My sentence means dharma, which is necessity for every human being. A follower of dharma can do it in any way, not necessarily only by giving money, material or service. Charity is not a word I like as it looks innocent, but conveys an egoistic attitude for any one who carries it out. Decently arguing in this forum itself is dharma practice by each one of us.

Keeping the philosophy aside, this business is definitely not comparable with other lending business because it has very high margin, probably only lesser than what a private money lender would charge.

And Bandhan has only penetrated eastern part of the nation leaving out the remaining part. So how come it has been said as Bandhan Bank covers 80%?

To re-emphasize my earlier point, the con call which I referred to has points about the pitfalls standalone MFIs have on their hand. Foremost among them all is, it protects the entity from being influenced or threatened by politicians either through legislative means or through coercive methods. At several places the local politicians mislead people by saying waiver is in the works or something like that. And BFIL has handled those kind of areas very well through their standardised policy approach. That is my understanding.

Discl- I got good allotment in HNI category in Bandhan Bank & bought some more on listing day. Bet is again on workaholic frugal ethical first gen technocrat entrepreneur with superb execution track record and opp size remains huge. Its frugal work culture & empathy with its customers & locations remains its strength.

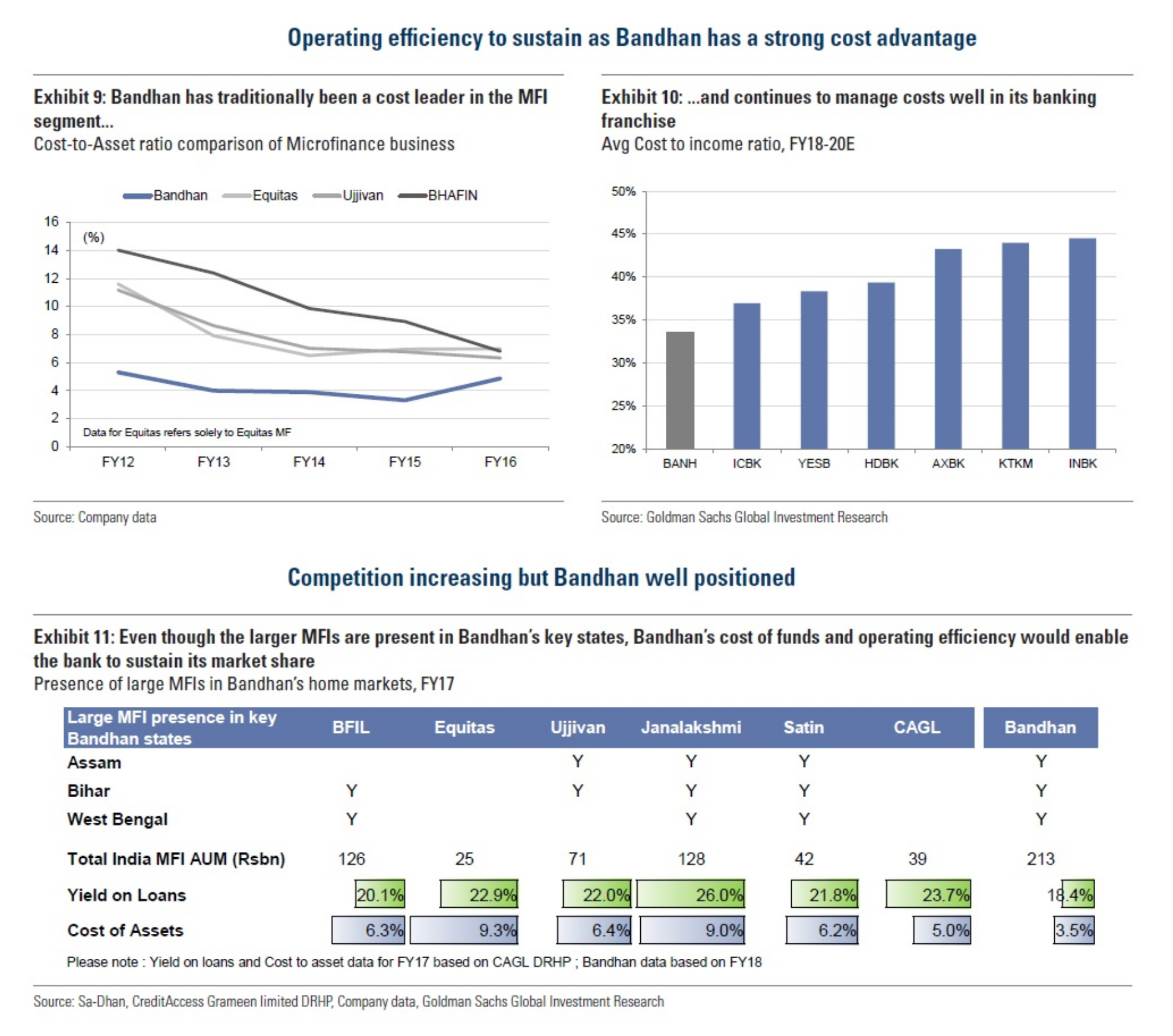

Formidable liability franchise built in a short span of 3 years ,CASA of 33%.

Cost control giving rise to above average profitability,NIM of 9%,ROA of 4 to 5%.cost to income of only 35%.Amongst the best ratio for any bank in the world.

Focus and leadership on under banked regions of India ie eastern India and the trust it enjoys among the poors ,its high touch n supervisory model leading to only 1.6% GNPA & 0.8% NNPA even after worst of DM time.It being a bank helped it a lot then.

Superb list of Anchor investor whose portion was oversubscribed 22 times.Anchor investors included Abu Dhabi Investment Authority, The Master Trust Bank Of Japan Ltd, Blackrock India Equities (Mauritius), HSBC Global Investment Funds - Indian Equity, National Westminster Bank Plc, East Bridge Capital Master Fund, White Oak India Equity Fund, Invesco India Equity Fund, DSP Blackrock Fund, UTI MF, ICICI Prudential, BNP Paribas Arbitrage, Fidelity Funds, Aditya Birla MF, Sundaram MF, IDFC MF, Citigroup Global Market Mauritius, Reliance Nippon Life Insurance Company etc. http://fpindia.in/blog/wp-content/uploads/2018/03/bandhan.pdf

Pl also read the book Bandhan by Tamal Bandopadhyay to get a better idea abt the bank & its founder.

The bank has posted healthy 20% growth in the net profit to Rs 388 crore in Q4FY2018, while the growth has been stronger at 21% to Rs 1346 crore in FY2018. Bank has fully provided for all MTM losses of Rs 21.3 crore in FY2018 itself, instead of RBI dispensation allowing to spread MTM losses over four quarters starting Q3FY2018.

Deposit portfolio of the banks surged 46% to Rs 33896 crore end March 2018. The bank has posted strong 70% growth in CASA deposits, helping to improve CASA deposits ratio to 34.3% from 29.4% a year ago, while retail deposits accounted for 72% of overall deposits. About 7% of the deposits were contributed by microfinance customers.

As per the bank, the West Bengal state contributes about 44% of total deposits, followed by Maharashtra at 16.8% and Assam and Bihar at 5% each.

The average cost of CASA deposits for the bank stood at 4.9% in FY2018.

Loan book of the bank has jumped 37% to Rs 32339 crore end March 2018, driven by 30% growth in the micro credit to Rs 27701 crore, while non-micro credit loan portfolio has more than doubled to Rs 4689 crore end March 2018 from Rs 2150 crore end March 2017.

Micro credit accounted for 86% of the overall loan book end March 2018, showing decline from 88% end December 2017.

The bank has acquired 2.6 million new customer in the year ended March 2018, of which 1 million were acquired through 936 bank branches and 1.6 million customers were acquired in the micro credit business. The overall customer base of the company has increased to 13.01 million end March 2018.

The bank has network of 936 branches and 2764 Doorstep Service Centers (DSCs), comprising to 3700 banking outlets which is the third highest level of banking outlets in the private bank sector. The bank proposes to raise its distribution network to 4000 banking outlets by March 2019, consisting of 1000 branches and 3000 DSCs.

The bank expects to sustain strong loan growth in microfinance segment in FY2019, while non-micro finance loan segment is still evolving while the growth can be accelerated with the capacities building. As per the bank, the forecast of better southwest monsoon rainfall in 2018 and better GDP growth outlook raises hopes for higher credit demand.

The bank has taken various initiative too closely monitor asset quality, and expects asset quality to further improve and credit cost to decline in FY2019. The bank has been making provision at the higher rate of 1% for standard advances against the regulatory requirement of 25 bps. The credit cost for the bank stood at 1.51% in FY2018.

The bank is exhibiting healthy momentum in core fee income generation. The bank has already started the distribution of third party products which is adding to the fee income.

About 94% of the loan book of the bank is Priority Sector Loan (PSL) compliant, so bank was participating in the issue of Inter-Bank Participation Certificates (IBPCs) FY2017, while the bank has shifted to sale of PSL certificate which is contributing to fee income in FY2018. However, the shift to PSL certificate has impacted margins by 50 bps in FY2018. The bank has generated fee income of Rs 151 crore from sale of PSL certificates in FY2018.

The system of free markets ensure that if Bandhan bank helps its shareholder its fruit will be enjoyed by larger society i.e weaker sections

Every individual… neither intends to promote the public interest, nor knows how much he is promoting it… he intends only his own security; and by directing that industry in such a manner as its produce may be of the greatest value, he intends only his own gain, and he is in this, as in many other cases, led by an invisible hand to promote an end which was no part of his intention.

If you wish to see the results of Govt. intervention in free markets, look at whats happening to Sugar industry. Govt. is mighty trying to help farmers, already sold all its mill and now trying to bankrupt all the private mills. India is the costliest producer of Sugar and now trying to export at loss.

You can also look at why we cannot blend ethanol into petrol (We are largest producer of sugarcane in the world) because our ethanol is more costly than petrol (minus excise).

Are you willing to invest in Sugar industry for the benefit of farmers?

A society, country need to decide if it is for free people and free market or Govt. control. Free people and only exist in free markets. The more we do flip-flop at times this, at times that we will hurt ourselves and remain almost lowest per capita earner in the world.

Commercial banks play an important role in the financial system and the economy. As a key component of the financial system, banks allocate funds from savers to borrowers in an efficient manner. They provide specialized financial services, which reduce the cost of obtaining information about both savings and borrowing opportunities. These financial services help to make the overall economy more efficient.

Do not follow this stock, so no fundamental comments on the company. But this company looks to have most of its business in WB, Bihar and Tripura. I grew up in the East and these states have an extremely socialist mindset. There is nothing to believe that if need be Mamata Banerjee or a Left govt. will not write-off loans. Huge risk I feel and this itself should warrant a low multiple.

Who would give them loans in that scenario in future… this could be a risk or an opportunity… unless high NPAs emerge, from its high growth, high ROEs, it looks like an opportunity

@LTInvestor@RamanTiwari Any data to support above comments specific to Bandhan? I am aware of industry and agree but specific to Bandhan , would like to highlight few points. So far, historically, they have been an outlier in micro finance pack with an envious NPA record to competitors. Even demonetization did not have any significant record on their NPAs. They have been doing this in WB since 2003. There is a book by Tamal Bandhopadhyay on Bandhan bank. I think must read for anyone interested in this script or sector. Disc : Not invested in Bandhan, 3% exposure to Ujjivan

No data but WB is a agri-based state. One year of El Nino>>Drought>>Interest rates up>>Mamata waiving loans, especially in a election year.

Also just from what I felt in WB that it is a very cadre based state. Cadres get politician votes, get them money. Difficult to believe Bandhan could get up a $9bn business with CPI/Trinamool politicians/cadres not knowing. Reminds me of what Dilli Raja from SKS had said in 2013 about WB business:

"In West Bengal, we are present in 17 districts. In Cooch Behar (north Bengal) and a few small adjacent districts, we had a problem of commission agents. They exploit rural women borrowers saying that the only way to get loan from this company is to pay a 5% cut to them. There could be two approaches to tackle this. One is to turn a blind eye and you will get money back because these women used to pay 40-50% to money lenders and they will pay 24.5% interest and an additional 5% to the agent.

Nothing to believe that Bandhan does not face this. Remember that they have the highest margin in the banking industry.

Not saying it is bad, but may not be worth paying the P/BV they are commanding.

Ujjivan is undergoing banking transformation where lot of costs r front loaded and it ll take 1-1.5 year more for cost to income to normalise which I think should happen around 50-52%

Structurally , bandhan is a full fledged bank where as Ujjivan is a SFB and as per RHI, they kind of terms n conditions which r laid out for these two regulatory entities provides ability to bandhan to have better coat to income

If you read Bandhan’s promoters life , he has been super cost conscious since beginning n it is culturally imbibed in bandhan genes you can say

Would suggest you to go through Ujjivan concall , this question was asked by one of the analysts

Disc : have not studied bandhan, invested in ujjivan

Is Bandhan bank still a microfinance institution or will remain that after becoming bank? I believe the depositors it is getting with huge increase in CASA are the same people lowest in pyramid whom they lend…at least some good is happening by making these microfinance institution as banks…in quest of CASA, they will instill saving habbit in these people…

They have targets to open a certain number of CASA accounts everyday. So the employees approach the publics mostly businessmen to open accounts. Of course opening new branches still helps.