Raw material dependence on China – 10-12% which is mainly for backup purpose, can substitute easily by another vendor of another geography if need be

as per 4q20 concall notes i have with me

Raw material dependence on China – 10-12% which is mainly for backup purpose, can substitute easily by another vendor of another geography if need be

as per 4q20 concall notes i have with me

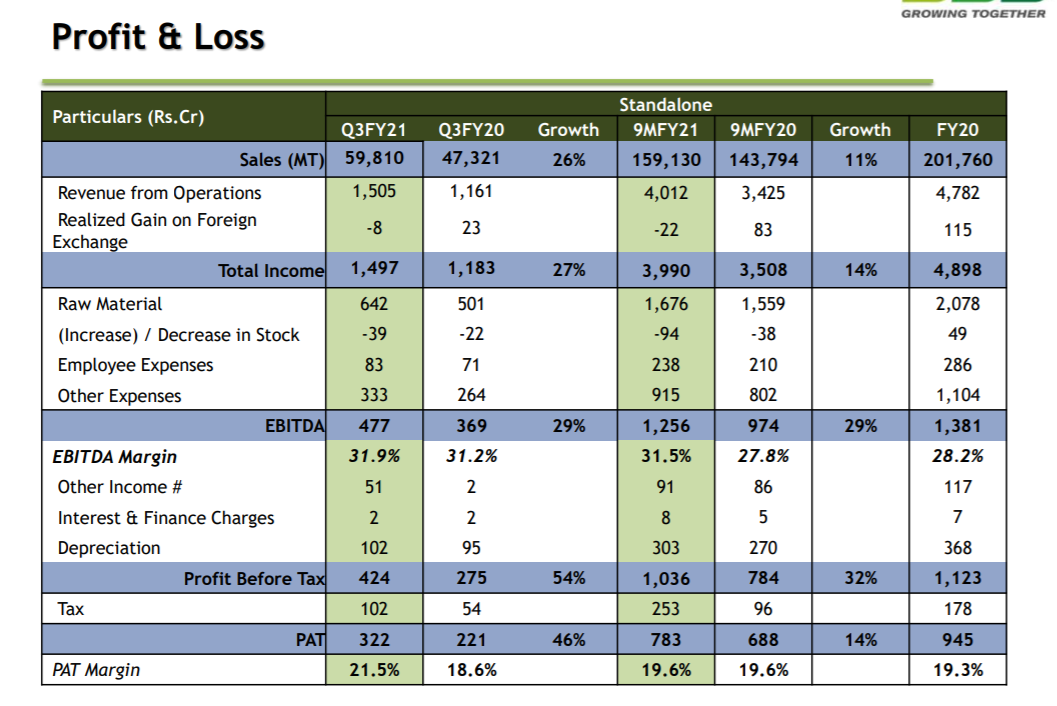

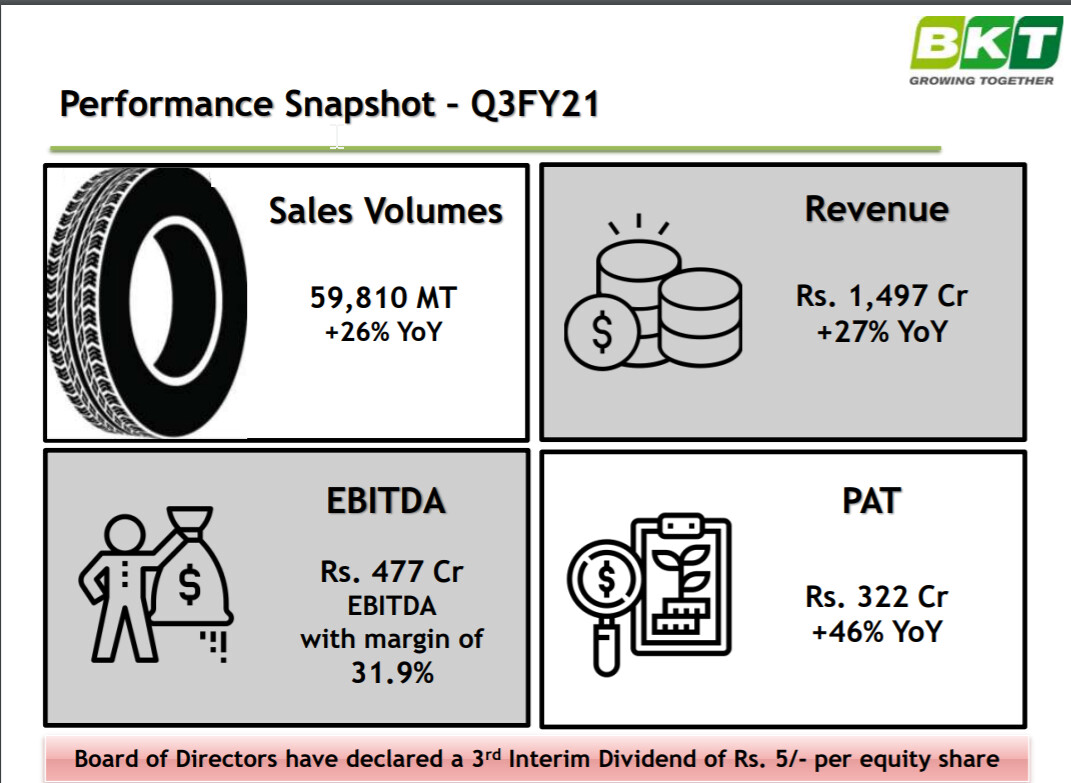

Very strong results continued from Balkrishna.

EBITDA grew 101% YoY at Rs 5.37bn with margin at 34% (+902bps YoY; +917bps QoQ).

Revenue was Rs 15.79bn (+32% YoY)

PBT came at Rs 4.5bn (+76% YoY)

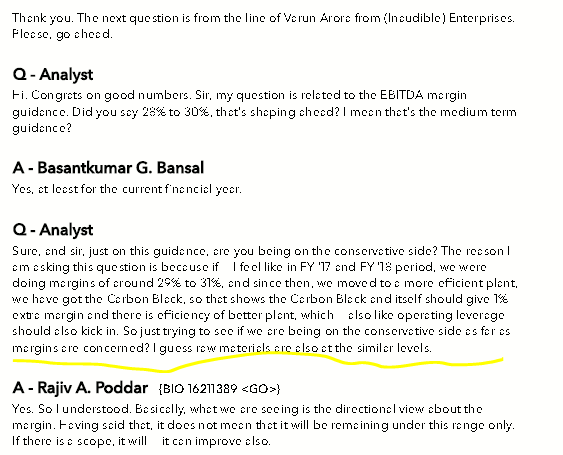

Not surprised with the margin performance. Felt the guidance was not reflective of the changes the company has made and the current RM prices as long as normal operations continued. Had clarified the same with the company in Q1 call.

Balkrishna Industries has posted another brilliant set of numbers this quarter, margins are intact at 31%! It looks like the company is on a roll and is seeing good demand in the agri side

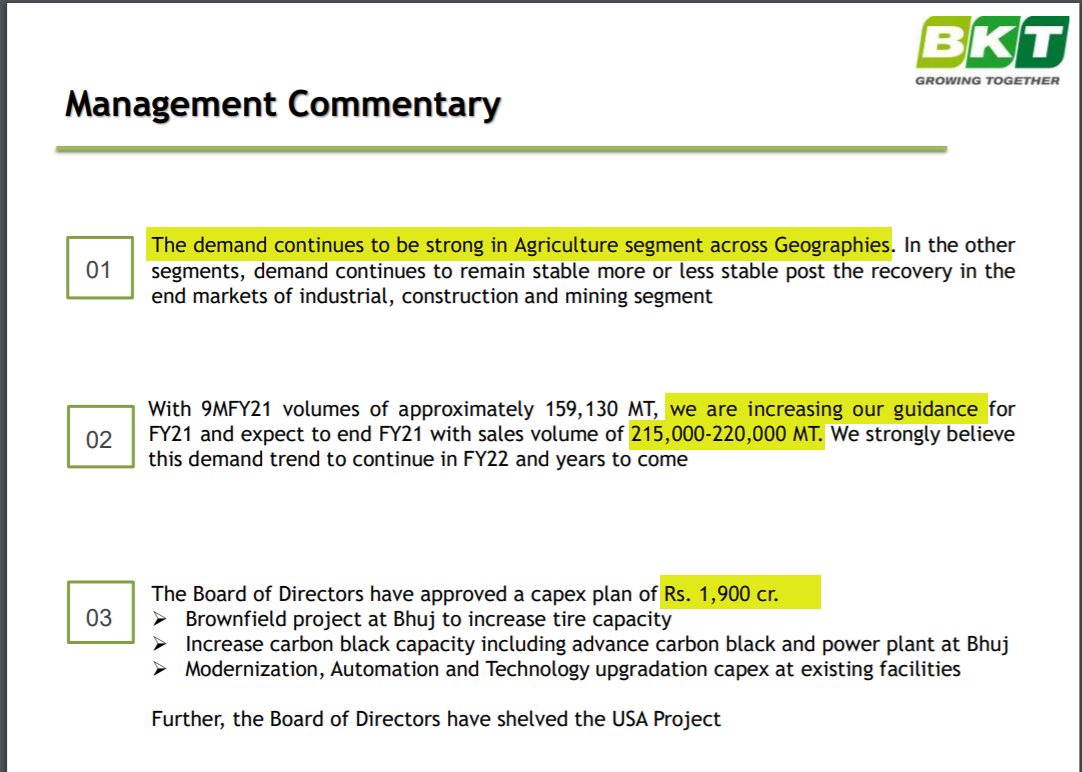

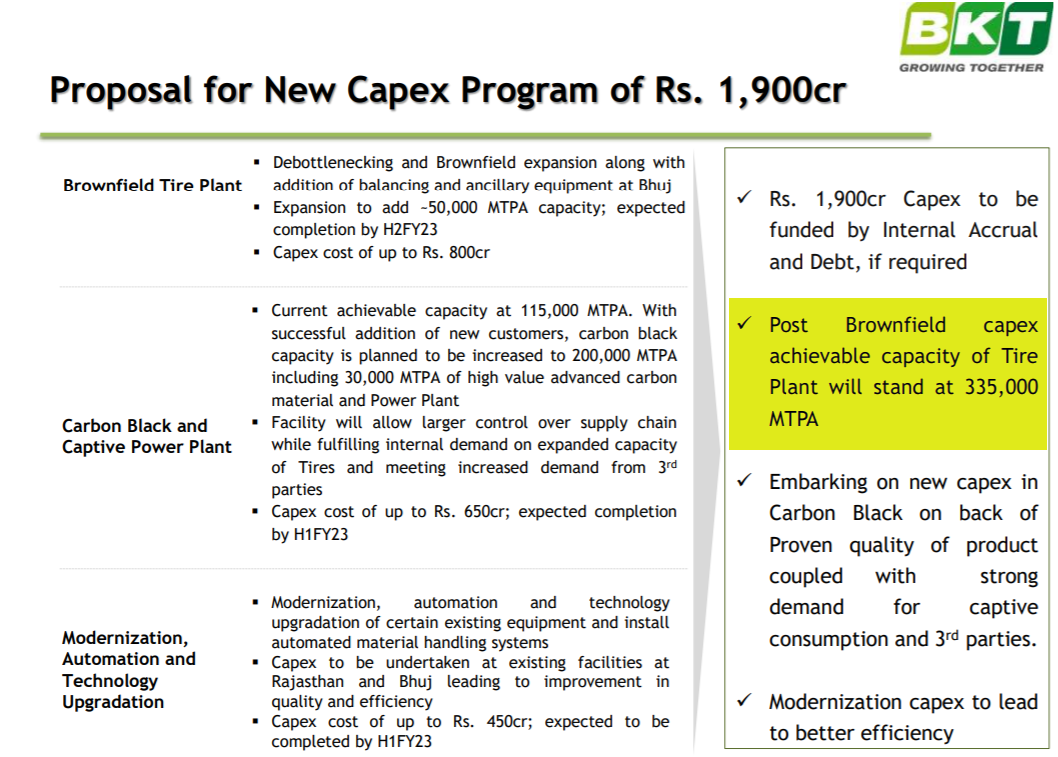

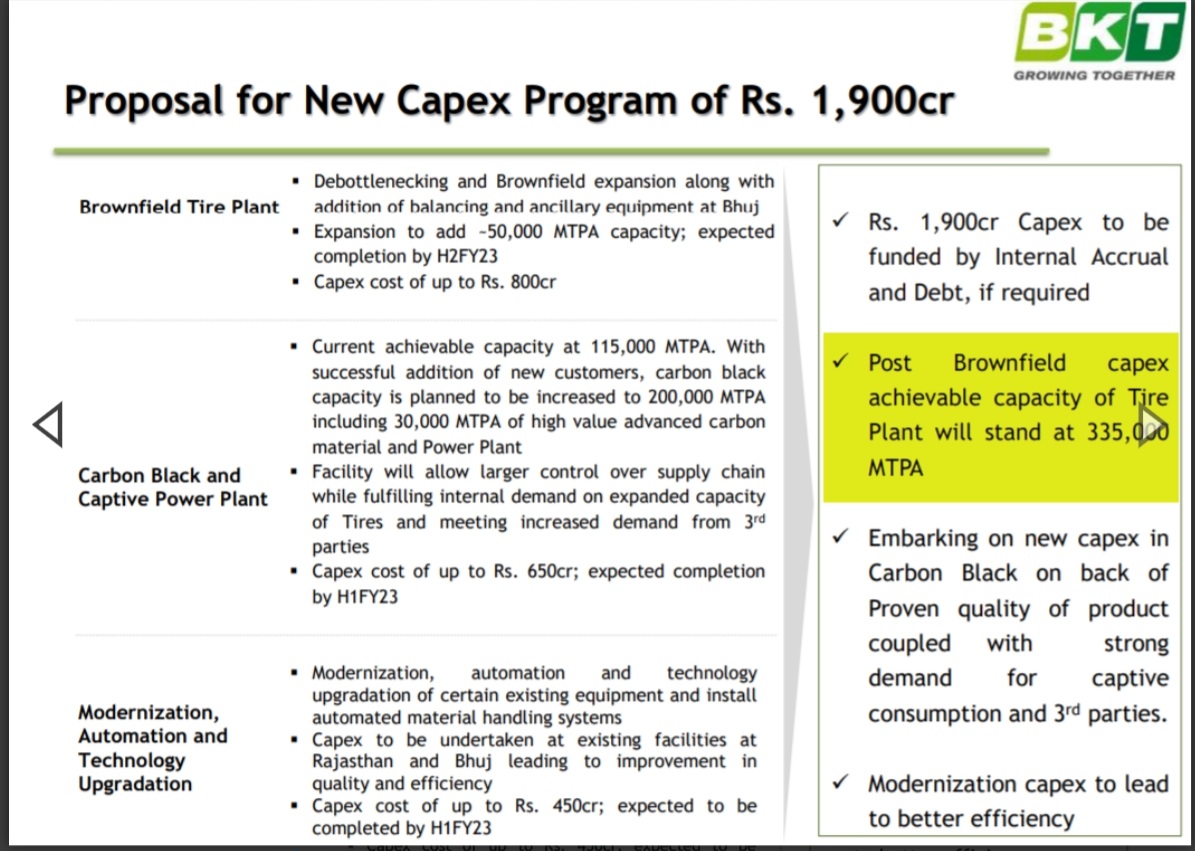

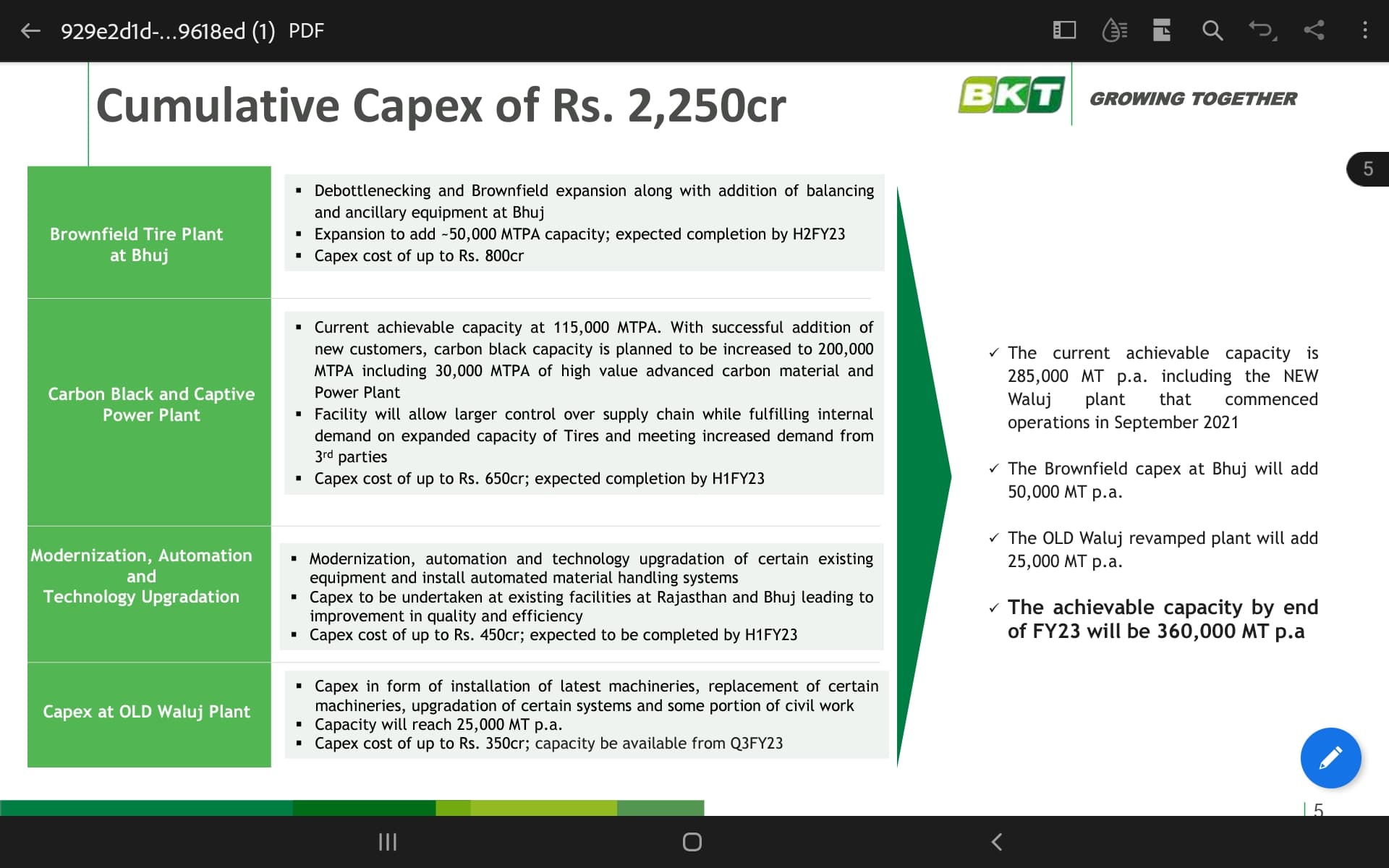

Management commentary is ultra-bullish and the co has announced a massive 1900 crore capex (all of which is expected to be completed by 2023). Note - The US project is shelved

Capex proposal: ![]()

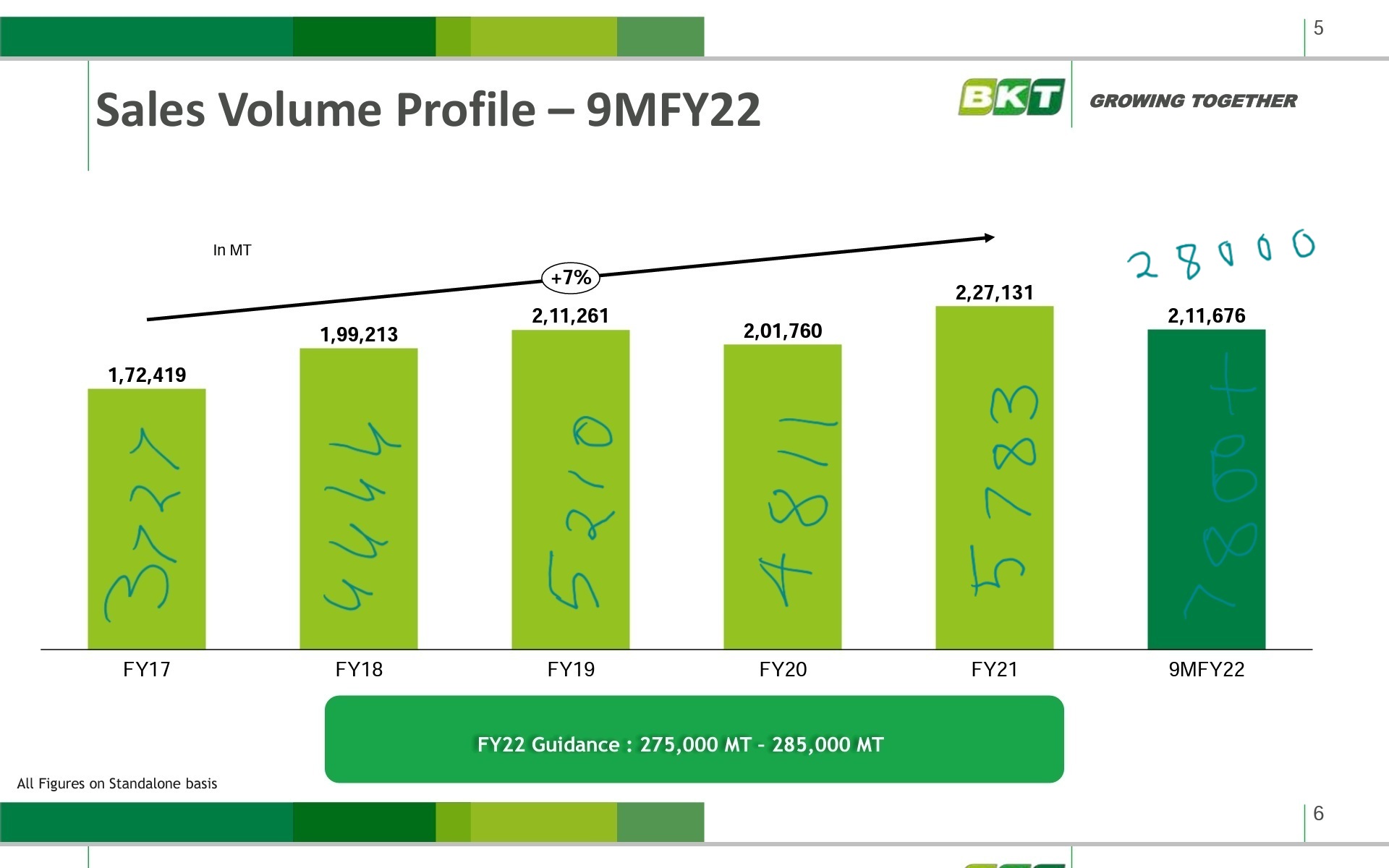

Expected volumes for FY21 is ~2.15 lakh MT and they expect the total capacity to be at 3.35 lakh MT once the brownfiled capex is achieved. I believe the current capacity is at 2.85 lakh MT

Results look great YoY, but negative for QoQ. Is that the reason for negative reaction of the market, and another cause could be shelving of US project? I know market can be irrational, for a person averaging down this is a great opportunity yet the fear about retail investors not knowing something that market knows.

The usual dilemma!

Hi Vinay,

A naive question may be: if the current capacity is 2.8 lac MT, and in the current robust demand and growth phass they expect to end the year with estimated 2.2 lac MT, then why is a need for capacity expansion? Their existing capacity is still not fully used. Pease help me understand, still learning.

Regards

Yogesh

Hi Yogesh,

On the outlook, 2.8 lakh MT looks like excess capacity for BKT since they’re only

clocking 2.2 lakh MT pa but there are multiple reasons for a company to operate at less than the achievable capacity. The most common reasons being:

In that case, why are they increasing capacity?

hope I was able to add some value

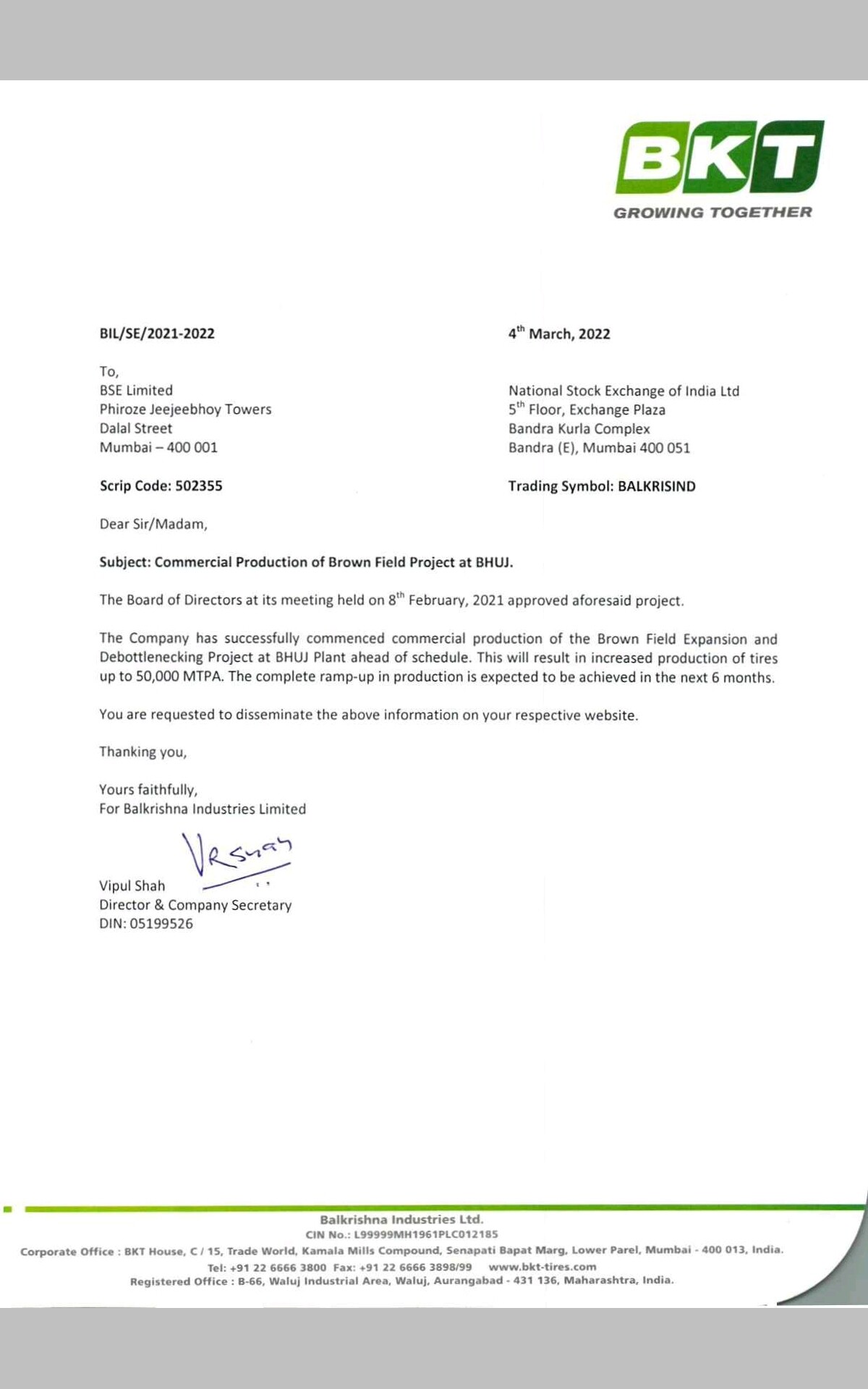

Balkrishna Industries Q4FY21 Concall Update

High capex towards modernization and expansion in carbon black to weigh down on return ratios in near term

Outlook: Positive

• Co has guided for sale of 250-260k tons in FY22.

• Capex for FY22 will be at Rs. 800-850 Cr.

• Project for ultra large tyres at Bhuj has completed and is in the final trial phase.

• Co is running at full capacity in carbon black on existing capacity at 115k tons.

• Carbon Black plant’s capacity has now increased to 140k tons and sales to 3rd parties has started.

• The greenfeld plant at Waluj for replacement tyres with 30k tons capacity saw a temporary shutdown in March but commenced again in April and now is expected to be completed in Sep’21.

• The company has long-term margin estimates of 28-30%

• The company had prices hikes of around 3-4% in Jan’21 and Apr’21

• The company had witnessed a raw material price increase of 2-3% and expects it to be around 5-6% in the coming quarters

Break up of Rs. 1900 Cr capex plan

Most of the capex will be funded through internal accruals and some debt will be taken.

Share is trading at P/E of 28.9x FY22E EPS

Majority of institutional shareholders voted against the reappointment of Arvind Poddar as MD & Chairman.

High salary of the CMD is reported in this news article.

Another news article connects the CEO compensation with the Institutional Voters being unhappy.

Per management stand, Capex to be funded by internal accruals, and debt if required

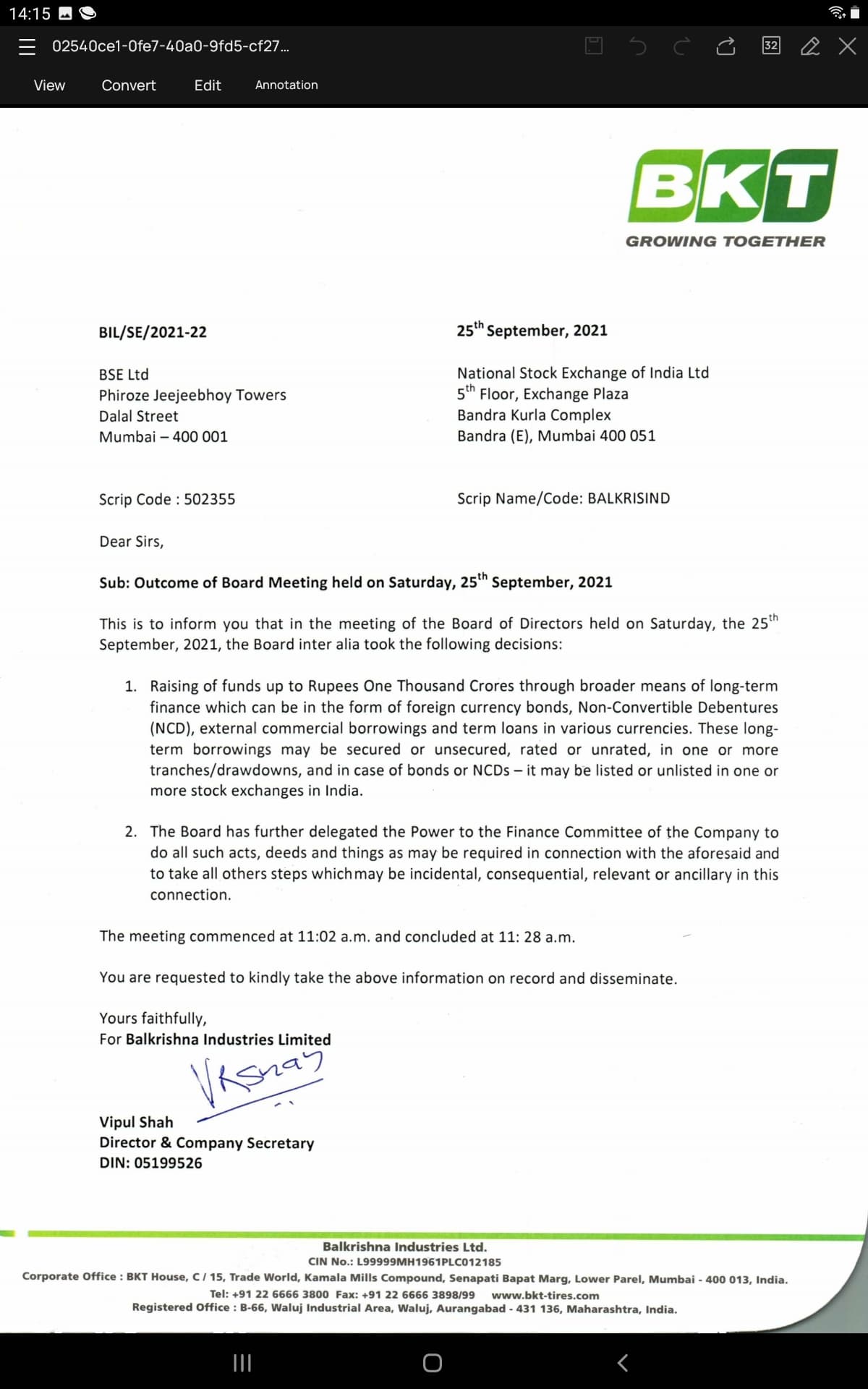

1000 Cr fund raising announced

Not connecting above two but management has its unique ways to drive execution, even at cost of being little bit unpredictable/inconsistent. Carbon back Part of Capex itself was a controversy when announced.

Wonder if this is a case of Great business with average management still delivers better results than great management with average businesses.

Invested

Some important points from Q3 concall:

So in short, any further revenue and margin growth from here on will be largely driven by volume mix change or further price increase (assuming everything else remains the same). From share price action perspective, it looks more probable that any big move will happen only close to new capex coming online (more than 3 qtrs away + volume ramp-up time).

At monthly support and below long term Median PE, been a long term steady compounder so far.

Till Q3 , RM inflation was giving Margin headwinds & Freight issues were in favor of their competition. Hence price rise was Deferred, though taking minor hike in Q3. Baltic index has cooled off significantly and freight issues should go away.

Now EU stress with Russia Ukraine war weighing on it, given majority exports from EU. As of now risk aversion and any impact will be visible in Q4, has given decent corrections taking PE value below longterm median( 23 Now TTM basis - much lower if normalcy in margins returns per mgmt guidance, long term average has been 30)

Added positions with Med term perspective.

Brownfield expansion commissioned. Full ramp up in 2 Qtrs( Q2 23), additional 20% capacity.

Trend of revenue realization per MT from FY17 is unit is 21670, 22307, 24670, 23850, 25460, 28000+ - There is secular uptrend, though we can see FY22 being benefits from elevated realization, some moderation likely as CBFS/rubber prices cool down. 24K to 25K looks more sustainable.

Go forward capacities view

Valuations

While full capacity ramp up may be with some lag , for simplicity lets take 360000 MT at average realization at 24K to 25K gives - 8600 to 9000 cr revenue potential, mgmt has guided for 28-30% ( q3 deck and call) sustainable EBDITA, that gives a number of approx 2500 to 2700 cr range for EBDITA for FY24. As is the case , next Capex will be due in 2-3 years as well.

FY 19 and 20 EBDITA has been around 1300 cr and Price was in range of 1000 to 1300( excluding corona Mar 20 crash) - Note this was a bearish phase for small and mid cap - fast forward to year FY24 EBDITA should be in range of 2500-2700 cr - logically under normal scenario price should reflect corresponding upside in valuations as well to 2600-3000 by past median range( mkt being forward looking will happen earlier), about 50% upside from current levels. Note - back of envelope calcs and could be off.

Current risks - EU being key markets for exports for BKT, there is perception of disruptions as well as margin pressures in Q4 as well. Second order thinking tells that, Balkrishna competition which is based in EU will likely see much worse input cost pressures, given major Gas and crude dependency from Russia( Germany gets most of its Gas from Russia)- By not increasing prices BKT stand to gain mkt share at cost of margins

On Demand front need to see how it plays out given ongoing Russia, Ukraine issues and if any demand impact in EU, if any issues would reflect in Q4 - e.g. stocking/destocking , given BKT is heavy on Replacement, difficult to imagine any prolonged challenges unless Agri/industrial activity comes to halt in EU - contrary post war settlement could see higher usage of off road machines etc.

Invested and adding in dips

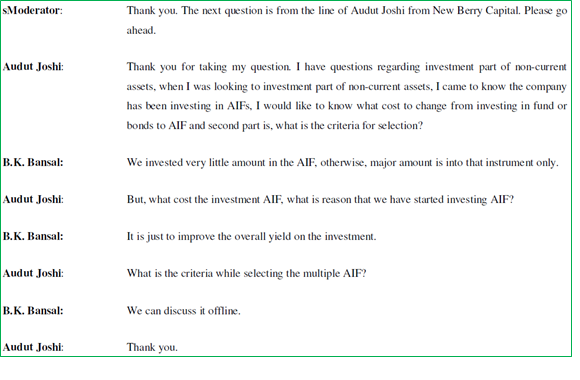

Yes! This q was also asked during a concall (dont recall which one) but had saved extract so sharing. And mgmt gave convenient answer and obvious solution to take it offline (a mgmt practice which I’m very skeptical of, tbh)

PS - Basant Bansal resigned as CFO in Aug '20 and he’s answering the qs here so this extract should likely be part of Q1FY21 concall.

Superb catch! He is 65 yrs now. Age may just be a number but now is he adding value commensurate to his Rs.37.42 cr comps in FY21? One can only hazard a guess but what majority institutional investors think is obvious I must say

Hi Dev,

While the recent quarters are outstanding, is it a case of a rising tide lifts all boats? Because of late; BKT certainly appears to be unable to grow faster than the industry. This appears to be a very fundamental issue but a very pertinent one.

BKT ~ consistently grew mkt share I would say till '18; from ~ 2% in FY11 to 5+% in FY18.

And it took them 3 yrs to modestly bump this up to ~ 5.5%+.

But in the latest concall (Q3FY22), Rajiv said mkt share is ~5% which was not a pleasant surprise!

Apart from the obvious answers of increase in competition, what exactly has stalled this mkt share gains since FY18 I’m unable to put a finger to it. If you or someone else has insights to be shared that be much appreciated.

Another vantage point: for the longest time they have been saying they want to achieve mkt share of 10%. FY11 they had said this. And in FY23; after a dozen years; they are still saying the same. We all know the +ves of the company - limited point is whether a premium valuation is justified for industry growth rate?