This is my first ever post on the platform…please bear with any points that I am unaware of.

The company that I want to discuss is BankaBiolooLtd. Surprisingly I didn’t find any threads related to the company on the site.

Overview:

Was founded as a proprietary business named Banka Enterprises in 2008 by Namita Banka. She was later joined by her husband, Sanjay.

Converted to a Pvt. Ltd. Co. in 2011 or 2012. Got listed in 2018 on NSE EMERGE.

Currently, Namita Banka is Founder and MD while Sanjay Banka is Executive Chairman.

Marketcap: INR 740 Million (Small-cap)

Business: Provides sanitation infrastructure and turnkey, human waste management solutions and services. Also provides sanitation operations and maintenance (O&M) services to the Indian Railways.

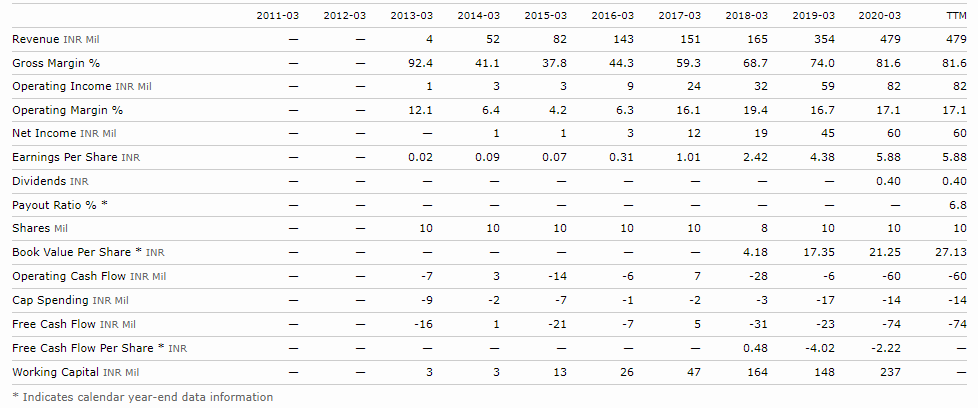

Numbers and ratios with which company is growing is quite impressive

Promoter shareholding: 59.11% (0% pledged)

Products/Services:

Bio-digester: This technology was developed by DRDO (for soldiers at high-altitude bases) and was transferred to Banka via ToT. This technology is used in bio-toilets.

Bio-toilets: Consists of toilet cabin + multi-chambered bio-tank + bacterial culture (Psychrophile). The modular structure of bio-toilet is a patent-pending technology (as of Jun’19) designed by Namita herself. The average life span of a bio-toilet can be up to 35 years. These do not require sewage connectivity and because the process is self-contained, are also maintenance-free.

FootLoo: is a low-water flush system, best-suited for environment-conscious people. FootLoo comes in two specifications, one using no water, and one using very little amount.

Pluto: has indigenously developed and patented a small-scale Faecal Sludge Treatment Plant (FSTP). It is based on Geotube technology.

Urban STP: collaboration with Aqua Nishihara Corporation, working on Japanese technology, Johkasou Wastewater Treatment Technology

Some random points that I collected from multiple articles, videos, and ARs:

As of April’20, had installed: 5,000+ bio-digester, 10,000+ bio-toilets/bioloos (across 22+ states), 2 FSTP

2,000+ bio-tanks installed in train coaches across India

13,000+ bio-toilets monitored and serviced daily in train coaches

As of August’20, employee count: 1,000+

Word-of-mouth helps them to get new clients

Uses polystyrene bricks for building toilets

Average cost of developing one bio-toilet is around 30-35k (from one source) 85k (from another source)

From FY20 AR:

Indian Railways (also was their first-ever client) were the largest client and accounted for 81% of FY2019-20 revenues

Unexecuted order book from Railways: Rs. 500+ million

Unexecuted order book from non-railways: Rs. 400+ million

Has raised Rs.38 million of ECB (External Commercial Borrowing) from WaterEquity, a US-based asset manager focused on solving the global water crisis

Key priorities (i) Reduce Railways service concentration (ii) Full-stack offering in wastewater & fecal sludge treatment plants (iii) Disinfectant services (iv) Deliver superior returns.

India ranks among the top 10 countries with poor sanitation facilities. India has around 7,000 towns with less than 1 million population. Almost all of these towns as well as urban poor do not have an efficient underground sewerage system connected to sewage treatment.

Only 24% of Indian cities are connected to a CSTPs (centralized STP)

Since the inception of Swaccha Bharat Abhiyan and various other such initiatives taken up by the GoI, the mindset of people towards sanitation is gradually changing as they realize the necessity of it. After building a large no. of toilets across India, GoI is now focusing on the treatment of waste via ODF++ (open defecation free). This opens up opportunities for the company.

Challenges/Negatives:

Daily volumes traded are very low (less than 20k on average)

Negative FCF in past multiple years

Government business is through tendering and has witnessed significant pricing pressure.

One remaining challenge in promoting toilets’ use involves the perception among some Indians that sanitation is not worth paying for. Many are comfortable with defecating in the open.

In rural India, problems relating to Vastu, land, etc prevail. But they take care of it by building toilets in whatever way they want by changing the exterior, technology, design a little bit because they have learned that if they force a single model/design on everyone, then some do not use it only

Initially faced a challenge that not many people look forward to investing in these sectors and so there was shortage of grants/funds’. (I am not aware what the situation is as of now)

Why I consider it as an opportunity:

Sustainable and eco-friendly business model

Highly focused on innovation, R&D

Well-experienced and seemingly above-decent management

Clients: IR, Integral Coach Factory, Government of Telangana, L&T, Shpoorji Pallonji, Havells, GAIL, IOL, HP, etc.

Started to see some interest from overseas as well. (Kenya, Peru, Nigeria, Thailand) (As of now, the company is present within India only, but any overseas demand would lead to exponential growth)

Despite being a small-cap, has a dividend yield of 0.96%

Invests up to 5% of revenues in R&D, innovation, and market development. (Positive: I feel this is pretty high as compared to average R&D spend by Indian cos.)

Their proposal to get $1 million from Miller Center for Social Entrepreneurship’s GSBI Accelerator program had the sections in which they would utilize the capital. 9.7% i.e., $97,000 was for R&D, innovation.

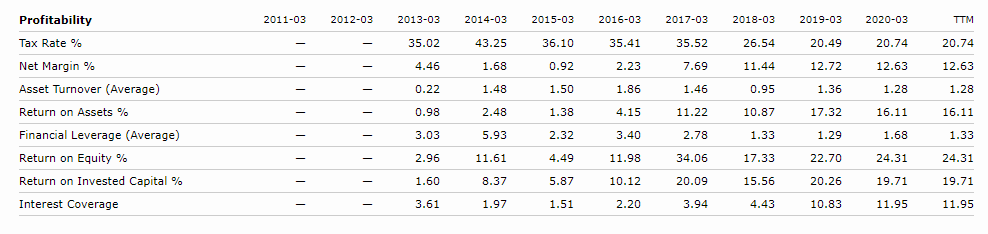

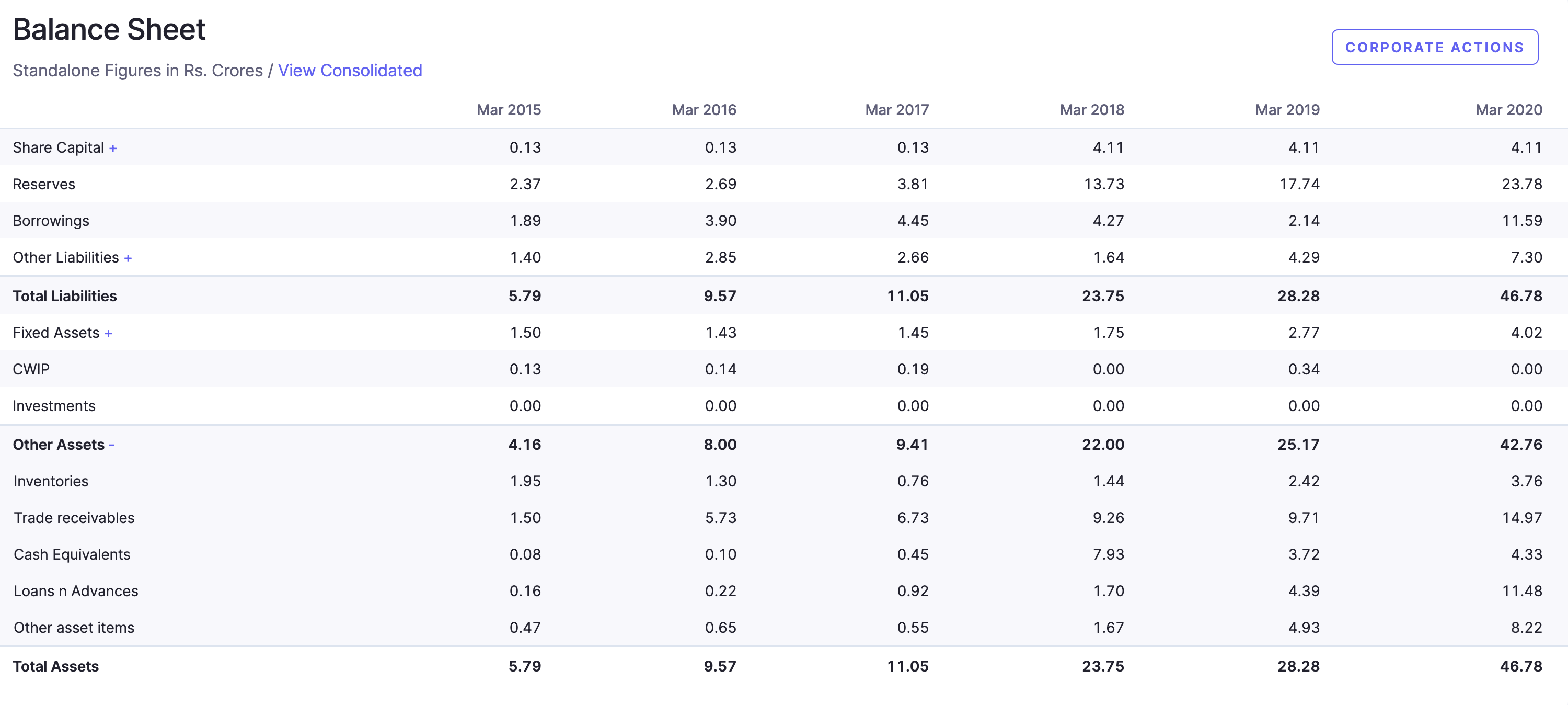

Have reduced their D/E from 1.15 in FY13 to 0.11in latest quarter

Company is working in full value chain: designing toilets and other technologies, manufacturing, then maintaining and servicing them followed by the treatment and recycling of fecal sludge generated.

Disc: Not currently invested

Please feel free to share your opinions/analysis to add value to the thread. Also, I would appreciate any comments on things you liked/disliked about the analysis. Cheers

Thanks a lot for posting on this company. I had studied it few months ago. I decided to give it a go for 2 reasons:

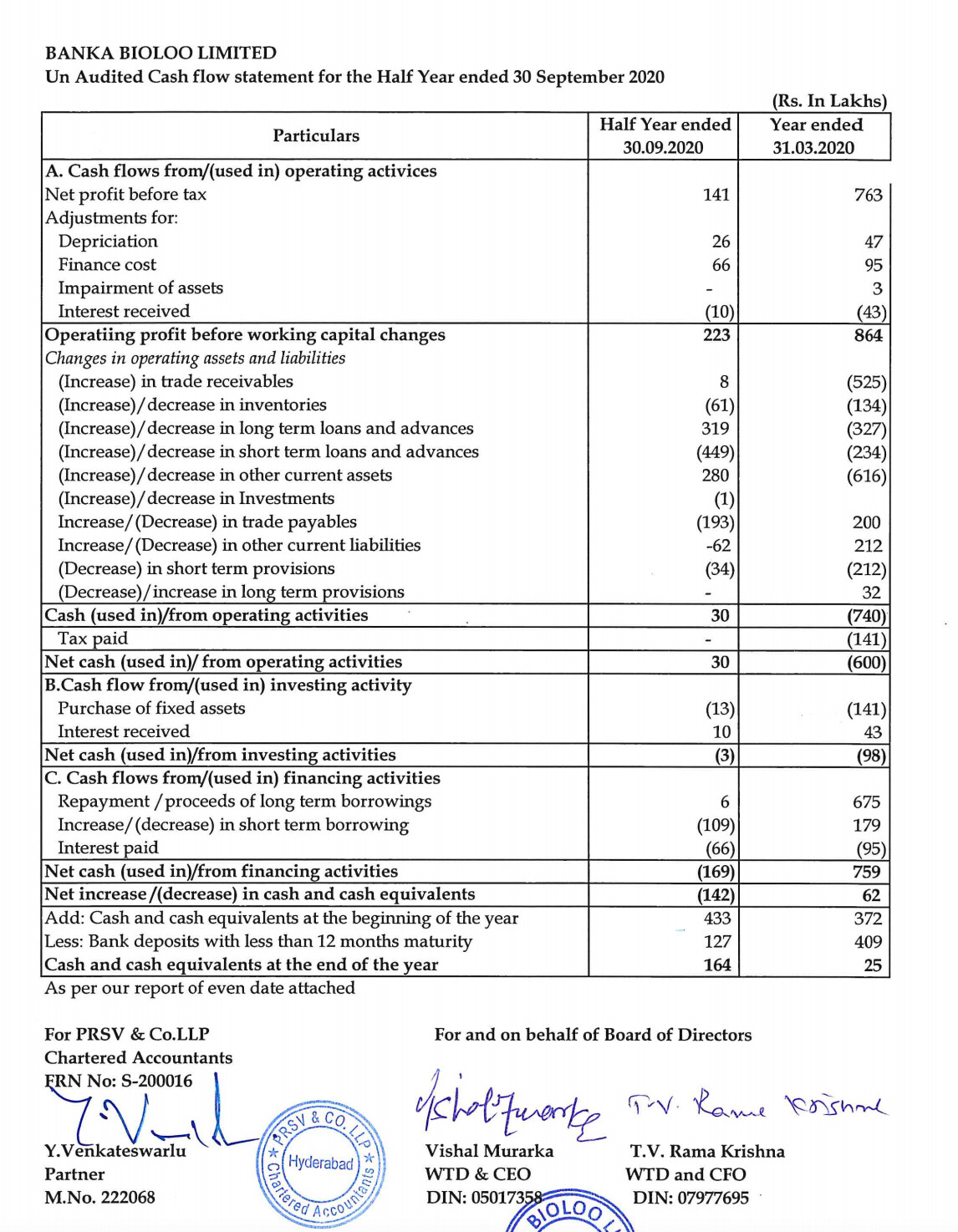

Look at the cash from operations. It’s been negative for last 6 years. negative FCF is alright. Negative CFO is not. It might be ok for a 1-2 years but for 5-6 years?

The reason for this becomes clear when one reads the annual report:

Banka AR

Our government business is through tendering and we

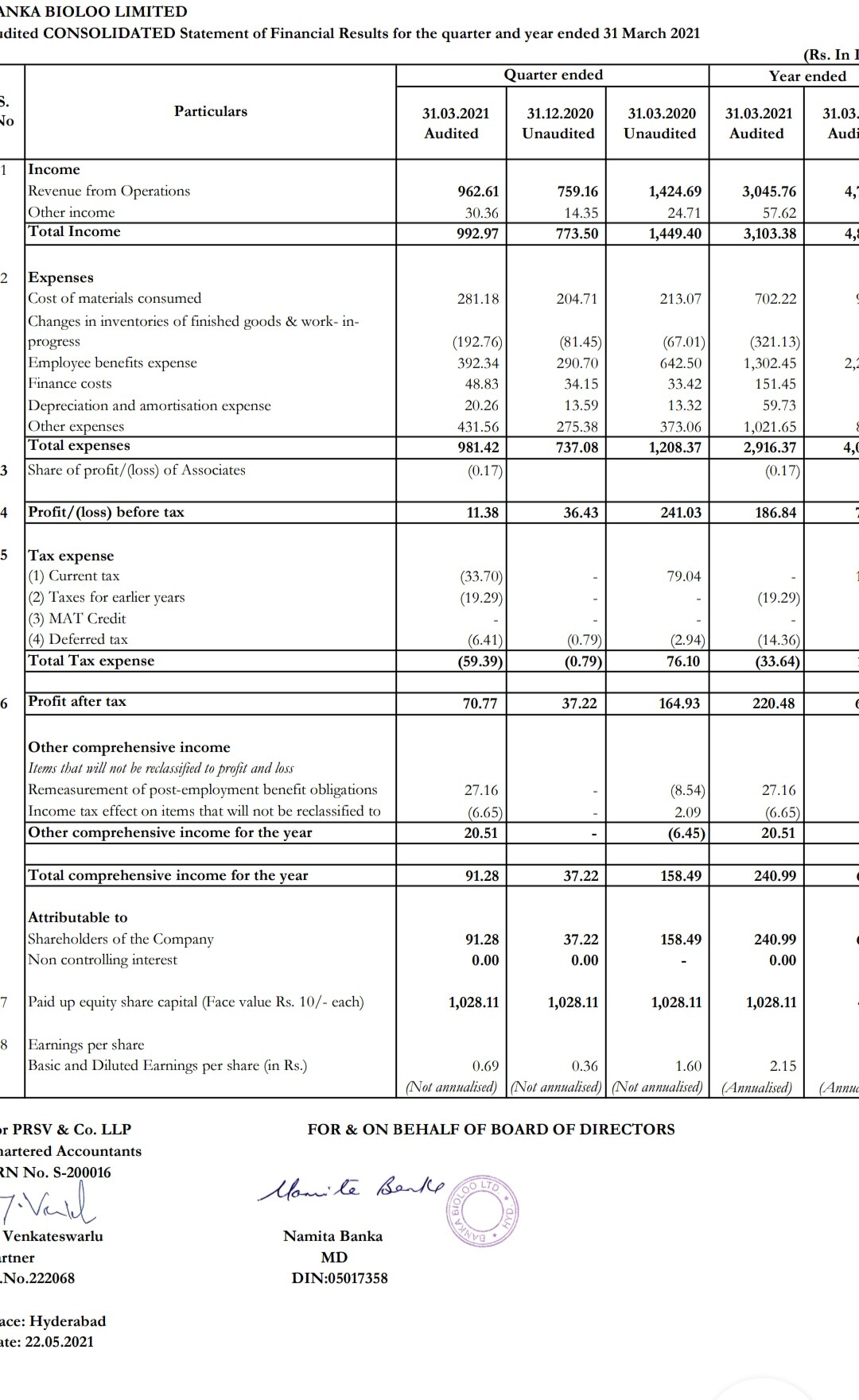

have witnessed significant pricing pressure…In FY2019-20, we serviced over 13,000 bio-tanks maintenance per day for Indian Railways. In addition, 1500+ new BioLoo (Bio-Toilets) were manufactured and installed across rural and semi-urban locations. We are working closely with the Railways to offer new and innovative products to upgrade facilities in trains and railway stations.

The company gets lot of revenue from Government. Such businesses often have a high risk of the government not paying up, or the payments being held up for one reason or another. Cash is the life and blood of a business. Without any cash from operations coming in, it’s difficult to see how the business would sustain. I really like the business and the industry and continue to track. But unless all the paper profits from yesteryears convert into cash from operations, there is significant risk for the business.

Having said that, the position seems to be improving in the latest Half. I continue to track.

I had completely skipped over the points you pointed out.

The company had received the first tranche of $1 million sanctioned loan, ECB from Waterequity.org in March 2020. This might have helped them steer their way through the pandemic.

Hopefully, with improvement in CFO figures and further tranche receivables, the position will improve.

I was going through the numbers and in expenses, the material cost has halved over the last 2 years along with manufacturing cost reducing as a percentage of total expense. Whereas employee costs have contributed more to the expenses. (Source : Screener)

A company offering products as such had such low expenses for manufacturing and materials?

Maybe I’m missing something or these were inventories utilised from previous years?

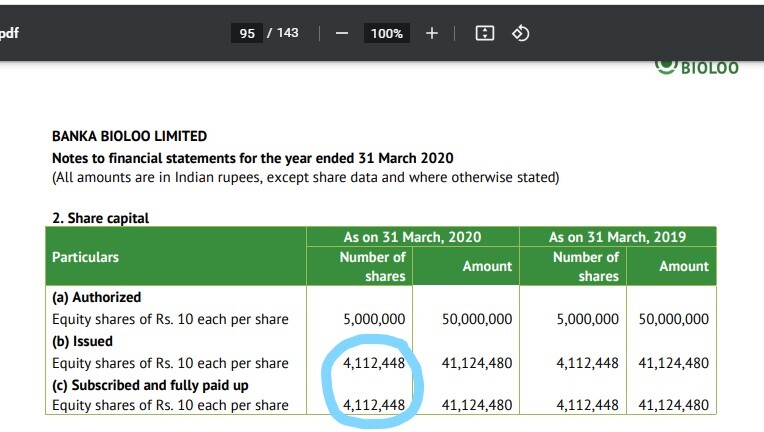

The EPS data in Morningstar/Screener doesn’t seem to match with what is available in the company AR. For FY19-20, the AR gives the EPS as Rs. 14.7 whereas the same is given as Rs. 5.88.

This increased the total outstanding shares to 10,281,120. Screener and Morningstar are using the updated number of shares with previous FY’s net profit hence it’s showing as 5.88 (60,456,142/10,281,120 = 5.88)

They should use the updated no. of shares for the FY21 results and not on FY20 results

Good to see the H1 trend continue and first year of operating cash flows. While receivables have improved, inventory has gone up by a lot. Would be interesting to read their annual report to better understand the reason for these changes. I think the next level of analysis for someone very interested in this company would be to try and understand the competive landscape and banks’s market share. Are there any other small and big players who make these bioloos or are they the sole manufacturers?

Another line of accounting deep dive might be to try and understand the margin volatility.

I got interested in this stock due to low market cap of this stock and earning growth in last 5 years, also, as Kenneth Andrade holds close to 2% of total ownership.

However, I have decided not to invest right now because of the below points:

Concentrated client portfolio around 80% from Indian Railways (High Risk)

High contribution from O&M business, however, Bio Toilet/ Digester contribution on annual basis is not significant.

Claimed to install 10,000 Bio Toilets/Digestors in last 8 years which indicates 1250 units per annum, and in FY20 they installed close to 1500, so can’t see any significant growth in Non O&M channels.

Low FCF and CFO as mentioned above

In O&M vertical, can’t think of any other major business or industry where the similar arrangement as with Indian Railways can be replicated. (if anyone can share any info around this it can be a major future advantage)

Products such as Bio Toilets/ Digestor have high life span as mentioned (avg. 35 years), hence, no recurring product sales…hence, required high efforts in Business Development.

Apart from above points, what surprised me is that executive management team is paid 1.7 Cr annually when the net profits are in the range of ~2 crores, the interest cost have risen to 1.5 Cr annually and there is liquidity crunch for which debt is required. Although, CEO is paid 21 lacs p.a, however, banka’s together are taking up close 1 Cr per annum.

Positives:

Unexecuted order book which showcases coverage for next couple of years

Huge upside potential in case any of the business vertical fires which is only O&M at the time being

Please share with me in case my observations are too pessimistic or I have missed out any interesting perspective.

Can anyone tell what is the reason for the current rally in shares? is it due to some orders that company is getting or it is just due to some big shark coming into play?