The story is simply too good to be true but will give management benefit of doubt. There are lot of risks/challenges ahead. The Gruh merger has to be done perfectly , so there is synergy between 2 sets of employees. The corporate culture could be very different. Moreover, Bandhan now in space of 3 years became a Bank from microfinance company. Now its merging with a sizable NBFC to become a even larger entity. Their business , the way of management, everything has to evolve.

With their valuations, they have no margin for error.

I don’t know the bank rlues,but so far as Bandhan is concerned it was a nbfc since more than a decade ago but got banking license few years before.This may be the reason for more advances than its deposits.

People who are doubting management integrity , please read the book ‘Bandhan- The making of an Bank’ by Tamal B.

The guy has accomplished herculean tasks till date in a country like India with the utmost integrity

Please read.

Disc Invested through Gruh…

yes Integration challenge is there but he has handled much bigger insurmountable challenges in his early days…

5 Likes

Yes, there is no such restriction, the bank would need to borrow from the markets to lend.

Good to see Bandhan exploring new territory ![]()

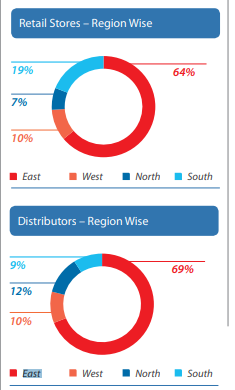

They have tied-up with Kahdim for promotional offers for next 5 months (ending current FY). Considering Bandhan’s strong hold in eastern states of India and Khadim’s big presence (they have 2/3rd stores in Eastern part) in same territory, we can see some traction.

Based on earlier performance, Khadim is expected to have 320cr of sales in balance period of current FY and EAST can contribute 200cr+

1 Like

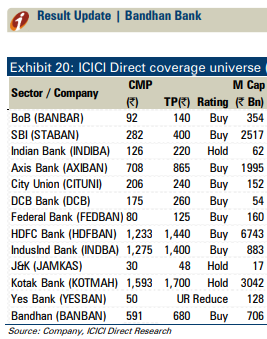

Market_BUY_BandhanBank_ICICISec_30.10.19.pdf (744.5 KB)

1 Like

While its good to see such reports (due to ownership bias) start floating , I could find surprising that analysis for Bandhan is indirectly showing other investing opportunities in Banking space.

If one concentrates on above data, shouldn’t we invest in better opportunities than Bandhan ![]() .

.

P.S.: I hold Bandhan & such reports don’t impact my decision to hold

The present situation in Indian banking is very unique and has come after many years, where we are seeing massive issues in stressed assets which are not going away.

Power, steel, real estate companies had already stressed the bank balance sheets, now even telecom companies are threatening them. In such a scenario, it is important to focus on return of investment rather than return on investment. The more prudent and diversified the bank/financial institution is, the better. In such a scenario, other banks may look optically cheap, but Bandhan has a great past track record as of now. So, better to stick to the proven stories rather than to chase cheapness now.

Disclosure: No holding. A keen observer of Indian banking space ![]()

13 Likes

Its always good to get inputs from seasoned investors like @basumallick. Thanks for affirming my conviction as already mentioned

Your views gave me another angle to look at investments in banking space & raises few questions

-

If telecom hits already stressed banking space & I guess big giants will get affected. It may impact the whole banking space, few may get big slap while others may get nominal warnings (excuse me for using school language)

-

Is it a good exercise to get individual banks exposure to telecom biggies (now we have very less due to JIO affect) and plan accordingly

-

Will it be better to take contrarian view and wait for it (telecom to hit banks) which may provide better entry levels for quite long term investments

Bandhan Bank has decided to stay away from big-ticket corporate lending and would remain happy with its micro loans to small and micro enterprises and housing loans after suffering its biggest non performing asset hit from its exposure to IL&FS.

“We used to always take unsecured exposures. This was an experiment on a secured lending to a AAA borrower which has gone bad,” managing director and chief executive Chandra Shekhar Ghosh said during a media interaction.

We had tested waters with one large corporate account. But that failed. We will not repeat this," he said.

This is a 3 quarter old news which I am sharing again to show mngmnt focus. Gross NPA which increased to 2.4% after IL&FS problem,that is reduced to 1.76% on this quarter report.

Bandhan is expert and market leader in micro/small lending sector and they wish to stick to that business mainly which they are doing with quality since 2001. They are now focussing on affordable housing segment with gruh inclusion,which is exceptionally huge market with government support.

1 Like

Bandhan’s greaest challenge will be 2 things

-

How to repeat East expereince in other parts of countries ? How to bring touch & feel of WB experience in other NEW places

-

Successful merger of Gruh. Merger means merger of Culture, People. Not about systems & process

In #2, Mr.Ghosh’s leadership will be truly tested. In case somebody reads. Tamal B’s book, he is extremely tightfisted,. micro-controlling…But amazing leader who loves to work hands-on…

We know he has given complete freedom…+ give HDFC sold Gruh to Bandhan , Not any other bank, he has Mr.Parikh’s confidence…too.

Incase he can ride over this merger, further rerating on the way. Where he needs to templatize Gruh processes & systems to distant corners of North East…

Story to watch…

2 Likes

Q2FY20 highlights

Gruh merger to add value: The management has selected ~106 branches of the existing 1,000 branches of Bandhan to roll out the mortgage product. (GRUH has ~195 branches).

Hiring and training of employees for the same has started. Almost 50% of the high cost borrowings of GRUH have already been reprised by Bandhan. This was also putting a burden on NIM as both entities were carrying excess liquidity (~`7 bn). Liquidity coverage ratio as of Sep 2019 was at ~225%.

Bandhan management sees no signs of overleverage in any region. Teams visit DSCs/group meetings at least twice a month to keep a close tab. MFI customers are not pushed for deposits as only 5.7% of total deposits are from MFI customers.

Average monthly of MFI customers as per management’s assessment is ~38,000 and the average loan amount is 68,000 with 54% of customers being such that Bandhan is a sole lender to them.

Bandhan has a diversified loan book (larger share of secured loans), adequate capitalisation (Tier I at 23%), reduced cost to income of 30.8%, benefits from corporate tax rate reduction and stable asset quality. It has ample room for growth with opportunities for cross-selling and harnessing operating leverage from existing infrastructure

6 Likes

How is LTCG calculated for people who got Bandhan shares in lieu of Gruh shares? Will the buy date of Gruh shares treated as the buy date? Or will the date we got Bandhan shares treated as the buy date?

It was discussed before also… check

2 Likes

Hi Varun,

Thanks. I am not worried about the grand fathering clause. “Capital gain should be calculated as normal” - I get it. But, what is “normal” here? Is it the date I purchased the original Gruh shares or the date I got Bandhan shares? The difference for us is, we would incur long term vs short term capital gains tax depending on what they consider as the “purchase date”. Therefore the question.

For LTCG, henceforth it will be the date at which Bandhan Bank shares were alloted to you… The purchase price will automatically get adjusted to the Bandhan / Gruh swap price ( based on the rate when you bought it) but the new date for calculating LTCG will be the allocation date.

1 Like

Sir

The purchase date will not be the allocation date of bandhan shares but original buy date for the shares, in this case GRUH… NOT Bandhan allocation date, NOT bandhan-gruh effective date of merger, NOT record date, NOT date of credit of bandhan shares in demat account.

Eg. If you bought Gruh on 1-1-2017, and Sold bandhan bank today 7-11-2019, it will be considered long term investment… All other dates are irrelevant. In case of more than one time investment in Gruh/Bandhan, FIFO (First-in-First-Out) method shall be applicable.

Purchase Date 1-1-2017

Sale Date 7-11-2019

Kindly refer to Income tax law…

Source:

Section 4.4 of the quoted webpage…

Relevant Portions

Allotment of shares in amalgamated Indian company in lieu shares held in amalgamating company – The period of holding shall be computed from the date of acquisition of shares in the amalgamating company.

2 Likes

I think so. It borrows as well other than taking deposits from public.

As per Section 47(vii) of Income Tax Act, the conversion of shares from GRUH to BANDHANBANK is not regarded as a transfer and is not subject to capital gains. When BANDHANBANK is sold, as per section 55(2)(aa), the cost of acquisition is that of the original asset (here GRUH) and as per section 2(42A)f, the date of acquisition shall be of the original asset (here GRUH)

5 Likes