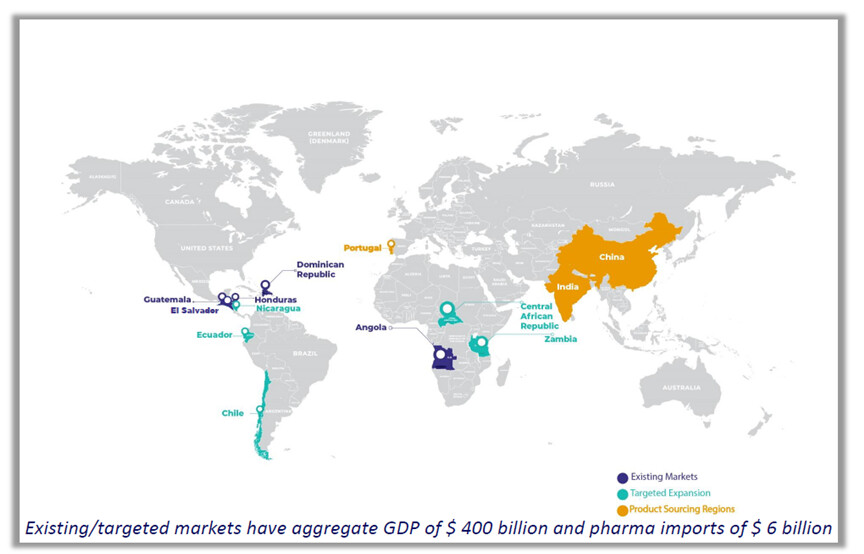

Balaxi Pharmaceuticals Limited is a branded IPR-based pharmaceuticals Company with on-ground presence in markets within Africa, Caribbean Islands & Latin America. It is presently an ‘asset-light’ IP-based pharmaceutical company with a different portfolio across multiple therapeutic segments, stock & sell models, and supplying branded and generic medicines. The pharmaceuticals formulation business is the fundamental driver of revenue, earnings, and growth.

Company is well-established in the existing markets of Angola, Guatemala, Honduras, and the Dominican Republic. It is entering newer geographies in Africa and Latin America, specifically El Salvador, Ecuador, Nicaragua, Zambia & Central African Republic. Beyond this, the company has plans to expand in additional Latin American countries for the next orbit of growth.

It has submitted several technical dossiers of pharmaceutical products for product registration in El Salvador, Honduras, Guatemala, and the Dominican Republic – hence building a deep pipeline of registered/approved products that will eventually become a formidable portfolio. With a growing brand penetration in Venezuela, among the top three markets by size in Latin America, the Company now aims to create in-roads in this region.

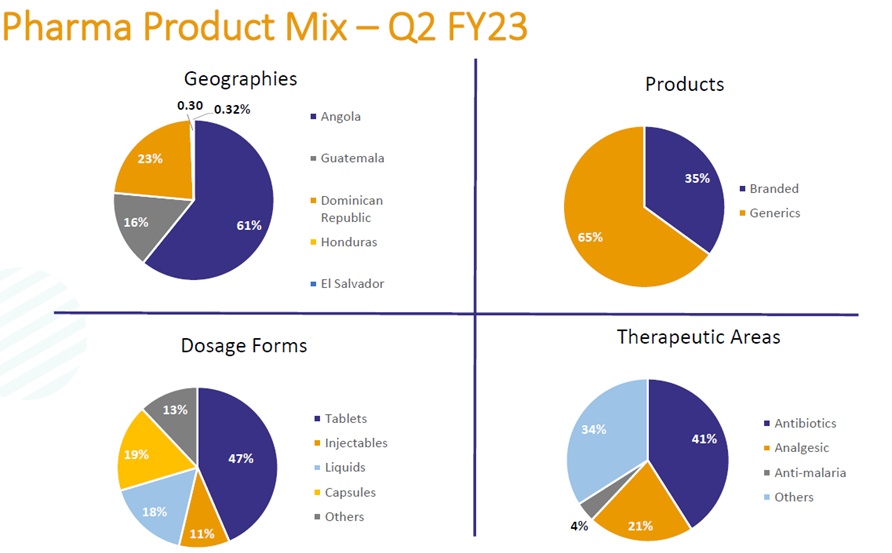

The current geographic and product mix is as follows:

It has a rich portfolio of 745 pharmaceutical product registrations (646 new registrations submitted), strong distribution strength of 37 warehouses, and a fleet of owned vehicles across four countries. The Company aims to double its portfolio of product registrations over the next two years. It has plans to set up a pharma warehouse in Nicaragua, Ecuador, Zambia & Central African Republic.

Future Expansions:

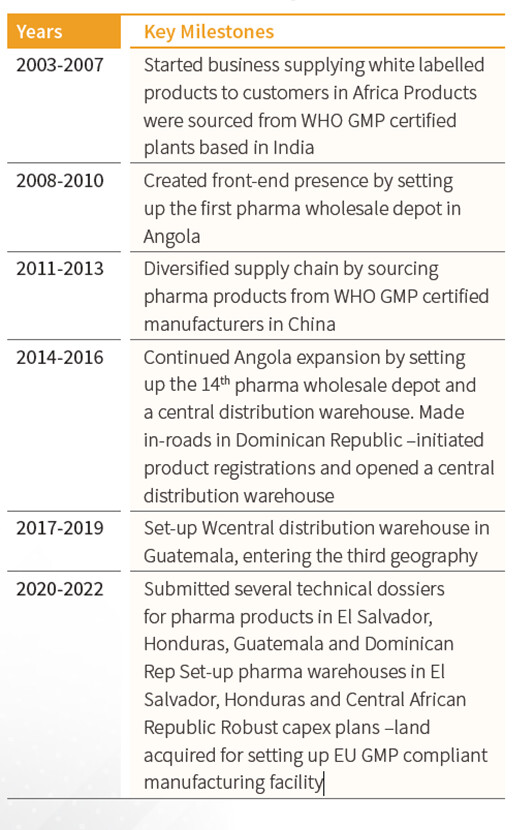

History:

Setting Up Manufacturing Facility

The Co has decided to invest in establishing in-house capabilities for researching, developing, and manufacturing differentiated formulations for Latin markets. It has acquired land to establish its first manufacturing location in the Pharma SEZ, Telangana and the ground breaking ceremony is scheduled on December 2022. It intends to establish a greenfield WHO-GMP/PICS certified manufacturing facility. This facility will be specifically focused on expanding the portfolio of differentiated branded formulations.

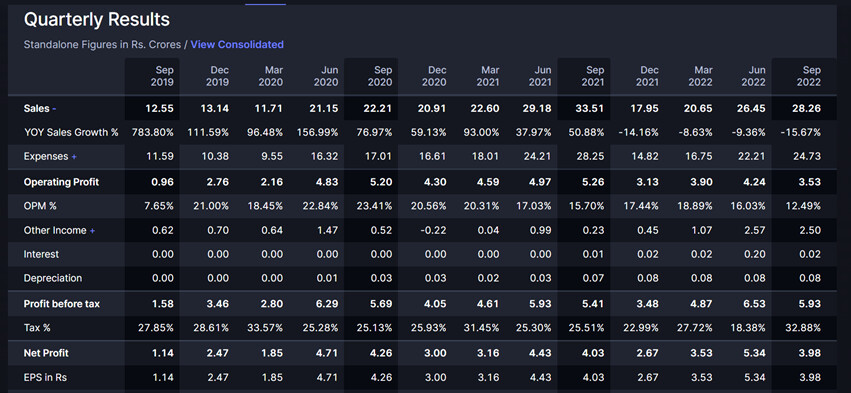

Financials:

Standalone results:

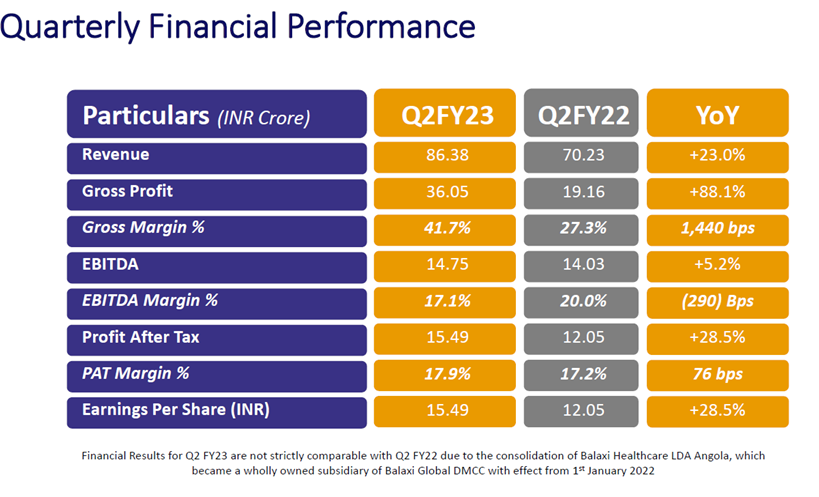

Consolidated results:

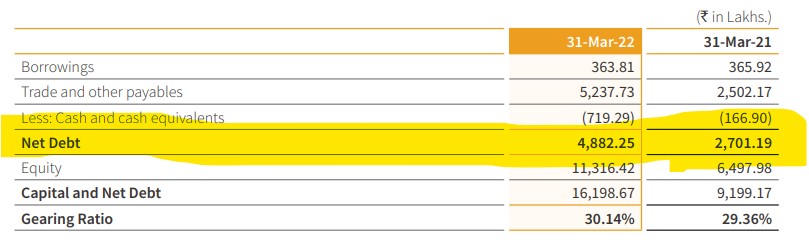

-The company was virtually debt free now but will take debt of around Rs 40 crs for manufacturing expansion.

- The ROE is 53%

- Please note that results post March 2022 will be different due to merger of subsidiary.

Quarterly Performance Commentary

Revenue

- Robust revenue growth of 23.0% YoY during Q2FY23 period was led by the Pharmaceuticals business. In this segment, Latin America contributed significantly with 29% growth. Previously launched geographies of Dominican Republic and Guatemala delivered strong expansion whereas Honduras and El Salvador have also initiated business operations and hold immense long-term business potential. In addition, other countries in the region are being lined up for upcoming expansion. In Africa, established operations in Angola resumed growth within the ecosystem of previously registered products, with the Central African Republic that is likely to start contributing from Q4 FY23.

EBITDA

- During this quarter, EBITDA was higher by 5.2% despite absorbing higher cost structures in several recently launched operations in countries that are likely to scale up to potential over the next few years. EBITDA declined marginally by 290 bps to 17.1% in Q2 –however, the outlook of margin expansion in most frontier markets targeted by Balaxi remains encouraging.

Profit After Tax and EPS

- Profit After Tax: Profit After Tax grew by 28.5% YoY in Q2FY23, despite lower margins. Earnings per Share (EPS) for the quarter was recorded at Rs. 15.49 compared to Rs. 12.05 in the corresponding quarter last year.

Risks:

Working capital intensive operations: Operations are working capital intensive as reflected in gross current assets (GCA) of 181 days as of March 2022 owing to inventory days of around 150 to 180 days. This is supported by moderate support from creditors of around 90 days.

Revenue concentration risks : More than 75% of revenue coming from Angola, the company remains vulnerable to economic uncertainties in the region and volatility in currency rates.

Risks related to the upcoming capex plans: The group is taking up a project to set up a New manufacturing unit in fiscal 2023 at an estimated cost of around Rs.95 crore, which will be partly funded via debt of Rs 40 crore. The balance requirement will be met through internal accruals and promoters’ contribution. Completion of the capex within budgeted costs, timely commencement of commercial operations and offtake from the same will remain key monitorables.

Management:

It is promoted by Mr. Ashish Maheshwari and family. Mr Ashish is CA by qualification and 1st generation entrepreneur. He started this business selling white labelled products to customers in Africa. Together with him, his wife and son are running the company and is typical family run business. There are professionals heading various business verticals whose detailed profiles are in AR.

Latin America Pharmaceutical Market

As per the Magma Information Centre research report, the Latin America Pharmaceutical Drug Delivery market was valued at $62.2 billion in CY2020 and is projected to reach $160.5 billion by CY2030, growing at a CAGR of 9.97% from CY2021 to CY2030. The oral drug delivery segment

was expected to be the highest contributor to this market, with $23.2 billion in CY2020, and is anticipated to reach $49.5 billion by CY2030, registering a CAGR of 7.86%. According to statistics, the generic drugs market in Latin America currently has a value of $37.1 billion. It is expected to reach a value of $50.6 billion, growing with a CAGR of 6.4% between 2021 and 2026. ACCORDING TO A PROJECTION FROM COHERENT MARKET INSIGHTS, the CMO (Contract Manufacturing Organisations) pharmaceutical market in Latin America will increase from $15 million in 2020 to more than $39.7 million by 2027. This represents a CAGR of 14.7% over these seven years. The Latin American over-the-counter drugs market is growing significantly: it’s set to post a robust CAGR of

8.64% between 2021 and 2026 and an increase in volume from US$11.4 billion to US$17.3 billion, as

per projections from Market Data Forecast.

The Central American region is a subset of the Latin American Market and comprises seven countries: Belize, Guatemala, El Salvador, Honduras, Nicaragua, Costa Rica, and Panama.

The estimated combined population size of the region is ~49 a million people, and its combined Gross Domestic Product (GDP) is estimated at ~$275 billion. The country with the highest GDP in the region is Guatemala – ~$78.5 billion, and the country with the lowest GDP is Belize – ~$1.8 billion.

Stock specific information:

Currently only ~8% of company is in hands of public. MGC Fund and Elara India opportunities fund are both holding 9.5% stake. Promoters having 73% holding.

The valuation is 11 times earnings with market cap of Rs 610 crs. I think its nearest competitor in terms of geography and product mix is Caplin Point. The PE of Caplin is 17.8

Disc: Invested and biased. Not registered analyst. Information for education and not for recommendation.