It’s subscribed article.

See if this snap helps. There is stress. Bandhan mngmnt is not agreeing to anything wrong happening on ground. Micro lending is creating Debt Trap.my personal opinion after speaking to those who avail loans.

3 Likes

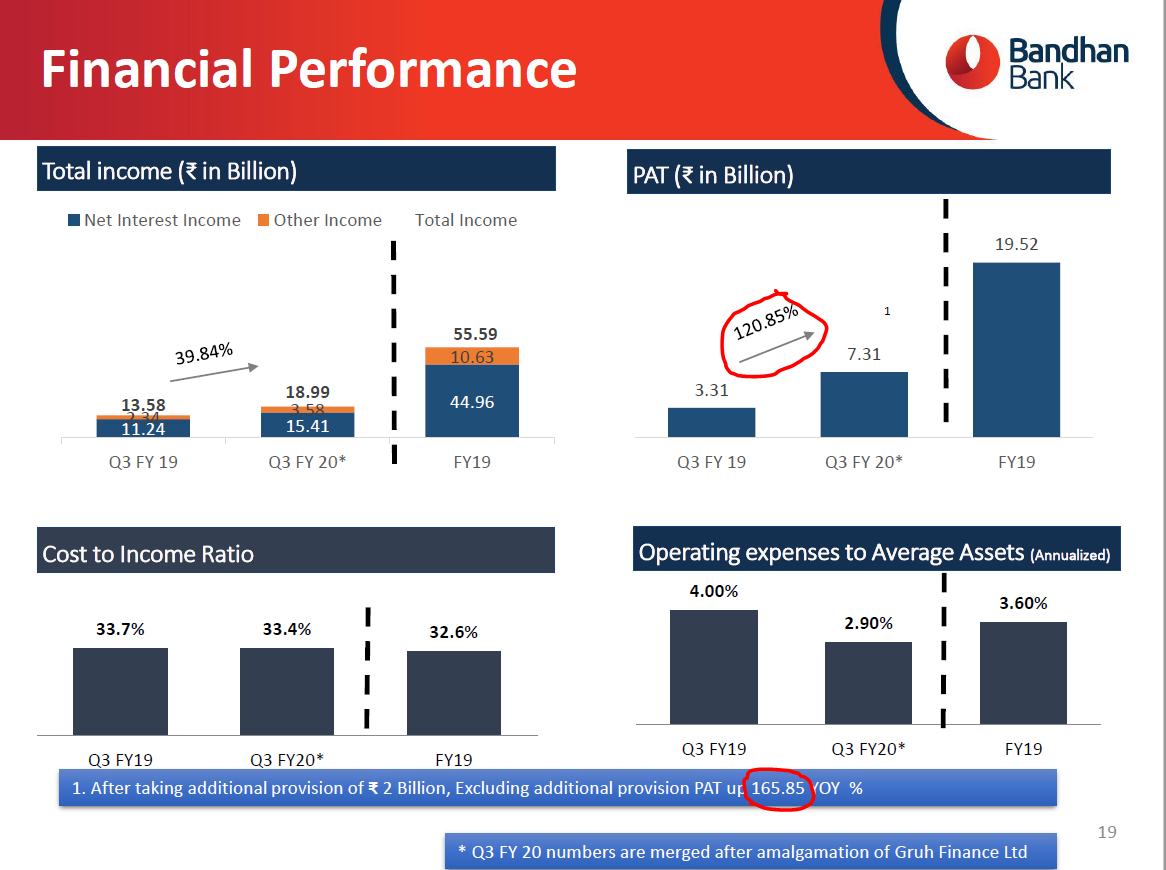

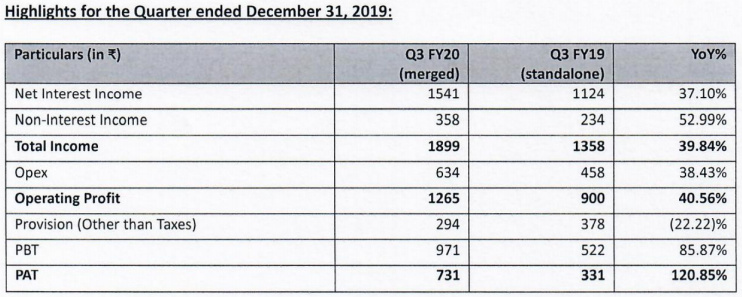

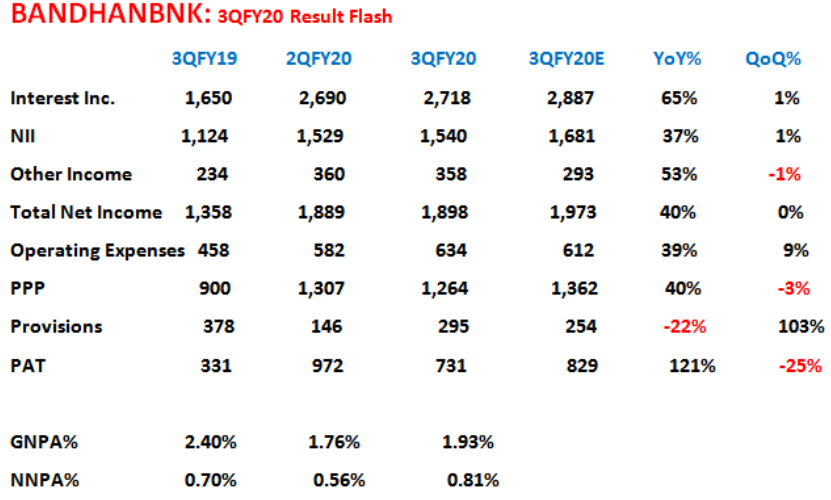

Great results from Bandhan Bank. Net profit jumps 121% even after making additional provision of Rs. 200 Crores, loan portfolio increased by 89%

4 Likes

Debt trap to those who is not willing to return the money. Sensible people trying to uplift their livelihood is not becoming defaulter.

My personal opinion is different. My 2 home maid didi is customer of Bandhan micro loan and they are happy and repeat loan getter.

6 Likes

The result is on expected lines as there have been challenges from multiple corners starting from MFI protest in Assam & then CAA/ NRC etc

- The topline is almost stagnant (Q2 vs Q3)

- Expenses have increased by 3.9%

- EBITDA stagnant … grew by meagre 0.65% (even after discounting 200 Cr provision)

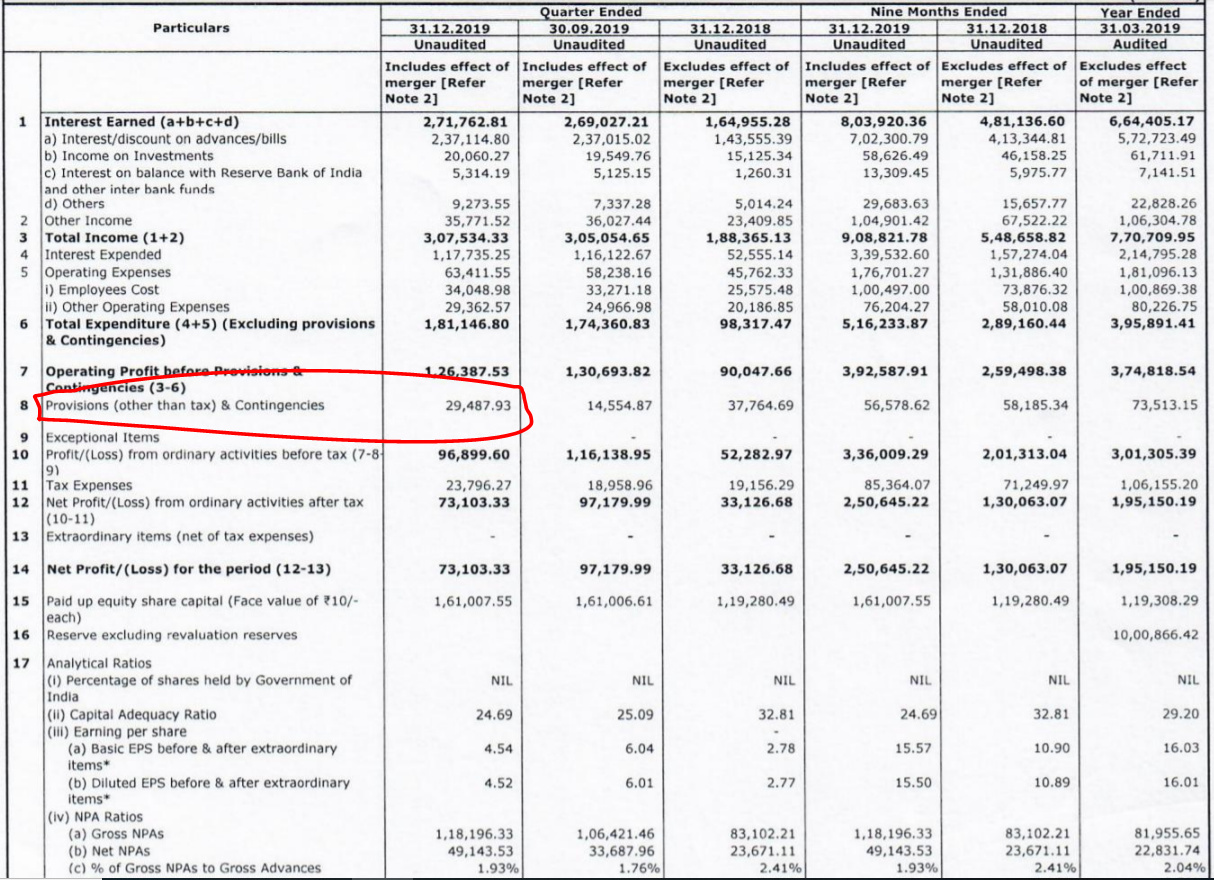

During the quarter, the Bank has made additional provision of 200 crore on standard advances in microfinance portfolio after evaluating risk observed in certain areas of a north eastern state, though having a dwindling effect.

Detailed Q3 result

1 Like

In my opinion more than YoY, we should be calculating form last Quarter as Gruh fin has merged, so that should give better picture in earnings. Increasing provision & GNPA is also concern.

1 Like

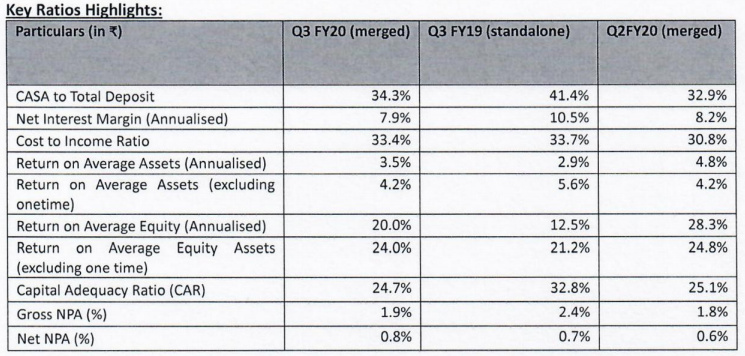

Key Ratios Highlights may tell a story, comparing Q2 and Q3 of FY20:

CASA to deposit - increase by 4.2%

Rest everything is relatively worse/declines:

NIM - dec by 3.6%

Cost to Income - inc by 8.4%

etc.

Top-line is frozen QoQ, even after Gruh has been part of Bandhan now for 1 full year. Markets seem happy just because they were scared with the situation now in East and NE, politically and specifically with microlending.

That situation seems still developing and overhang of dilution/RBI remains.

Microlending does seem an exciting field but seems everything is priced in.

Disc: Taken position variously over past 6 months, very volatile stock, cannot stomach such excitement, exited!

3 Likes

Management talk to ET now after results.

My notes after listening yesterday’s concall.

Bandhan Q3FY20 Con-call Notes:

Assam Portfolio

- Assam total book is 6500cr.

- Management confident that thing should be back to normal in 3 months.

- Seeing OTR improvement week after week in Assam. If situation remains same, no more provisions will be needed in Q4.

- Bank wide 30+ DPD Portfolio 556cr vs 384cr. Increase has been 172cr. Out of 172cr, 162cr is increase in Assam. Have used this metric + OTR + ground level assessment have taken 200cr provisioning conservatively. This 200cr is the total portfolio of folks contributing to increase in DPD from Assam. Not taken any hair-cut, but provided provision for entire portfolio.

- Total Deposits from Assam banking channel is 1474cr.

Gruh

- 82cr slippage in Gruh portfolio.

- Till last quarter NHB norms were applied for Asset Classification. Post merger Asset Classification has to be done per banking regulation. Difference is as follows:

- NHB Asset Classification Rule: on reporting day DPD (Days Past Due) is considered. If DPD is > 90, it is classified as NPA.

- Banking Asset Classification Rule: If portfolio moves beyond 90 days and even if it falls back to 60 days or 30 days, it is still classified as NPA until it becomes 0 DPD.

- Since Gruh was on INDAS, processing fee on loan was amortized during the tenor of loan. Now we have repaid Gruh borrowing, you cannot carry uncharged processing fee on the books and that has been charged off last quarter. This is one time hit.

General Business:

- Average age of customers with Bandhan in Eastern India is 5-6 years.

- 100% MFI customers’ data is reported to Credit Buereu

- WB growth is 15%.

- Reasons for 20bp drop in NIMS (expect going back to 8% in a quarter or two)

- Excess liquidity of 4500 for entire quarter

- Recognition of NPA for Gruh portfolio. Reversal of interest income.

- Reasons for drop in PCR

- Increase in GNPA largely is on account of home loan book (more on accounting side)

20 Likes

I think there are headwinds for Bandhan at least in near future:

- From my knowledge of Assam (I am from Assam) I feel that the CAA protests are not going to die soon. Not sure if the situation can be compared to demonetization and GST scenarios as shown in latest investor presentation.

- Additionally, with upcoming West Bengal assembly election, there is a risk of increase in clashes between the political parties.

Above two points will have higher negative impact on the segment Bandhan serves.

Disclosure: Bandhan was 10%+ of my portfolio since more than a year. Gradually trimmed from Dec and completely sold out today at overall ~10-12% gain in around 1 year. I still believe in the long term story. Will be happy to re enter at lower levels with better margin of safety!

3 Likes

Regarding CAA protest in Assam, my view is that it will loose it’s intensity with each passing day. Bandhan has already published daily tracking graph for December in INVESTOR PRESENTATION , which shows positive outlook.

Other concern regarding state elections in West Bengal shouldn’t be a major concern as Bandhan or any organization has seen such events successfully in their life time. I agree that these events may have minor impact on operations from current levels. Any correction from current levels would be a good opportunity for long term investment.

Disc: Invested via Gruh at lower levels. views may be biased

2 Likes

Q3 Result Analysis - for subscribers

Disc: Invested

It’s a subscribed write up.based on contents, you could mention the main points

1 Like

Yes you are right on Assam

I am not sure of WB. I have seen multiple elections in WB from my school days, elections are sometimes violent but not violent to disrupt day2day public life. Also this is State , not Panchayat eleciton

I am more concerned with Assam where Protests are still continuing. I have seen how family members got affected during Assam Agitation days in 1980-85. Any Agitation with Social Protest, connected with human emotion, will like to badly affect day2day life

Bandhan has to reduce dependence on WB and Assam, but its’ not easy. These 2 states are 60% of its business now as per latest Q3

Excellent and honest management but people who r invested in MFI, has to bear volatility in Price from time2time

7 Likes

Some points to add from my Concall understanding

CAA and Assam

-

No OTR dip outside Assam

14.2 lac total customer in Assam out of 10.5 M total Customers -

93.5 OTR in Assam end of DEc and improving.

Come to know every week, weekly collections

Conservative side Provisioning done based on OTR

No need to take any extra provision in Q4 and

as for current situation OTR rate, provisions could also be written back in next quarter -

30dpd 556 Cr. Sep 384Cr.

172 Cr. increase - 162 Cr. in Assam only -

200 Cr. provision (3% of Assam book - 6500 Cr.)

162(assam) 30dpd + OTR rate + on field customer interaction,

reversal on provision possible- its net to net provision no haircuts, overall

book loss expected in worst case - customer behaviour is not changing , just that due to bandh

or agitation or curfew on a particular day the group meeting

on the day does not happen and customer is not able to pay

and next day the ratio improves, thus the provisioning is enough

- its net to net provision no haircuts, overall

-

in current scenario, day by day collection is improving,

once people movement comes to normal this will all settle down -

1474 Cr. total deposits from Assam

-

OTR in WB still 98% (45% book) + since 19 years. deep experience

PErmonth Income avg. Rs. 38,000 of ppl in WB

Banks are giving 6 lakh loans, we are giving only 1 lakh

very strong risk team, process, not worried

working on ground level, emphasizing on experience of the team,

customer loyalty intact and satisfied -

lowest otr even on curfew date was 78%

-

Process improvements introspection

-

13 yrs sole lenders in Assam

-

in last 3 yrs other lenders entered

-

in last 1.5 yrs we heard the noise

-

no process changes, thus we are just more conservative now,

our process and systems are robust

Operation Process

-

Ensure KyC and Citizenship Process

avg. age of customer in eastern region is 6-7 yrs, he is

already qualified as a citizen -

Now onboarding strictly on KYC,

Customer Acquisition still healthy at 20% -

total MFI growing 30% and WB growing 15%

Overall customer leverage- process ensuring

Clean data ensuring

- Indebtness all customers on Credit bureau,

Every customer is on Bureau,

but the problem is that the Money lender is not

on bureau

Only reliable source is 1 hr meeting with customers

every week, no data process involved,

probability of risk becomes high

gather info bt customer from both formal and informal sources but still it is a blind spot

Ghosh

- Responsible lender in practise with lowest interest rates of

17.95%, ensuring best value to customer --> works for them - strict 1 customer 1 loan policy, only size increases

once you mature through loan cycles - ensures granularity

So, overall they will be better survivors

Retail Liability

Q

Primary A/C, 4.5 yrs Mass market retail assets

slow. hinders cross sellability.

Float CASA but not cross sell CASA

Ans

Much deeper penetrated in rural and semi urban and a lot of

opportunity

MSME type value accredition for older customers

5-19yrs with bandhan (50% customer base of MFI)

GRUH NPA changes

82 Cr slippage

41Cr. attriutable to A/C recognition change

- NHB til sep: reporting day DPD

- pf beyond 90 days - NPA

- Banking :after sep

pF beyond 90 days -NPA

even if it comes back to 60 dpd or 30 dpd

still classified as NPA

Gruh business momentum

- Integration still WIP from Oct 17th 2019

- Compliance and NPA compliances in progress

- 3-6 months normal growth trajectory to follow

- Focus is on gathering the momentum now

9 Likes

I have gone through both the concalls posted above.let me day that I am not an expert on concalls analysis and banking. It appears to me from concalls that situations is not that bad and would improve in 1-2 quarters. Would request senior boarders well experienced in these fields to share their opinion.

1 Like

I listened today to the concall and went through the notes posted above which capture almost all the relevant details.

My impression is that a lot of recency effect is reflected in stock price. The issues in Assam are fresh in everyone’s minds and we are wired to extrapolate things into the future.

In the concall itself, management said that if situation remains as it was in late December, then the bank is past its worst phase in assam, and no more provisions may be needed.

There has been some effect of 41 crores due to change in accounting policy for processing fees which earlier were amoritised over the tenure of loan but now since all high cost loans of gruh are replaced by funds from bandhan, the amount has to be paid off now as the loans are retired.

Ex of gruh numbers, loan book growth is to the tune of 33%, which in current scenario seems good. NIMs which went down below 8% are likely to come back to 8% plus from next quarter onwards.

All throughout the concall most of the questions raised were regarding Assam situation and further provisions if any going forward.

Bandhan remains one of the long term structural growth stories which is likely to grow in the range of 25-35% CAGR for next few years but it might continue to be plagued with issues like agitation, violence, rural stress and so on and so forth. Long term investors should focus on such opportunities to acquire the stock when newsflow is negative but chances of long term story getting affected are low.

Not invested now but it remains in my watchlist.

31 Likes

Thanks a lot for responding with a detailed balanced view.

Encouraging for many of us to see your interest and assessment @hitesh2710 bhai. Few Qs if you dont mind answering

- Are you able to assess Gruh( home loan) side of biz future growth - most of analysis and con call discussion has been around MF biz and short term issues. Does HFC story take a back seat compared to MF potential

- How would you compare BB vs Manappuram or Muthoot - why should BB command a higher PE even if most of folio is unsecured and prone to many sensitivities - does growth prospects gets highest weightage in valuations( like Bajaj fin a another story built on similar lines on unsecured cons loan at very high growth + demonstrated asset qlty control). Or rather which of these at current valuations would you pick/allocate for mid to long term - your rationale and thought process will help.

- Now that you have BB in your watchlist - how and when you start to nibble it or it is based on next 1-2qtr developments - from your other responses I gather you like to load on way up once bottom is found - trying to understand how would you go about it to if you planned rs X to allocate. A high level mental roadmap/milestones to allocate over time yet deploy effectively to get solid avg cost.

Thanks.

Have BB in my PF from Gruh conversion. Small allocation currently.

3 Likes