Balaji Telefilms - Indian Netflix in the making?

Hello everybody – See below my write up on Balaji Telefilms which I believe is at an inflexion point now.

Bit of history –

Run by ethical and able management, its traditional TV serials business has now turned around and is doing good. After severing the relationship and exclusivity with the Star channel in 2008, it took them a few years to stabilize this business and since 2013 the TV serials business is on an uptrend. (Accumulated cash - It was pre-2008 times that engagement with Star resulted in significant profits and cash in the books). They produce almost 1300 – 1400 hours of TV serial content every year. Of this almost 40% is hindi and remainder is in regional language.

Its movie business is not much to talk about and is still evolving and loss making. It is gorging on cash accumulated pre-2008. The movie quality is below par and only handful of movies have been successful such as Udta Punjab and a few others. You can see full list of movies here: Balaji Motion Pictures - Wikipedia

Management speak on latest quarter which clarifies that TV business is doing good. Moive business is a challenge: Hoping to have 10 shows on air by FY17 end: Balaji Telefilms

But Balaji seems to be in an inflexion point as it is launching its third business vertical –ALT Balaji (Over the top or OTT, new media platform).

ALT Balaji (OTT), A B2C play:

Launch timing - ALT Balaji launch anticipated in Jan 2017 after delay of almost 6 months.

Revenue stream – The business model that Balaji has chalked out for digital is subscription based ‘freemium’ approach as the primary source of revenue. Revenue from advertising, licensing and sponsorship will be the secondary source of revenue.

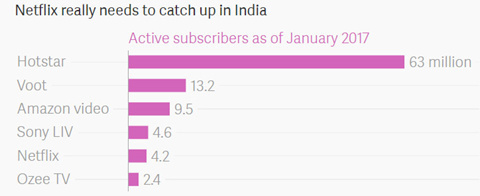

Competition landscape – Attached excel sheet Balaji v2.xlsx (1.1 MB)

provides details. Very few OTT players are providing original content. They are Netflix, EROS, VOOT, Hungama.

Market size – Initially Balaji is targeting 70 mn Indians who used net banking and have debit/credit card (no. to rise due to recent demonetization) + NRI/PIO abroad.

(FYI – India have 150 MN household with TV connection and 125 MN household with cable/satellite connection and 15 MN household with dish TV connection)

Investment – 150 cr raised from Atyant Capital and others in Mar 2016 and 65 cr is invested from internal accruals of Balaji. They have said that 150 cr more can probably be invested in FY 18/19.

ALT can be at an inflexion point for Balaji due to –

- OTT is a sun rise industry

- ALT will allow Balaji to focus on shorter format + different duration + genre

- Changing the company structure from B2B to B2C and turning into realty, the Balaji dream of owning a channel (IP owner)

- Only pure play listed OTT company

- Small market cap and TV/Movie business means OTT success can significantly boost market cap and revenue and EBITDA quality

- Low current market cap means OTT upside remains uncaptured by the market

The key question is will it be successful and value creative for shareholders? Below pros and cons, attempt to answer this question by balancing all viewpoints.

Pros of ALT –

- Balaji is the leader in content creation since 1990s so they can be relied on creating original series and content with strong appeal

- Balaji is targeting youth** + exclusive original series** (comedy, series, shows, drama etc. + Hindi, English, Tamil + regional) that can be viewed in multiple platforms anywhere anytime and no available anywhere else but in Balaji ALT entertainment app

- Annually produce and air c. 300 hours of content annually – enough original content to attract users. Plan is to launch 8 to 10 shows initially in Jan 2017 and then one new show every fortnight. Balaji will outsource good part of this 300 hours of content from external production houses, diversifying content type plus leveraging external expertise. With so much content, chances are quite high of some of the content becoming a hit and attract end users to subscribe

- First mover advantage in a sun rise industry where other players are focused on aggregating content/catch up TV with limited to no focus on creating exclusive original series (such as Game of Thrones, Breaking Bad, Better Call Saul or Netflix’s Narcos, Daredevil, Luke Cage, Stranger things etc.). First mover advantage is key here as by the time other players start focusing on creating originals, Balaji would have already created a library which should act as a strong competitive advantage to attract end users - Strong technology interface. Balaji Telefilms Selects Xstream and Diagnal to Power its Global OTT Entertainment service, ALT Balaji (the same is used by Netflix)

- OTT is a proven model which has worked in the west and so should work in India. We love western stuff (iphone, western branded apparels …). This is why AMAZON is also investing 2000 cr cumulatively to produce original series for Indian viewers

Cons of ALT –

-

Rising competition + Incumbency of YouTube in the market

o Amazon has ear market 2,000 cr for creating original and local content, unlike Netflix. Amazon is a big and real competitor for Balaji but its pricing will be close to what Netflix charges right now i.e. c. 500/month or 6000/yr. So Balaji can be competitive on the pricing front to manage international competition.

o Mitigant – Rising competetion signifies the strength of this disruptive trend. Balaji is not a competition (to most of the OTT) but complimenting. Balaji’s ALT is positioned between English movie n soap (available on Netflix) and mass India entertainment (available on TV and every other OTT platform of the competitor) - ALT is not a one stop solution as ALT does not have movies, catch up TV, channels, etc.

o Mitigant. But since they will air original exclusive series which are not available anywhere else, it should be able to draw end user -

Inadequate bandwidth speeds

o Mitigants - The 4G rollout will boost infra speed - Indians (like Chinese and unlike westerners) don’t want to pay

o Mitigant – Balaji only needs 2 mn subscribers by 2020 to be able to create shareholder value from current low market cap base. Also even in China which is same as India there are users who have started paying for the content and now it is a billion dollar industry. Also the link shows research which says that 21% of Chinese are ready to pay for OTT OTT in China: Viewership grows more quickly than expected | Media | Campaign Asia -

Piracy is a concern

o Mitigant – Hopefully there will be enough users who would like to pay a nominal amount for good technology driven hassle free differentiated content experience which pirated content does not provide - Govt. regulation against OTT – unknown at this stage!

Despite strong pros, cons are not weak. But given disruption capability of the OTT platform + promoter’s leadership position + large addressable market size + extremely cheap market capitalization: it looks like a very good opportunity.

Valuation -

Based on future OTT value – Attached excel sheet Balaji v2.xlsx (1.1 MB)

provides details. Assuming 2 mn OTT subscribers by 2020 each paying 2000/yr – The current valuation assuming 3x EV/Rev in 2020 and 10% dist rate is 820 cr rupees. As opposed to current market cap of 706 cr rupees.

The above Huawei sponsored research estimates that India OTT market will have revenue of 1.1 Bn USD by 2021. If we estimate Balaji will have 2 mn subscribers paying 2000 each/yr - it is 400 cr or c. 5% of 1.1 Bn. A 5% market share for Balaji, the OTT showing original series is definitely very conservative!

Assume we give 400 cr valuation to the existing business of TV serial and movie business, the total value is close to 1106 cr based on a very conservative valuations. (FYI - Existing business traded between 200 - 500 cr valuation between 2012 and 2015 June, before the OTT announcement.)

The business has 200 odd cr cash in books which I assume that will be lost in their loss making movie business and we should not attribute any value to it.

Based on star’s stake sale - Star India sells 26% stake in Balaji Telefilms for `108 crore in Aaug 2015 which means total value of 415 cr. Add to this the 150 of fund raising by equity dilution in Mar 2016 – the current value comes to 565 cr (20% below CMP or roughly 75 bucks. This is the price the share was quoting few days back). The Star stake was acquired by Radhakishan Damani, Bhanshalis and the promoter itself.

Based on recent fund raising - Atyant Capital/Rahul Sarogi bought shares in the company at 140 rupees/share in Mar 2016 when the company was raising 150 cr and Atyant also bought shares at c. 85/share in sept this year. (FYI - Atyant Capital/Rahul Sarogi is holding on to a big stake in Navin Fluorine since 2011 or 2012 i.e. he foresaw/spotted CRAMs trend very early on)

Lastly, promoter hiked stake in the Sept quarter (min price during that quarter was close to 85 bucks).

Key positives for the stock in the future: Good end user review of ALT original series; Rising subscriber numbers and ALT revenue; Exiting film making or turnaround of the same; ALT expanding its OTT platform to include movies and other non-exclusive TV channel content borrowed from other sources incl. such as broadcasters and say Shemaroo’s movie library.

For further reading please look at the attached sheet.

Lastly an interesting article from Swanand Kelkar - Executive Director at Morgan Stanley Asset Management

Do read with an open mind and let’s have a healthy discussion focused around pertinent issues and risks and anything else you may deem fit. At your disposal for a healthy debate. I know that there is already a balaji thread but given the nature of the transition, I thought it warrants a separate thread and discussion. thanks

Invested and biased. Please do your due diligence before investing as my data / analysis / logic / conclusion can be wrong.