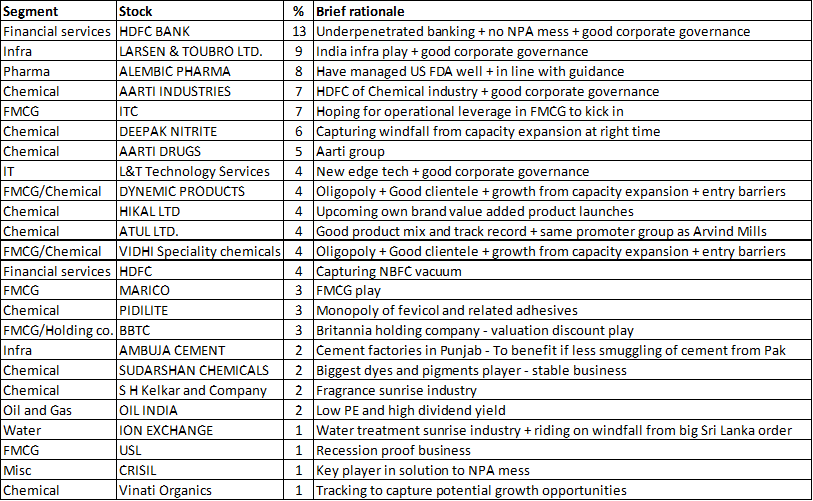

Portfolio theme is to capture good quality companies across Large+Mid+Small cap space. Special focus on corporate governance. Companies having growth triggers in near future are of interest. Try to add/reduce weightage as stock price becomes cheaper/expensive or accumulate in SIP-like mode if rangebound.

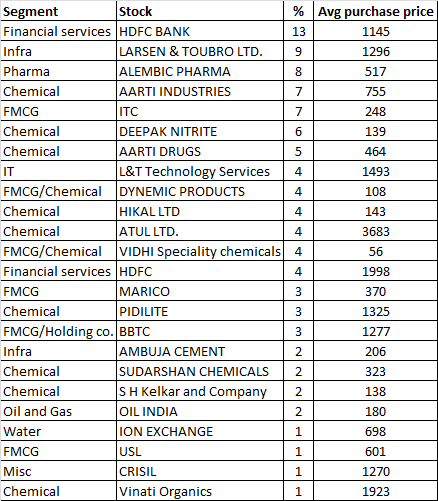

You haven’t indicated at what average price you have bought these stocks. Even if you have bought them in sip mode, valuations does matter, especially if you are in it for the long term.

@akash_das Part of it is because of the dream run that the chemical sector is having in India over the last few years and some winners do stand out. I find it relatively easier to identify moat in this sector and evaluate product niche, customer stickiness etc. I intend to have ~40% of my portfolio in Chemical space

@Abhishek16 Please find average entry price below. Much of the portfolio has been revamped in the last 6 months. I intend to deploy 50% additional funds in the next 2-3 months due to expected inflows. Hence, the objective is to learn from collective wisdom and deploy additional funds in the portfolio basis feedback.

Be mindful of companies mainly thriving on the China disruption advantage, as these companies are likely to suffer price erosion when / if China decides to change their strategy. You need to be careful with Hikal in this regard.

Also, you’ve companies like Dynemic Products & Vidhi Specialty in Food Color space, and S H Kelkar in Fragrance & Flavor space. These niche companies have moats and switching costs advantage. But you also need to be concerned about the market size & growth of that market.

Both Food color & Fragrance / Flavors sectors have limited market size & also growing slowly. Companies with small market cap in these industries may still grow well but they can at best be medium term play as sooner than later the base effect will come into play. I believe that the low PE of Vidhi & Dynemic, despite strong growth, is an indication of market’s skepticism in these companies’ long term growth capabilities.

Also, FYI fragrance is not a sunrise industry. It is quite matured, but some organized players are steadily taking away market share from the unorganized or weaker-organized players due to better branding.

Whenever I see very low portfolio allocations (1-2%), I get curious. I myself do these sort of on and off small “investments”, but in reality those are just for tracking. Here it looks like you have actually “invested” in these stocks (Please correct me if I am wrong).

Here’s a thought experiment. If the rest of your Portfolio remains the same and a stock in which you have 1% allocation made a 10x over 10 years (~26% CAGR), do you know how much contribution the stock would do to your Portfolio’s growth? 8.91%. No, not 8.91% in CAGR. 8.91% absolute returns over 10 years. Of course, actually the rest of your Portfolio will grow more, meaning the relative contribution of the 1-2% stock(s) would be much lesser.

Let me not force you into concentrating your Portfolio. I can’t be the judge of your Risk Aversion. But like Buffett once said, nobody made a ton of money by betting on their 15th best idea. The truly great bets are in short supply. So it makes very little sense to put a minuscule amount of money in a bet that’s going to fetch you peanuts even when the standalone returns is fantastic.

Take a close look at the stocks in which you have 1-2% allocation and think, really think, if they are great ideas. If they are not, you can probably reallocate them into a better idea (Cash/Liquid Funds is also a good bet in case you don’t find any).

@sujay85 - Fair points. Yes I am tracking China situation. The general sense seems to be that because of increase in environmental costs etc. in China, India is now expected to continue to remain more competitive.

For food colour companies, I’m expecting that they will mirror FMCG growth rate because of their end use. Also the regulatory aspect on account of being an ingredient in food as well as top notch clientele provides some amount of certainty to business. With capex being in final stages in both Vidhi and Dynemic, I expect volume growth to kick in. There will probably be some pressure on margin because of increased supply in the industry.

Fragrance industry was called sunrise industry because of their usage personal cosmetics and other segments which are actual sunrise industries. Probably, I need to do some more work on the overall market in this space.

@dineshssairam - Yes, most of the 1-2% allocations are tracking investments. I generally stagger my entry point wrt time and/or price points. In some cases, the stock ran away after my initial entry and I did not have the conviction to add more to the portfolio at higher price. Such allocations sometimes remain at lower % and I try to increase their allocation in future on dips.

Also, the conviction to identify one’s best bet probably comes with time. Presently, my high conviction bets are HDFC group (17% allocation) and Aarti group (12% allocation) - these are not cheap and hence I try to time entry points via technical analysis and buy on dips. Probably, next in the list which I intend to add more are Food colour companies (Vidhi, Dynemic) and LTTS (cutting edge tech services)

@maheshkumar - Theoretically correct. But it’s difficult to build in an expectation of any stock being 100 bagger when purchasing. It’s always a bonus if it happens, in which case, one should increase allocation as more triggers are realized during the journey.

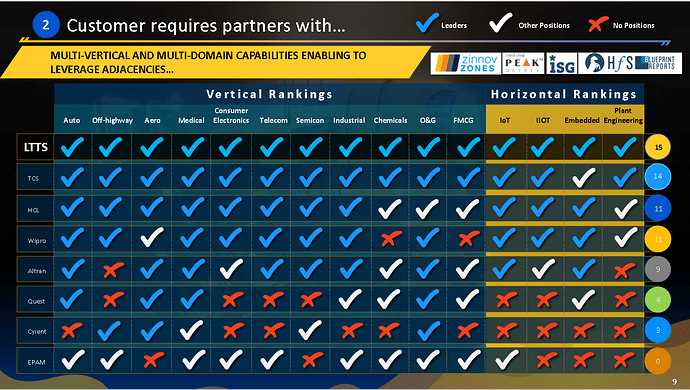

How is ltts any different from any other tech company except that it focuses on just engineering services vertical? There is the argument of various patents , IP etc but they are for insignificant stuff when it comes to contribution to profits or even future profits. Pls correct me if wrong or with any new thoughts. Thanks

LTTS and Tata Elxsi derive their strength from being part of large conglomerates and having a better understanding on certain segments. Below image provides a glimpse:

I believe that many industries are due for disruption and companies like LTTS and Tata Elxsi will be at the forefront of driving these changes.

I checked the share holding pattern of Britania and I dont find Bombat Bumrah being the holding company for it.Infact promoters are foreign entities and largest share being held by Associated Biscuits International limited.

And in 2019 BBT eps jumped from 40(2018) to 120 odd levels.The main contribution for it seems

Shares Associate of 434 crores.Please let me know how and why this happened??

~50% stake in britannia is held by BBTC through some subsidiary based outside India. Go through the annual reports and you will be able to figure out on the same.

For BBTC, eps does not make much sense since the market is valuing it more from a sum of parts perspective than as an operating company.