Agree @meditate that mkt share gains stays aspirational and a moving goal post.

In the absence of a third party credible report on mkt share, not sure how much weightage to give it. mkt share alone is however is not a prime aspect in my view as long as good growth is delivered.

Here is competition JFM qtr results and commentary

Replacement and off road segment seem to be doing well per above - key focus for BKT as well, price hike augurs well for BKT as in Q3 they did mention that future price hike is basis comepetetive scenario, ket monitoable given margin hit in last few qtrs.

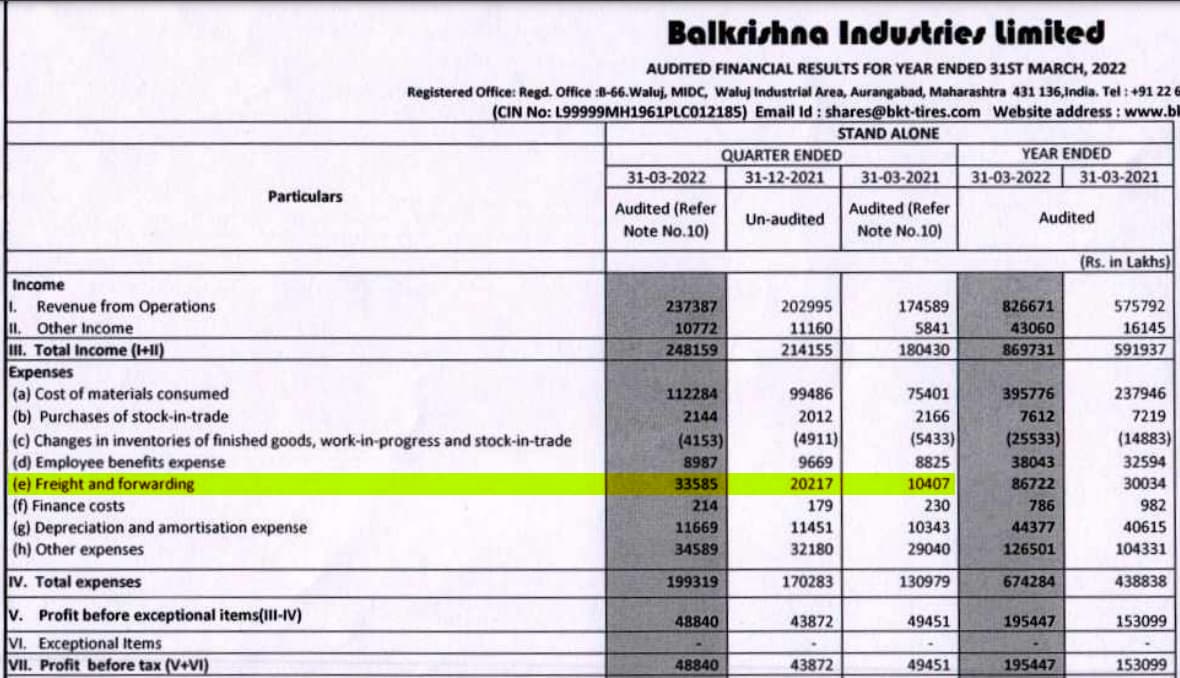

Inflation has taken a heavy toll on BKT this quarter. While the core revenue growth is ~36%, the operating profits have degrown by 1%. Volume growth strong at 13%

PBT margins are down from 28.3% to 20.5% YoY

Freight costs have gone up from 8% of the total expenses to 17% for this quarter (was 12% in the last quarter). Guess they have done reasonably well on the raw material front, will have to wait for the management commentary! The oh so criticized backward integration of carbon black looks sensible in hindsight

Old Waluj plant revamp capex (350 crores) on hold. Management says this is done to facilitate quicker production schedule demanded by end customers. Volume addition from this was seen at 25000MT p.a

Volume achieved for FY22 - 2.89 lakh MT (exceed expectations)

Revised volume guidance for FY23 stands at 3.2 lakh -3.3 lakh MT (was 3.6 lakh MT)

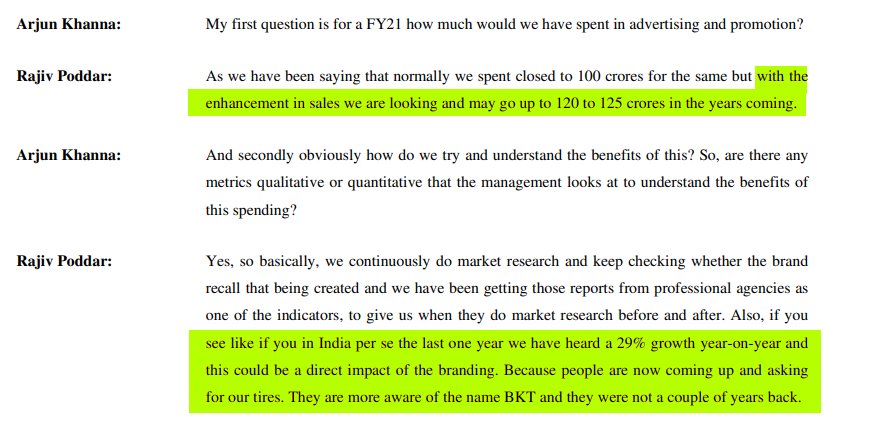

The management is of the opinion that the growth in India is due to the recent spending on brand-building (IPL predominantly).

During the last year’s IPL, they had invested in the electronic billboards inside the stadium but this year they have gone further and have tied up with eight teams (excluding CSK and RR).

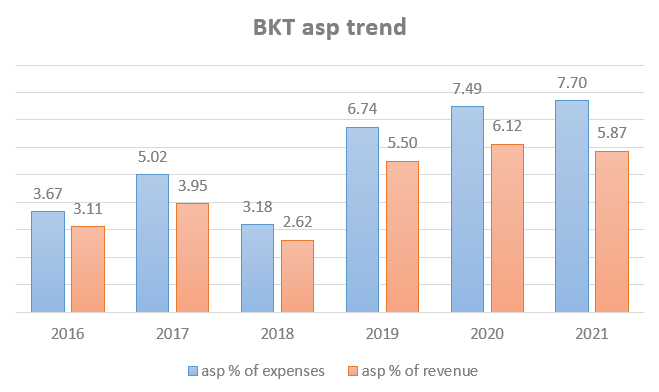

A quick look at the asp spends for the past six years shows that they have increased from 3% to 6% of revenues

As our geography contributes less than 20% of the overall pie for BKT, the incremental growth is coming at a high cost. Well… this is at least better than banking everything on Sunny Deol

Hello @Dev_S

Share price is more than 20% down from it’s high , any specific reason , even when all tyre companies are performing reasonably well. How badly its revenue will get impacted do to recession in Europe??

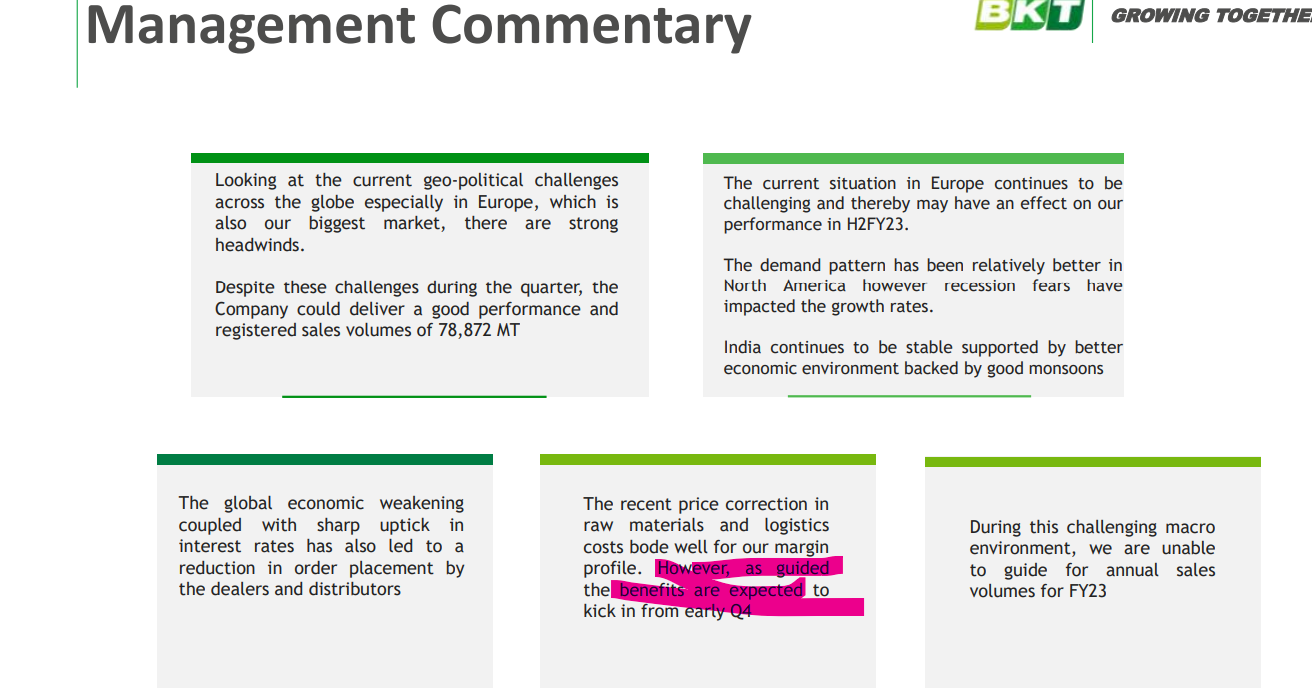

Answer likely lies in Q1 commentary, where in falling rubber prices would see some destocking + slowdown in EU etc, and some impact on Q2 though margin should improve H2 onwards helped by lower freight. My sense is that subdued commentary and regular newsflow from EU on drought/ inflation/ economy challenges have given enough reasons to market for treating them the way most EU facing companies are.

While things may improve from Q3 onwards here on for BKT atleast on margin front but we will have to wait till price action or mgmt commentary comes in, markets are more focused on rewarding local tyre mfg companies where end auto industry is showing signs of strength.

RM cost has gone up. In last con-call, management guided that it will remain high until Q4 atleast. They have forward contract rates with RM suppliers till Q4, so even if cost drops for industry, it will not benefit BKT till Q4 when they will be able to revise the rates.

Europe is going through their biggest drought in last 500 yrs. This has direct impact on farming and therefor on tractor sales. This is expected to impact BKT - new as well as replacement demand.

Market seems to be reacting to this pressure on both demand and supply side.

Request to guide about one query.

While reading Annual Report of Fy22,I came across the investment of BKT in unquoated shares of NSE Ltd and Care insurance co. And also preference shares of Tata capital and some other companies. Since these investments are unrelated to the core business of BKT, why they must be holding these shares? And are they allowed to do so? What must be the rationale behind it?

Horrible numbers posted by BKT. As expected market reacted and beaten down the stock by 11%. I think it will see at least 40% downside from 52 wk high,to justify this numbers. Continuously margins are falling for last 9 qtrs. To me management is quite impulsive, from the day they reverted back the US plant decision few yrs back, I was keeping a close eye on this company. Later they proved their impulsive decision making flaws,by reverting back few expansion plans in India too. Company can’t do core business but their other expense up 12% qoq. Most of them I guess addvertisement and sponsorship for players jersey.

Mgmt looks very evasive in its responses in the concall. Not much attempt to clear the doubts on analysts. Pain will continue in Q4 also. Also they are not giving any guidance for FY 2024.

We need to see the comments of mgmt on Q2 , highlighting too

Sponsorship of some sporting events really baffles me. Had written to investor desk to understand the rationale behind these sponsorships and how it will drive sales. They asked for my number to discuss on phone and never called back.

One thing I have learnt the hard way is never rely too much on management commentary…when times are good, all managements are super bullish, so when negative surprises in results come they really hit hard…doing ones own due diligence and developing independent understanding of business and its key drivers is more important as per me.

After reading the concall notes, nothing much negative is observed. Or no drastic change in business direction. Still share price tanked more than 10% in two days. Why so much over-reaction?

Share price moved up from 19th to 26th May in anticipation of great results…but results were tepid hence market got disappointed and gave up all the gains

Mgmt in last year AGM: “In the first half of the seventh decade, we are now embarking on a mission to double our global market share from ~5.5% to 10%”

They have remained “rock steady” in their “embarked mission” since many years, let us see where they stand this year.

Even if market is shrinking they should be able to gain market share right? In fact in down turns it is best time to try and gain wallet share if they actually have a right to win since that is when people will be more likely to switch from incumbents.