Bandhan bank is going to do an equity investment of Rs. 300 crore (Rupees

Three Hundred Crore only) for acquiring upto 30 crore equity shares of Rs. 2 each (Rupees

two only) of YES Bank Limited, for cash, at a premium of Rs. 8 (Rupees eight only) per equity

share, under the proposed Scheme of Reconstruction of YES Bank Limited.

1 Like

HDFC Bank already has a micro finance division. It is very small now but they are already in the space. One of my friend at VP level heads the business for India.

Banking seems to be the most complicated business to understand. I was interested in Bandhan bank after seeing the value it had created . There are a lot of positives but we should be aware of the negatives too many of which are inherent to Micro finance lending

Microfinance seems to be one of the very risky business as I see it. It is totally unsecured. So once the asset slips, bank’s recourse for recovery is very little… Pressure is the only tactic that will work for recovery in such cases. That’s where recovery agents come in handy. SHG loans usually work on the principle of ‘joint and several liability’, however according to bandhan, they don’t go by this principle as they don’t feel that this would increase any further repayment discipline among borrowers. They are the experts so they may be right about it. But other than bandhan most of the industry lends to SHG on jointly and severally liable principle only. Now to the reasons I mentioned earlier,

-

Competition effect on NIM

Competition is going up severely. Recently even SBI has announced their venture into microfinance lending. Due to the large opportunity size this may not affect bandhan directly. But their NIM may be hit. Already there are a lot of PSUs which even have specialised microfinance lending branches where they lend @ a rate of 10 - 12.20% (approx). So that is a severe discount to what Bandhan is offering. -

Location advantage

Bandhan is a prominent name in the landscape they are currently existing. I don’t think they will ever have a very severe competition there. Other banks including SBI may not be interested in aggressively moving to that landscape either. But regional diversification for Bandhan could pose a challenge where there are many other prominent players. So entry into other regions maynot be easy at all. In the South there are already PSU banks severely lending in this sector. -

Repayment discipline

Most of the banks have reported very good timely repayment in microfinance portfolio which have prompted every NBFC and bank to jump into this sector. More than 98% timely repayment has been reported by most of the banks on an overall basis. But if you take a smaller sample for analysis (region based), there are places where NPA ratio is even higher than 50%! (based on a PSU bank book). It clearly shows that SHG groups have a herding mentality when it comes to repayment. The individual ticket size is very small that you have to lend to a large number of groups. So however prudent you are, there are bound to be some mistakes. Along with herding mentality, political influence in repayment and recovery can be another factor that could have affect repayment negatively in these areas. Misappropriation by NGOs is another major cause of NPA. But to their credit, I doubt Bandhan uses the NGO based rating for MFI lending. -

Multiple lending risks

Nowadays, seeing the very high yield on MFI loans, every single NBFC and bank is vying for their piece of pie. And most of these NBFC are using agents to chase down these people for linkages. End effect is the same people are lend to by different institutions. The amount they lend to a particular person is decided on a certain risk perception, but this totally changes when different NBFC /banks lend that same amount raising risk of default, eventhough the risk is being shared. ICICI, HDFC etc had MFI lending for many years but they do it at very few branches. -

Much touted CASA growth

Casa growth as reported by Bandhan is excellent. We can understand that as they are more into MFI lending so they will definitely have a lot of individuals from these groups maintaining their SB at this bank thereby aiding them in raising CASA. but is it just this??? NO. I have seen a lot of Bandhan bank POS machines in many large detail shops in 2017-18 period. So I had a lengthy interaction with the store manager of a large South based retail shop. He informed me that they have given them a proposal to provide POS at MDR of 0.5%, which means sacrificing atleast 0.3% on every txn (above 2000/- as MDR is borne by gov on debit card txns upto 2000/-). Definitely this would have aided them in raising the CASA but at an addl cost. So when we analyse the cost of funds, I would say we should atleast consider a part of non interest and non salary expenditure too, as the sacrifice mentioned above is a direct expenditure incurred for raising deposits. Obviously if you consider their yield on loans, a slight increase in cost in current account, which offers 0% interest may not be an issue. But the period for which these funds will lie with them may be a major factor that would decide cost. For instance, most of these large retailers may have a large working capital loan preferably with HDFC, as Bandhan in no way would be able to match interest rates of HDFC on working capital limits. So bandhan will have an agreement with the retailer, to transfer funds collected through POS to the other Bank, where they have working capital limits on a SPOT or weekly basis after keeping a min balance. So this period will be a major factor.

To sum it up, there is a large opportunity size for MFI lending, but so is their risks involved which people seldom see. Please note, the last point I have made is based on conversation with a retailer so please do your own analysis before deciding to do anything based on my post. Just put up this post as people are pointing out only the positives. I have been quite sceptical about consumer finance too, and you know where Bajaj finance has moved from.

Not invested!

4 Likes

yes, Banking is a difficult business to understand. But, luckily Bandhan has been in this business for the past 19 years. Optimists tend to see this as a good sustainable business with a proven track record and I see it as a proof of the management quality. As far as new competition is considered, there are a lot of white spaces in the industry even in urban areas. For instance, I spoke to an autowala when I visited Hyderabad recently wherein he mentioned he still borrows from money-lender at an exorbitantly high rate on a weekly basis. Imagine the situation in rural areas. Therefore, SBIs announcement will only make the industry better and will make sure Bandhan remains on its feet.

I agree to this as Bandhan knows the behaviour of a typical person from rural east. However, competition is considerably more in south India and a lack of regional recognition might hinder its growth.

This is not a new risk. Investors have always considered this in valuation. Just remember that Bandhan has an enviable track record in managing this risk

There are systems already in place to avoid such traps. And the amount lent by Bandhan doesn’t simply depend on the capacity of the borrower. One has to complete several cycles of repayment in order to be eligible for higher amounts. Those who have done a deeper study on MFI knows this aspect about Bandhan.

I don’t quite understand how CASA is related to POS transactions? Please do elaborate on this for clarity.

1 Like

most of the PSU Banks do indirect lending in MFIs … they lend through a facilitator (like SKDRDP in KARNATAKA) so the rates even if its 9-12% at bank ends up being 16-18% for the customer

(knows this by my personal professional experience)

2 Likes

These are agricultural loans and not exactly microfinance loans. Microfinance loans amounts are much smaller in amount and the collection from debtors is done daily. The collection itself is a huge cost for the company.

2 Likes

Looking at the ticket size(and also mentioned in the category), it is clear these are not microfinance loans which we are discussing.

1 Like

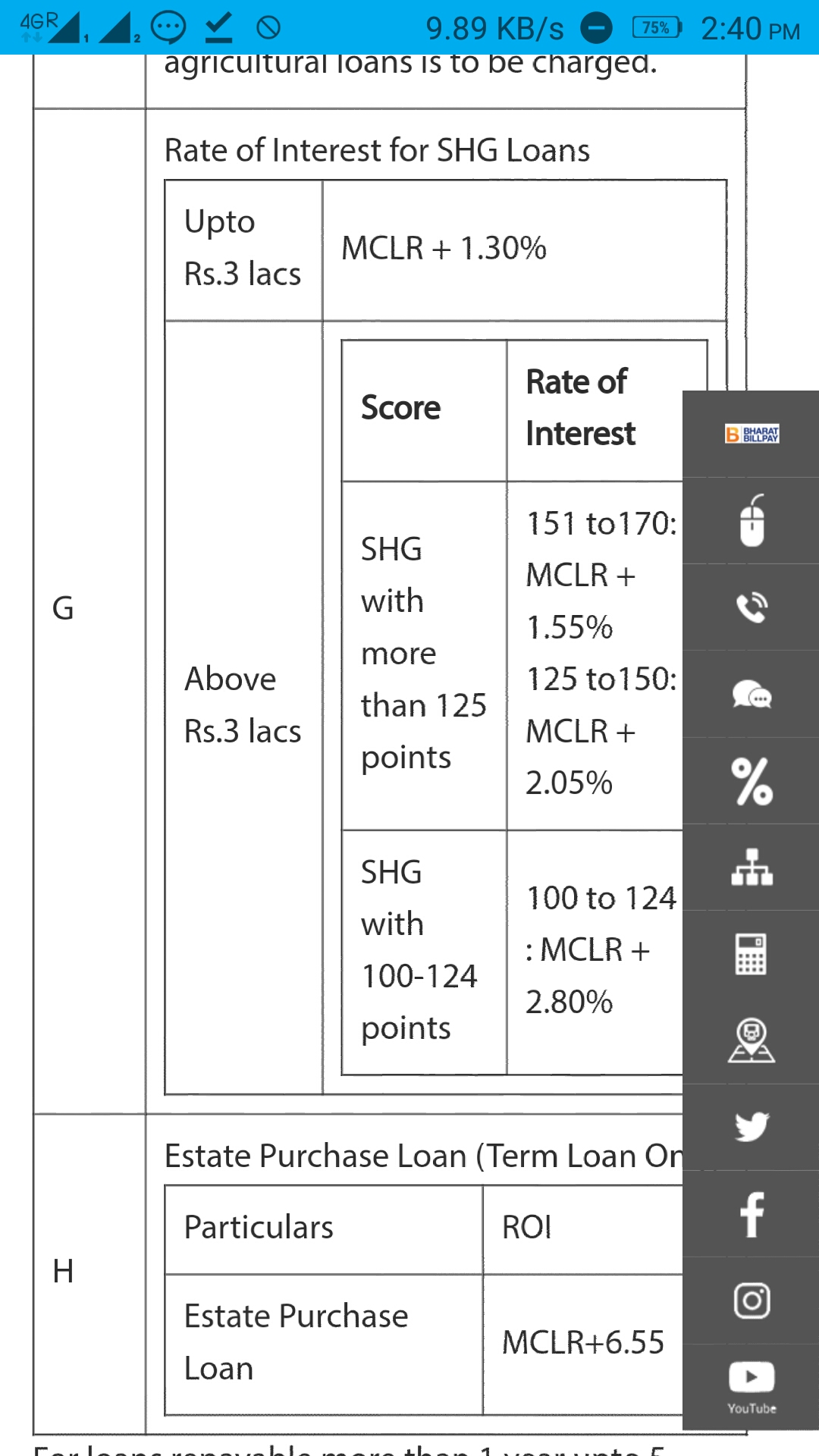

These are SHG loans .SHGs usually consists of groups of 10 - 20 members. Loans are usually sanctioned to the groups and the amount is divided among group members. Now you divide the quantum or ticket size mentioned with no of members and you get the small loans that we talk about.

There is a govt funded DWCRA program. This is similar to SHG. As far as I know DWCRA charges 6%-12% interest. How SHG of Microfinance are sustaining when there is a direct govt funded programs are competing( with less interest charges)?

I don’t know about SKDRDP. But PSU banks directly lend to SHGs which iam sure about. Usually there is a sponsored NGO who rates these SHGs but they are not supposed to earn any commission on if. There is no need for any intermediaries. However banks do lend to MFI institutions too. But that’s a different class of loans.

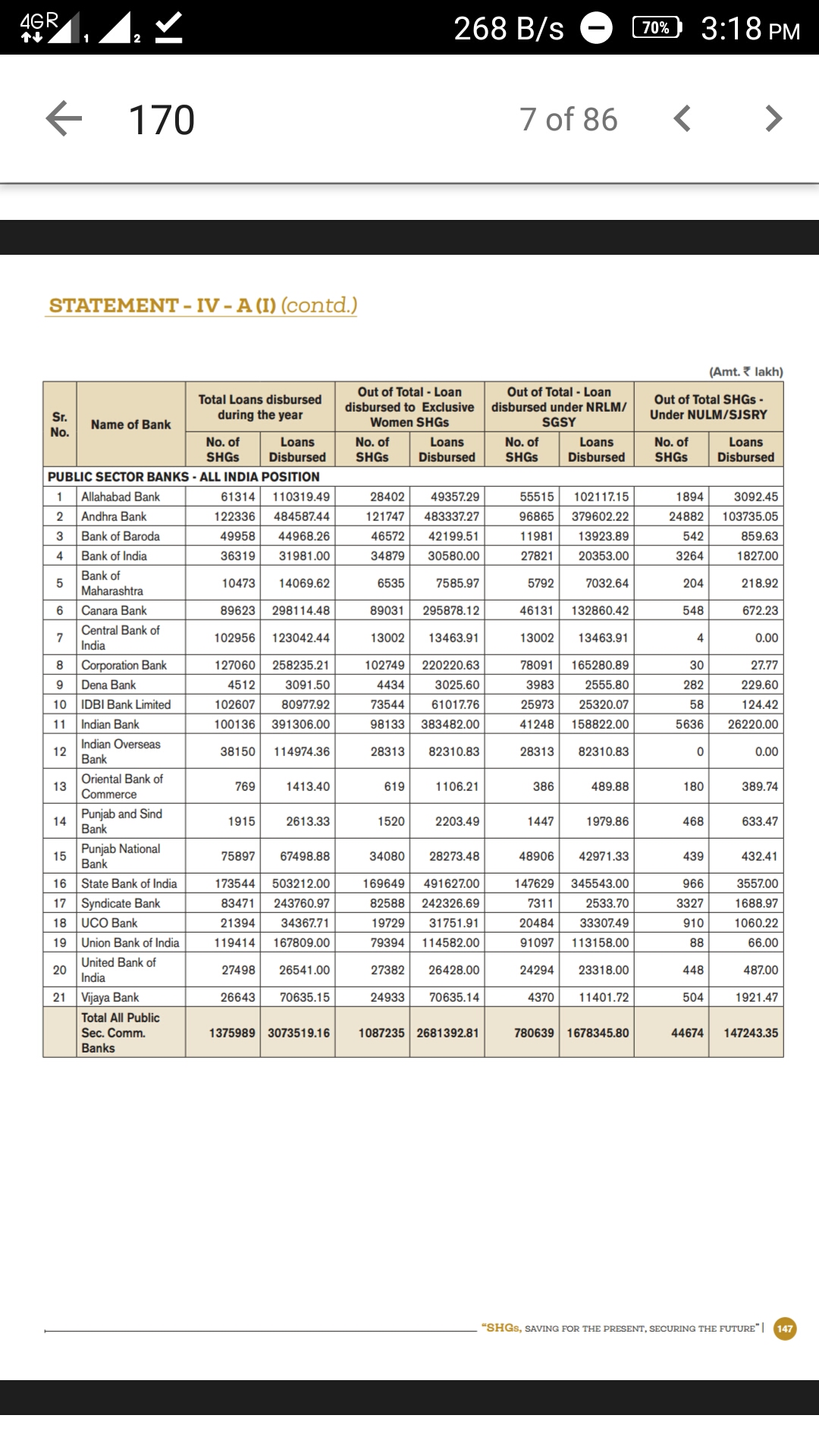

Also attaching direct disbursement made by PSU banks to SHGs in 2018-19

First of all , I am not telling that the business of Bandhan or other MFIs are not sustainable… The opportunity size is too large which I have already mentioned. I was just pointing out some negatives that they may face especially during expansion. If you ask me why people go to MFIs when there are govt funded schemes with low interest it’s obviously that to get hold of a loan through govt schemes is very difficult. They have so many guidelines and u need to have the right contacts to get those. Low awareness is another factor. Lastly these schemes are localised and they are not available everywhere. Don’t know specifically what DWCRA is…

The MFI or bank lends to the group and they in turn lend to the members of the group based on their requirement. That’s how usually SHG loans work. They are jointly and severally liable in this case.0609185415Cir_230_E_compressed.pdf (2.0 MB)

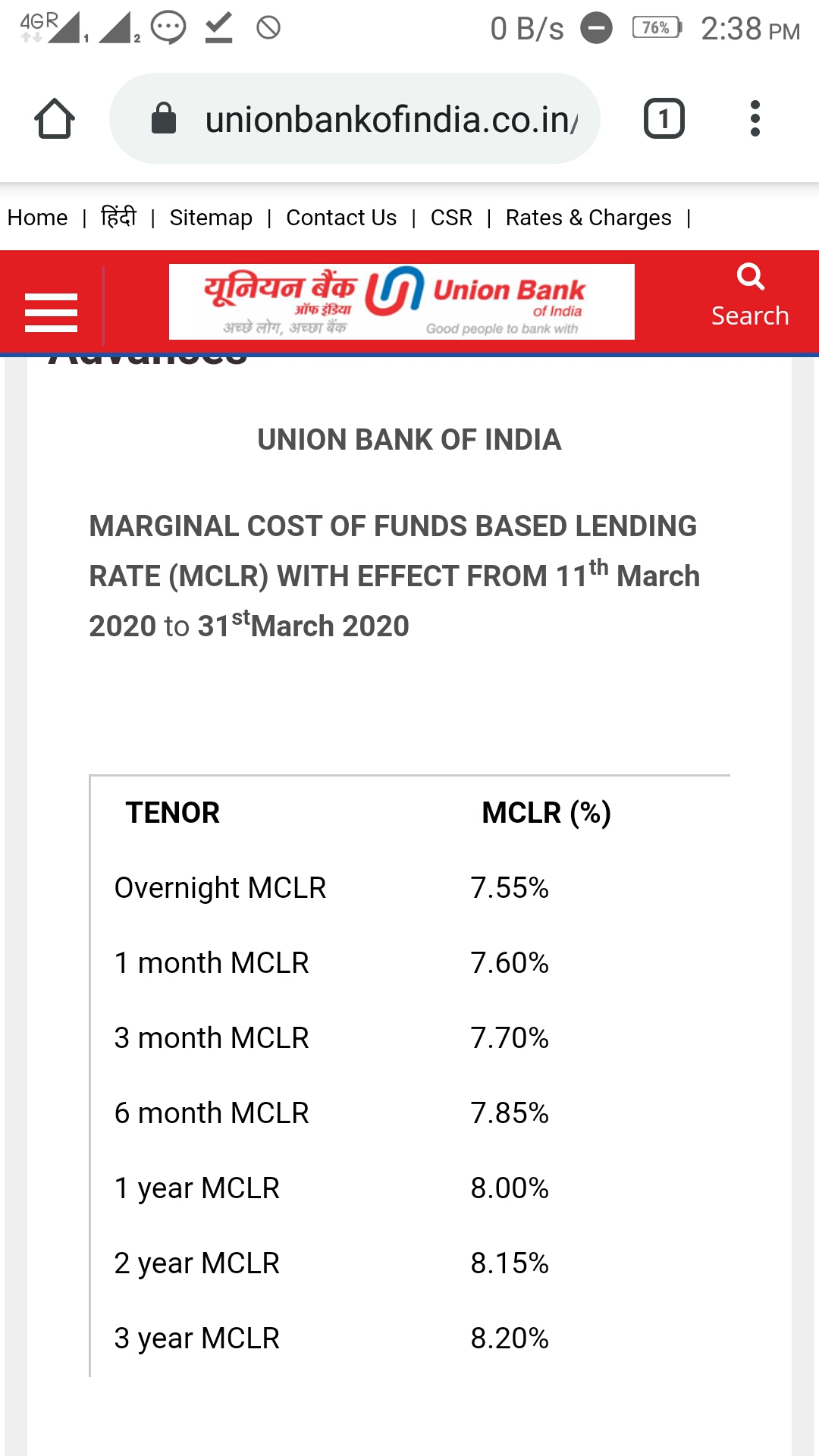

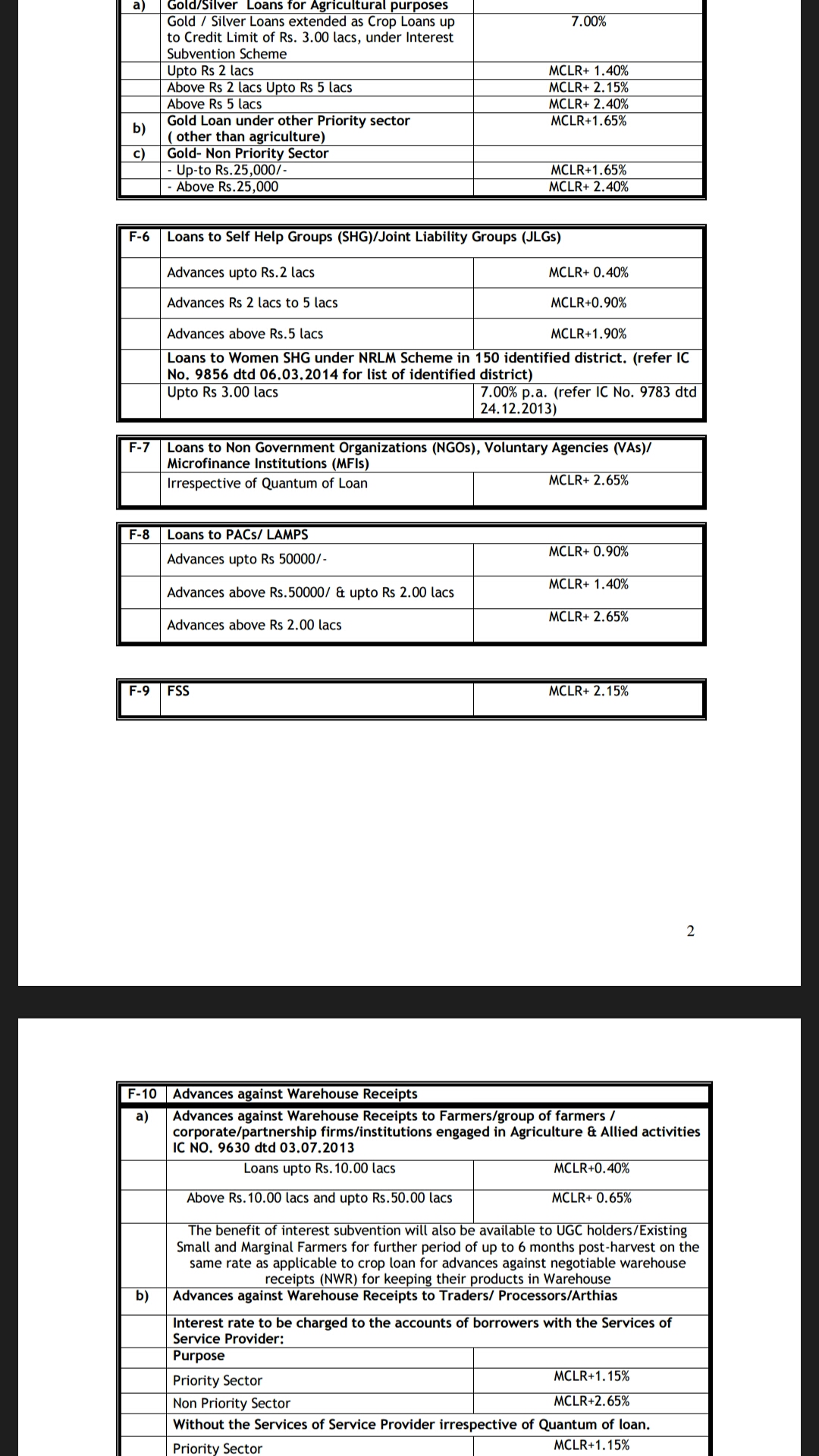

Attached NABARD circular

Bandhan Bank to gradually lower exposure to microcredit

12th Mar 2020

Bandhan Bank is going to gradually lower exposure to microcredit in percentage terms over the next three to five years. When the private lender started operations in August 2016, microcredit constituted 85 per cent of its total loan portfolio.

As per the Bank, its exposure to microcredit at present is 61 per cent. Over the next three to five years, the bank’s ratio of micro and non-microcredit will be 50:50.

Nabard is not a micro finance.They must be extending to cooperatives which are run by a group of people.Microfinance lend to individuals but SHG or JLG help the company in repayment as non payment brings the credit rating of the whole group down and in JLG system, the liability is passed to the remaining members.The JLG keep visiting the debtor ensuring payent.So there is a community pressure too to pay up.

Agree to it that they are experts but the scenario has changed a lot in recent years with competition higher than ever before. Many years before it was a sector no one dared to touch. Bandhan did a wonderful job by identifying the opportunity and making very good use of it.[quote=“Inimitable_Investor, post:497, topic:16722”]

, I spoke to an autowala when I visited Hyderabad recently wherein he mentioned he still borrows from money-lender at an exorbitantly high rate on a weekly basis.

[/quote]

That’s the situation everywhere in the country. If you visit any of the prominent markets in the country . you will see moneylenders collecting the daily repayment from fish,vegetable vendors etc. There is a very large opportunity size. But the problem with them is even if a bandhan lends to them, They often tend to get addl loan from the money lenders as a matter of habit. And these money lenders are not people whom u can default on even for a day. So this is where the branch has to tread very carefully as your loan gets the least priority.[quote=“Inimitable_Investor, post:497, topic:16722”]

There are systems already in place to avoid such traps. And the amount lent by Bandhan doesn’t simply depend on the capacity of the borrower. One has to complete several cycles of repayment in order to be eligible for higher amounts. Those who have done a deeper study on MFI knows this aspect about Bandhan

[/quote]

I agree that Bandhan has good systems in place. But what about the other MFI companies. Linkages may be given by Bandhan based on their past repayment history, but there are others in the business who are ready to lend to these people. So they too lend to these same people. So as per risk perception of Bandhan , Bandhan gives him say 20000, two other companies who are more aggressive lends him / her again thereby raising the overall risks. That is why RBI has made it mandatory for reporting credit details of SHG members to Credit information companies. But doesn’t know how effective it is. I seriously believe many MFIs are flouting guidelines regarding multiple linkages to the same borrower[quote=“Inimitable_Investor, post:497, topic:16722”]

I don’t quite understand how CASA is related to POS transactions? Please do elaborate on this for clarity.

[/quote]

When a pos transaction is done, that amount gets deposited in the vendor’s or retailer’s current account. There is an MDR associated with it which varies with different cards like debit, credit, platinum credit etc. We take debit for illustration purpose. Normally the MDR charges for a debit transaction is 0.90 %. That is the amount that gets deposited in the merchant’s account will be lesser by 0.90% than the swiped amount. Usually this 0.90 % will be shared between POS issuer bank, card issuer bank and the aggregator. For the pos issuer usually the commission is about 0.10 %, so when the bank offers a rate of 0.50% MDR you essentially have to bear the burden of 0.30% which needs to be shared with the other players ( the card issuer and aggregator). So by subsidising MDR they have gained a large number of current account.

National Bank for Agriculture and Rural Development (NABARD) is an Apex Development Financial Institution in India.[4]

The Bank has been entrusted with “matters concerning Policy Planning and Operations in the field of credit for Agriculture and other Economic activities in Rural areas in India”. NABARD is active in developing Financial Inclusion policy. The circular is based on which banks lend to SHGs

No intentions to clutter the thread …don’t know why someone flagged it.

3 Likes

Collections are bound to be impacted in this quarter and small businesses are sure to be hammered the most because of the shut downs, some clients may even go unemployed in this situation thereby increasing NPAs. I think the business would be in a mess for a quarter or two for sure. For long term investors, it is better to stay patient on the sidelines as the stock is likely to remain at these levels at least till the quarterly results. Based on the results over the next quarter or two, one can start accumulating. The rally will not be as fast as the fall and therefore one will get ample time to get into this stock.

Disclosure: invested 5% of portfolio at 320 levels and still believe that corona will not infect the MFI story. It’s hard to keep myself motivated after this bloodbath ![]()

8 Likes

Brief write up on recent fall in Bandhan share prices

There are mainly 5 concerns

1) Corona’s Impact on Disbursements / Collection and NPAs

This is spread across all business / industries and even experts will find tough to measure its current impact at this time. Market is assuming sharp spike in NPAs due to cascading impact of virus and it is a biggest worry causing recent downfall. Bandhan is connected with very small businesses (apart from Gruh’s home loans) and the lockdown due to virus will certainly impact daily / weekly / monthly earnings of its core customers. The virus is still spreading to unaffected zones and it is all set to impact next quarter as well. Apart from this regulators have provided extra month for Q4/ Annual results, which will also contribute in exact NPA details becoming available to general public with delay (on ground banking employees will certainly have exposure to their specific work areas). We have to wait till management comes out with their version or declare Q4/Annual results. Keeping a close watch on developments on virus spread and efforts in making medicines / vaccines available for treatment will help in NPA guesstimates.

Management indicated that in the worst-case scenario of complete lockdown for 15-20 days, they will stop the disbursements and collection (similar to when a calamity occurs). They have confirmed that there have been some withdrawals in deposits from government entities which amounts to less than 1 percent of the total deposit base due to Yes Bank fiasco. Bandhan has no issues with group meetings as of now and has made few changes to the overall process.

2) NPR/NRC impact in north east

Second issue contributing to recent downtrend in Bandhan is NPR / NRC agitations in north east, which has approx 16% business for them. I understand that Bandhan has aggressively provisioned for Assam issue in last quarter and as per recent interviews of management, it seems adequate to cover up. Any surprise may again push us back.

3) MFI specific challenges

There have been multiple reports quoting exploitation by MFIs in rural / illiterate communities. While such reports are sometimes biased as I see currently they most of them are targeting north east although such issues are common for other zones as well. Bandhan has survived similar challenges in last 2 decades of operation and we must trust management in tackling this one as well.

4) GRUH Merger

GRUH amalgamation process was fastest in history which speaks about ground level preparation and dedication of management. As the merger process completed well, last quarter saw some book adjustments contributing to lower bottomline. As per management that was one time impact and current quarter should resume normal bookings. Integration with Gruh has not seen any visible issues till date, although its too early to say that all is well but being optimistic we are hopeful to see bright light trusting leadership of Bandhan & Gruh both.

5) Promoter Stake Dilution

This is another issue which has been discussed multiple times. Though management keeps on quoting in media interviews that they are seriously working on this but currently stake dilution seems to be on back bench considering recent relaxation in opening new branches, Kotak getting relief & IndusInd approaching regulators based on Kotak verdict.

10 Likes

Thanks for a detailed write up. The possible causes are more or less known to vigilant investors. Next point is the quantification,impact and likey future prospects?Can you enlighten with your views on the same, if possible

I don’t have expertise in speculative guesstimate better I will wait for more clarity from management along with interviews / regulatory fillings / result etc or any community member having expertise in identified pain areas would certainly help.

1 Like