Bambino Agro Industries Ltd. is quite interestingly poised at current juncture :

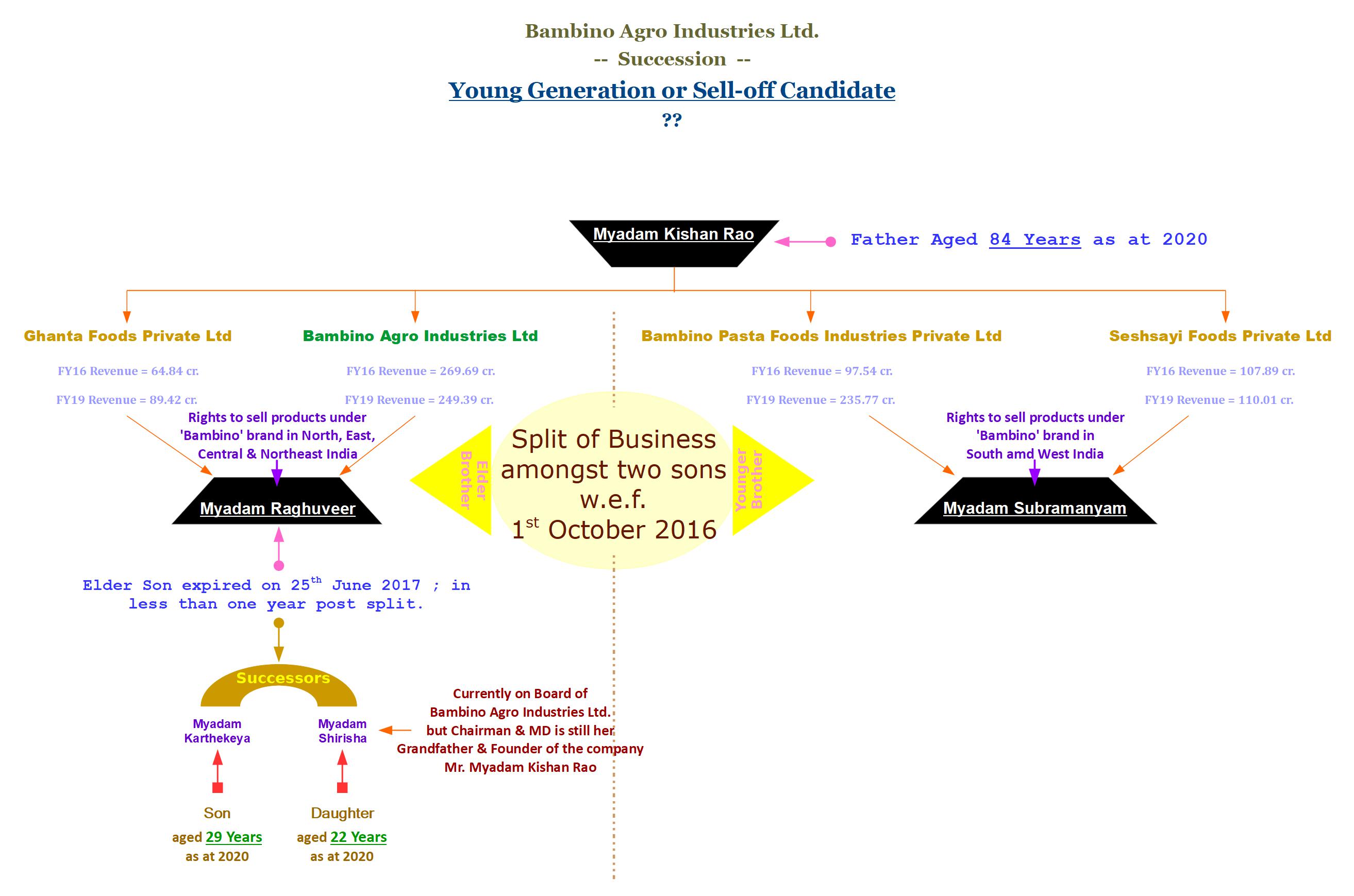

– Succession is the primary interesting point wherein company is going to be run by persons who agewise are in their 20s or otherwise the company is going to get sold off to some strategic investor. Current Chairman & MD Mr. M. Kishan Rao is now 84 years old and before 3 years he executed a business split amongst his two sons as part of which listed entity came under the ambit of his elder son, M. Raghuveer who then passed away leaving behind one son who is 29 years old (as at 2020) and one daughter who is 22 years old (as at 2020). Mr. M. Kishan Rao who relinquished all his active managerial positions from almost all his founded companies (listed & unlisted) subsequent to business split amongst his two sons, was compelled to again become MD of the listed entity (as also unlisted entities which came under elder son’s ambit) post sudden demise of the elder son.

– Company is making all the right moves like capacity expansion, building infrastructure to handle more raw materials, digital marketing of its products, building digital presence in the form of company’s own online marketplace to facilitate consumers to purchase company’s products online and efficient handling and execution of orders placed, introduction of new innovative products, etc. All these initiatives have helped company recoup in just 2 fiscals, almost entire revenue lost due to shrink in target addressable market subsequent to internal business split wherein listed entity was restricted not to sell its products under ‘Bambino’ brand in major revenue generating markets of South & West India w.e.f. 1 st October 2016 .

– ‘Bambino’ brand image is still strong amongst consumers and as an undivided group, the brand still is said to enjoy more than 50 % Indian Vermicelli marketshare and is amongst one of the South East Asia’s largest Suzi-based Vermicelli producers.

– Increasing financial support by the promoters post business split in the form of interest-free unsecured loans wherein 40 % of total debt on books of the company is provided by promoters . This is in addition to high 75 % equity holdings of the promoters in the company.

– Company’s Debt-to-Equity is approaching historically lowest and PAT margins are approaching historically highest with improving revenue trajectory which deserves attention.

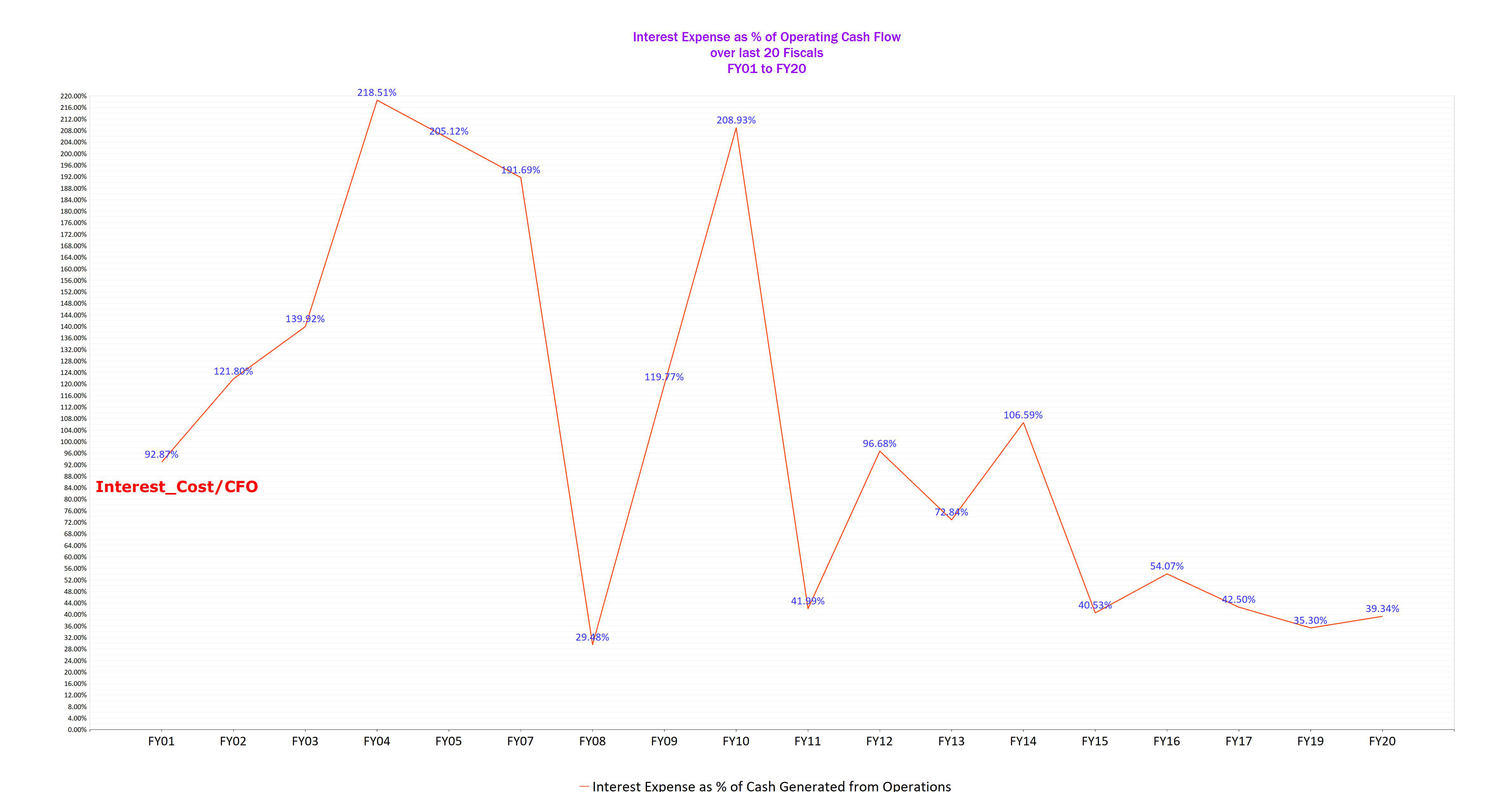

– EBITDA to Operating Cash Flow conversion has been healthy at 20 years’ average 79.74 % which signifies that if business is managed properly it can turn out to be a great wealth creator.

– Company is trading at relatively reasonable to cheap valuation which is a rarity amongst its peer group.

However, as an investor who is looking at analysing this company, there are also some questions that come to mind ; after finding answers of which we can weigh positives and negatives judiciously ; such questions are :

– Revenue growth, although linear but is sluggish ; 20 years’ CAGR (FY01-FY20) is just 5.5 % and if we take into consideration internal business restructuring which took place in FY17 then too going back 20 years from that period its just 6.2 % (FY96-FY16).

– Relatively high debt and interest payment eating up entire cash flow . Operating Cash flow (OCF) generation, although healthy at 20 years’ average 79.74 % of EBITDA, high interest cost eats up almost entire cash flow generated with 20 years’ average interest cost as % of OCF at 103.22 % . 20 Years’ average External Debt-to-equity is at 2.05x wherein we have not considered interest-free loans of promoters. Including such promoters support, 20 years’ average total debt-to-equity comes at 2.26x. Any smartly managed company would have not wasted Cash generated on such high-cost debt over these many years

– Although the matter is quite old, but promoters involvement in Spectrum Power Generation Ltd. controversy is also another point we need to pay heed to.

Having enumerated positives and negatives above, it is time to look at actual facts and numbers :

Succession :

Let’s first have a brief look at Succession issue that we talked about before. Refer following :

Mr. M. Kishan Rao executed a business split amongst his 2 sons w.e.f. 1 st October 2016 under which listed entity Bambino Agro Industries Ltd and unlisted associate company Ghanta Foods Ltd came under the ambit of elder son Mr. M. Raghuveer. Mr. M. Raghuveer passed away on 25th June 2017 leaving behind his wife, one son who is 29 years old as at 2020 and one daughter who is 22 years old as at 2020. Due to sudden demise of his son, Mr. M. Kishan Rao again resumed the responsibility of Chairman & MD of listed entity (as well as associate Ghanta Foods). Only the young daughter M. Shirisha is currently on board of listed entity from Mr. M. Raghuveer family.

Considering the age of Mr. M. Kishan Rao, having completed 84 years on 10 th February 2020 and approaching completion of 85th year in 3 months from now on, it is but obvious that either the company will now be actively managed by his young grand daughter M. Shirisha who has just completed 22 years of age in October 2020 or there will be a sell-off of promoter holding in favour of a strategic investor who can run the company from now on. Mr. M Raghuveer’s son, who is 29 years old, doesn’t seem to be interested in the business as otherwise he would have taken some active managerial position or directorship in the listed or unlisted entity post demise of his father.

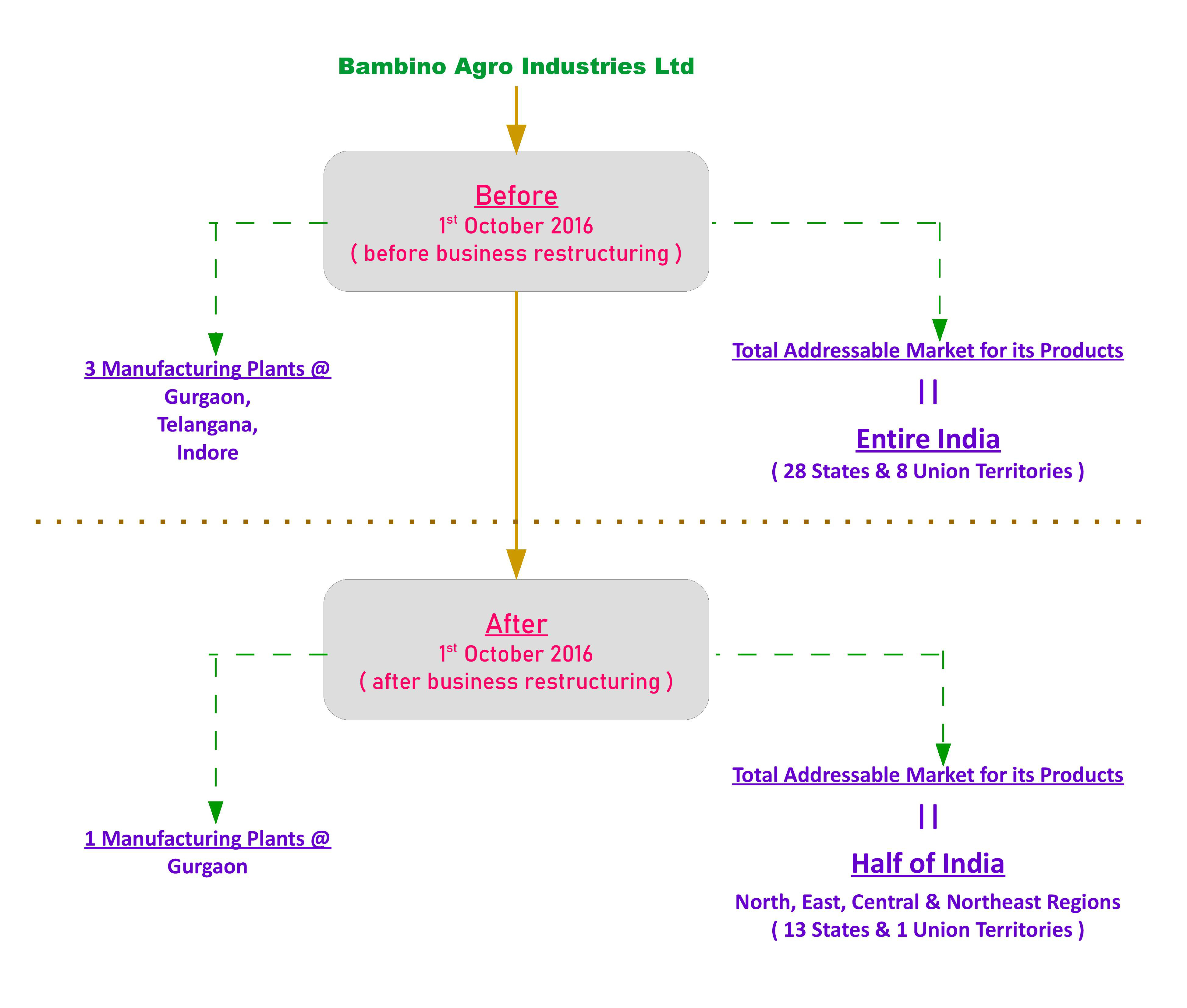

Listed Entity Business Scope post Business Restructuring dated 1st October 2016 :

Kindly refer following :

As said before, Mr. M. Kishan Rao executed a business split amongst his two sons under which listed entity came under the ambit of his elder son Mr. M. Raghuveer. As per the terms of the said business split/restructuring, w.e.f. 1 st October 2016, listed entity was restricted to sell products under ‘Bambino’ brand name in only North, East, Central & Northeast regions of India whereas the rights to sell products under ‘Bambino’ brand in South & West India went to the younger son Mr. M. Subramanyam’s entity Bambino Pasta Food Industries Pvt. Ltd. Alongwith the said rights, there was also transfer of 2 manufacturing plants from listed entity to Mr. M. Subramanyam controlled entities .

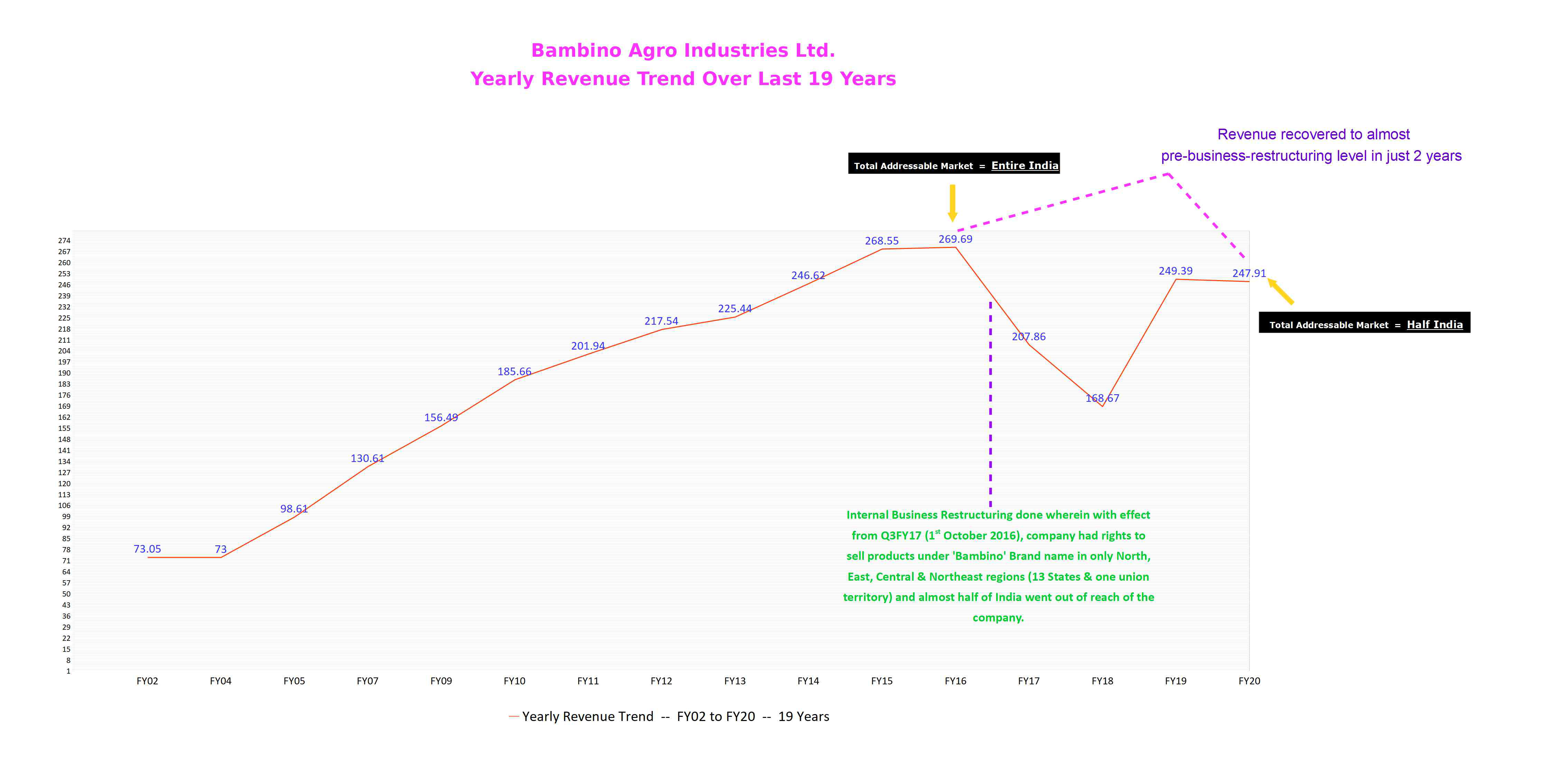

Revenue trajectory of listed entity over last 2 decades :

Kindly refer following :

Here, in order to enable us to compare in a proper way, while analysing revenue trend over last 19 years, we have considered each fiscal-ending to be 31st March only by extracting data from quarterly results of each respective fiscal where year ending in ARs was other like September or June.

– Company has recovered in just 2 fiscals, entire revenue lost post business restructuring in FY17.

– Company seems to be in the right direction towards the goal to achieve healthy revenue growth over coming fiscals which is evident from the recent steps taken by the management like :

replacing current machineries with more advanced ones (in FY21) which can enable higher output (~20 %) ,

expanding capacities (~50 %) under associate Ghanta Foods whose products are sold under ‘Bambino’ brand by listed entity,

building two silos (in FY21) to handle increased RM,

starting its own emarketplace (https://shop.bambinoagro.com/) w.e.f. June2020 during the lockdown phase so that consumers can directly buy online and get their products home-delivered,

efficient handling of orders placed at its eportal wherein despatch time is just 24-48 hours and products are well packaged and delivered by reputed courier,

increasing digital presence like on facebook, instagram, twitter, etc.

introduction of many new products like Ready Mixes, Spices, Namkeens, Sweets, etc. in addition to its stronghold Vermicelli & Pasta products.

It is heartening to note that even after business restructuring (shrinkage in total addressable market, transfer of manufacturing plants) as well as a big setback in the form of sudden demise of its leader within just 1 year of business restructuring, company has remained active on all fronts (infact more than before) and has not gone in stealth mode which is normally the case with any entity in similar situation.

Quarterly Revenue Trend over last 2 Decades :

Kindly refer the following :

Q2 is always strongest relative to other quarters. Q2FY21 has seen highest quarterly revenue being posted by the company .

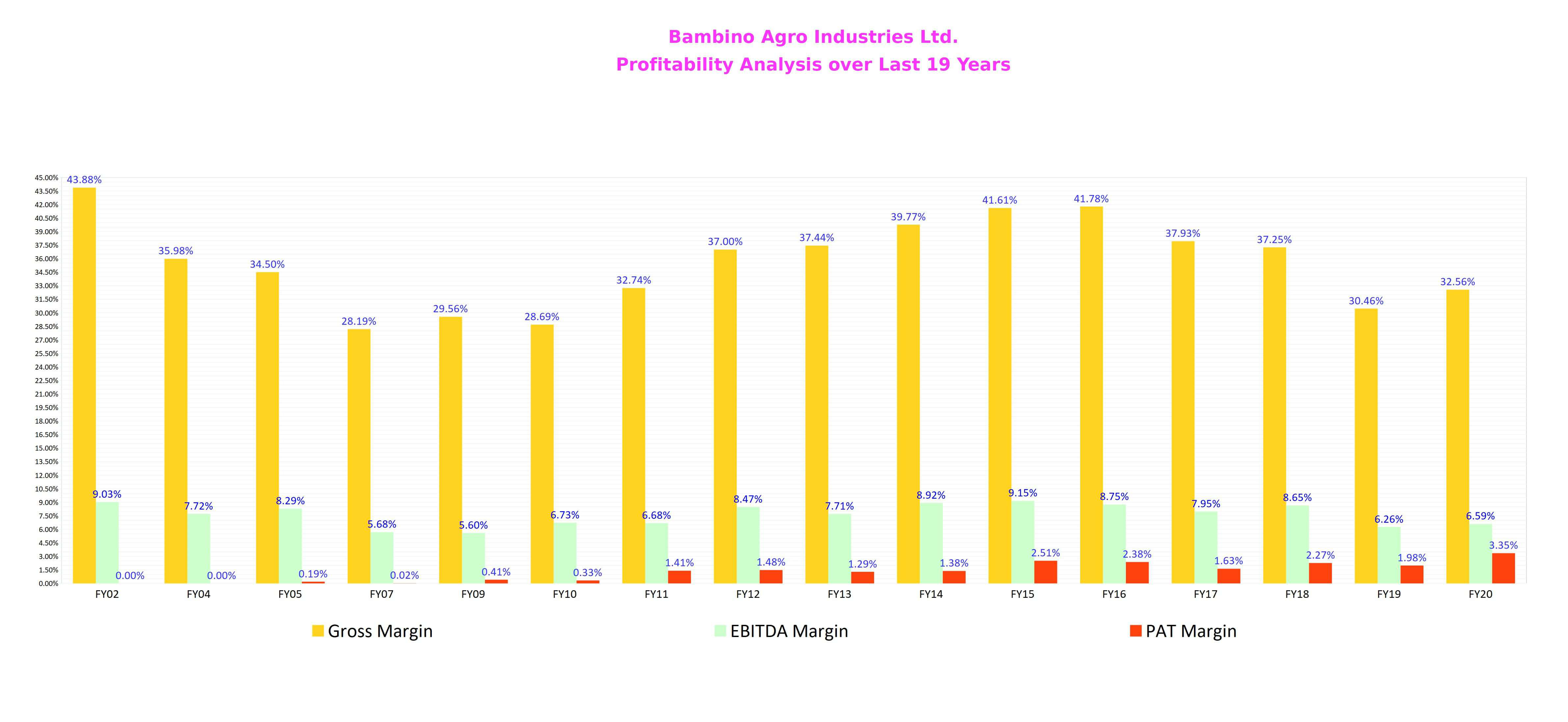

Profitability Analysis :

Kindly refer the following where Gross, EBITDA & PAT margin trend over last 19 years is depicted :

RoE & RoCE trend over last 2 Decades :

Kindly refer the following :

Company’s RoE, from negative till FY04, has exhibited a continuous improvement since FY11 and is currently standing at a reasonable 13.68 % as at FY20 .

Cash Flow Analysis over last 2 Decades :

Kindly refer the following :

EBITDA to OCF conversion is reasonably healthy at 20 years’ average 79.74 % and 10 Years’ average 80.47 % which simply means business has been able to generate very good cash flows which, if used judiciously, can create a good amount of wealth for investors. However, for that to happen, management has to learn to balance equity and debt. For example, lets analyse the period post the company reaching One Time Settlement (OTS) with its lenders in FY08 to come out of financial mess resulting out of high debt (D/E FY07 = 3.66 with absolute debt of INR 66 cr. on revenue of 130 cr.) :

– company has been operating at tiny equity capital of just 8 cr. over last 13 years (FY08-FY20) with promoter holding at 75 %.

– This is despite Revenues and EBITDA growing almost 100 % over the same period and the brand of company getting relatively stronger with introduction of multiple new products over the same period.

– Absolute Debt on Books has increased from 52 cr. as at FY08 to 75 cr. as at FY20. However, external debt , that is, debt other than from promoters has remained same with FY08 External debt being at INR 43 cr. and FY19 External Debt at INR 45 cr… Promoters’ financial support extended to the company in the form of interest-free unsecured loans has increased from INR 9 cr. in FY08 to INR 30 cr. as at FY19 .

– Absolute Operating Cash Flow generated over the said period stands at healthy INR 166.24 cr. . For a business with a scale of around INR 250 cr. p.a., to turn out OCF to the tune of INR 166 cr. over a 13 year period (FY08-FY20) is commendable and if this cash flow is managed judiciously then it could help the business grow well without much external support.

– Now, let’s look at the other side of the coin — the interest cost part — over the same 13 year period (FY08-FY20), company has used INR 109.47 cr. of OCF to serve its debt (interest payment). In other words, 66 % of OCF is used to serve external debt .

– Use of OCF for CAPEX over FY08-FY20 is just INR 67.42 cr., or, in other words, 40 % of OCF is used for CAPEX which is meant for actual business whereas 66 % of OCF is used to serve external debt .

– An efficient management would have put serious thought about this and either replaced the existing high cost debt with low-cost one or would have raised equity to retire debt and make business self-sustainable.

Debt-to-Equity (D/E) Trend over last 2 decades :

Kindly refer the following :

Here, ‘Total Debt’ refers to total debt on books of the company which includes financial support extended by the promoters in the form of interest-free Unsecured Loans. ‘External Debt’ refers to ‘Total Debt’ minus promoters’ interest-free financial support.

We have here looked at D/E in two parts because :

– to assess real leverage position of the company, we need to look at External Debt closely,

– post business split/restructuring, promoters have extended significant financial support to the company which can’t be ignored as in addition to this financial support, they also have 75 % equity holding in the company.

– As we can seen from the above, before company reached OTS with its lenders (FY08), company’s leverage position had deteriorated significantly with Total D/E touching 3.66x & External D/E touching 3.44x.

– Post OTS, there was increased financial support by the promoters in the form of interest-free Unsecured Loans which increased significantly post business split/restructuring which is evident from wide gap between Total D/E and External D/E .

– For the first time ever in past 20 years, External D/E has fallen below 1 (0.83) .

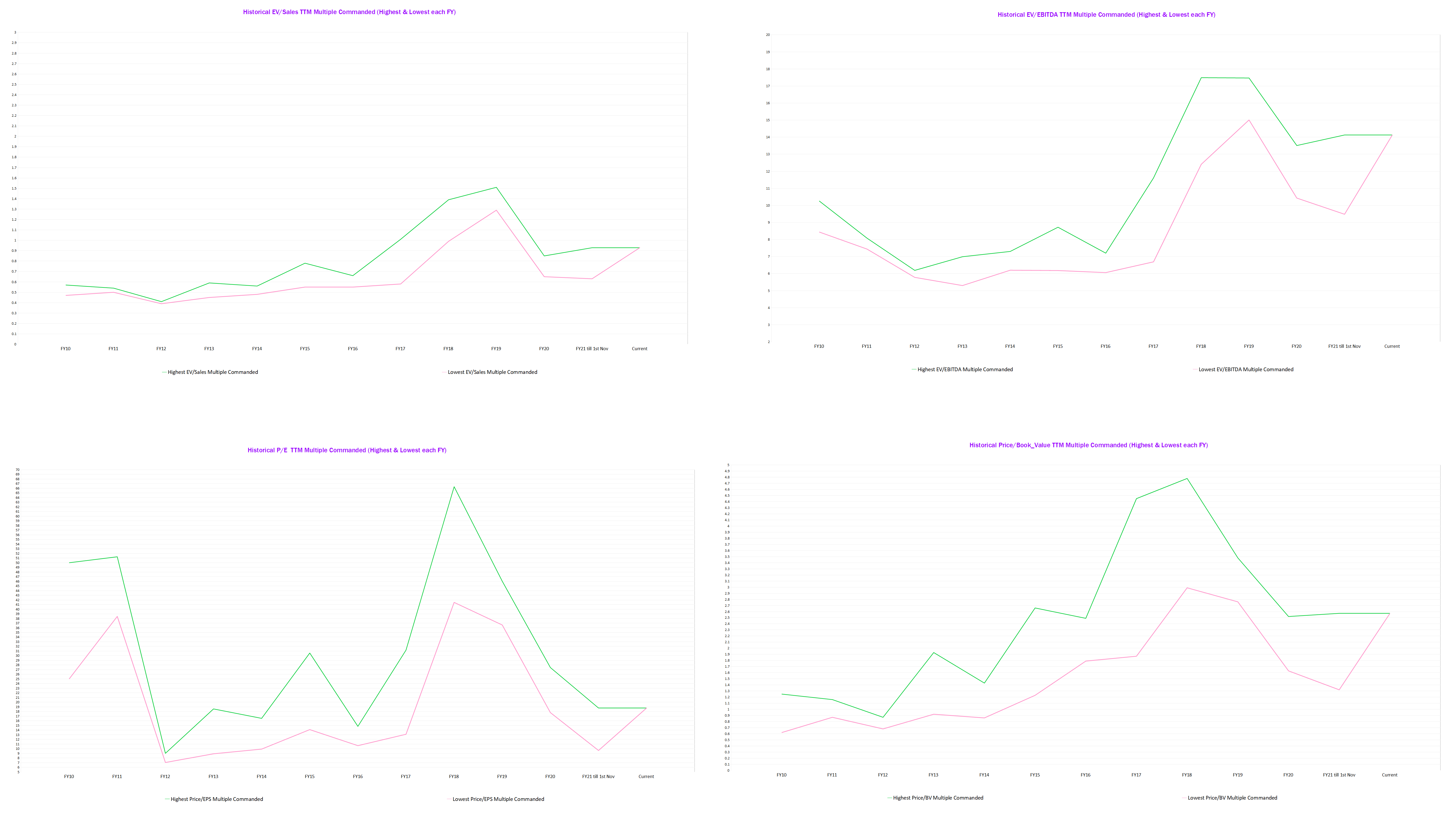

Valuation Commanded by the company on the Bourses :

Kindly refer the following :

EV/Sales multiple around 1x and P/E multiple around 20x is a rarity in company’s peer segment, especially when :

– brand is strong in consumer’s mind,

– company is innovative in both, introducing variety products and efficiently reaching to consumers,

– D/E is at its historical bottom near to 1x,

– Average OCF each year is near 70 % of EBITDA,

– CAPEX incurred in any one fiscal is at its highest.

However, as is rightfully said, markets are always right and therefore there might be some genuine reason(s) for such low valuation commanded by the company ; some reasons are already cited in the beginning like :

– sluggish revenue growth,

– relatively high debt and high interest payment,

– key founder involvement in controversy surrounding Spectrum Power Generation Ltd.,

in addition to these :

– ‘Bambino’ brand being registered under ‘M. K. Rao Family Trust’ and not under listed company,

– high Related Party Transactions,

– lack of many minority shareholder friendly actions by the management,

– dismal Investor communication.

Despite all these reasons, as investor we need to keep monitoring closely each and every development with regards to this company because :

– Company is at the cusp of management change ; either it could be internal with it getting passed to younger generation or it could be external with company being acquired by a strategic investor ;

– reasonable growth visibility with historically highest CAPEX being incurred by the listed and unlisted entity (under same management) ;

– proactive moves on-ground in the form of increasing digital presence with company’s own shopping portal being started from June2020, increasing presence of its products in organised modern retail formats, increased digital marketing, introduction of multiple SKUs, etc.;

– history of high EBITDA-to-OCF conversion with average standing at 70 % + ;

– historically lowest D/E and therefore highest PAT margins ; and,

– above all, in case of faltering, promoters will be ultimate loosers with them holding 75 % equity holding in the company in addition to INR 30 cr interest-free loans extended by them to listed entity.

Discl.- Invested

Note :-

This is not a Buy/Sell recommendation of any kind but is only representation of facts and figures to take it as a direction for further industry analysis. Hence, it should not be taken otherwise and should only be used for deep study of the segment and peer group. This is part of a discussion and is only aimed at stating statistical facts & figures for further discussion.

pdf of the writeup attached for members’ reference :

Bambino_Statistical_Study.pdf (4.9 MB)