Balaji green tech happened to be their unlisted Pvt Ltd. Company.est.in 2005…If we go by AR 2017…IT registered more than 50% fall in revenue and net profit…With negative growth of assets by 8%.why balaji amines should merge this loss making idea??

Greentech appears to be a business failure and in hindsight bad decision to enter the business in the first place. While they could have just let it default on the bankers am guessing there would have been some comfort or gaurantee given. Not too worried about the same fate for BSCL because as of today the business seems to be sound. Of course things could change. The risk that one is taking essentially is that the other 45% gets bought at a high valuation. That’s for each investor to decide if it’s okay or not.

Curious to know your take on the forest NOC issue. Capex has been lying idle for a long time. Now certain reports suggesting even balaji specialty chemical capex is awaiting the same clearance.

As posted above in the interview dated Jan 28th with CNBC, mgmt stated that BSCL got commissioned in Jan-end against the estimated Oct 2018 timeline.

He also said turnover contribution from the plant will start only from Feb 2019.

With regards to the forest NOC issue, I believe they were mainly awaiting clearance for acetonitrile while Morphilne and DMA Hcl were already started. Don’t know if there is any change in the status of that.

Main issue is that any company in the chemical space should first get the clearances before doing capex. Here company is waiting for clearances after doing capex. I dont understand the rationale for that. Also they have been awaiting the Forest NOC for acetonitrile for more than a year.

1 Like

Below is my understanding of the situation:

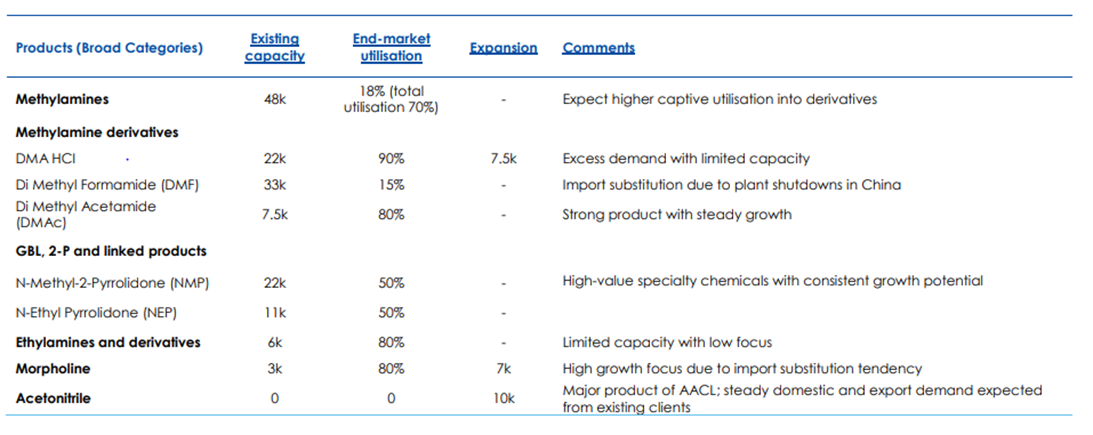

If you see above snapshot from Edelweiss IC report, you will notice that DMA HCL and Morpholine were already being manufactured in Unit - 3 and hence did not require an explicit clearance unlike Acetonitrile.

BSCL too is part of Unit 3 which is why there is a hold up for both Acetonitrile and the upcoming products such as EDA and Piperazine.

Even the new Unit - 4 (mega project) land has been allotted by the state government. Are the promoters wholly to blame for this situation or is it a case of typical Indian bureaucracy where one hand does not know what the other is doing.

One has to just wait and watch.

Thanks for the response. I’ve been trying to understand this for some time.

Commentaries on performance FY2018 from Jiutian Chemical

https://links.sgx.com/FileOpen/Fy2018%20result.ashx?App=Announcement&FileID=545033

-

Revenue in FY2018 increased by 16% from RMB 1,124.44 million in FY2017 to RMB 1,308.27 million, mainly due to increases in both sales volume and selling price of DMF and Methylamine (collectively, the “Products”).

-

Sales volumes of DMF and Methylamine in FY2018 were 9% and 5% higher than that of FY2017 respectively.

-

For FY2018, average selling prices per tonne of DMF and Methylamine were RMB 5,558 and RMB 8,530 respectively, which were 13% and 1% higher than that of FY2017.

-

The increase in average selling prices was mainly due to a tighter industry supply arising from production stoppages and cuts by other producers for environmental reasons.

-

Between FY2017 to FY2018, capacity utilisation at the Anyang Jiutian Fine Chemical Co., Ltd’s * (a 100% owned subsidiary of the Company) (“Anyang Jiutian”) Dimethylformamide (“DMF”) plant increased from 65% to 70%, whilst capacity utilisation at the Anyang Jiutian Methylamine plant remained at 100%

-

Anyang Jiulong generated revenue from the production and sales of Dimethylacetamide (“DMAC”) to third parties.

3 Likes

Looks like they’ve received forest NOC for the acetonitrile facility finally after a long wait. This may be a big trigger.

Read from page 28 onwards - http://www.moef.nic.in/sites/default/files/Minutes%20of%2053rd%20Meeting%20of%20the%20Standing%20Committee%20of%20National%20Board%20for%20Wild%20Life%20held%20on%2025%20February%202019%20(1)_0.pdf

2 Likes

The meeting was held in February. The minutes are dated 25th March. The news was known to serious players…it seems. Hence no impact seen.

Disc. Invested.

1 Like

I could not find official announcement or disclosure by company getting wildlife noc for its various expansion projects. Recently company conducted investor conference…but no presentation / transcript posted by the company.

Would be helpful if anyone has information on the expansion projects clearance.

Thanks.

Disc. Invested.

1 Like

http://www.balajiamines.com/pdf/1555409966BALAJI%20INVESTOR%20PPT.pdf

They have uploaded the presentation on their website, please visit.

2 Likes

In the presentation, there is a clear mention (on page 15) as - new plant for manufacture of Morpholine and Acetonitrile is commissioned after successful trial runs and_ready to be operational

If I am not wrong, this was the plant that was waiting for the crucial wildlife clearance.

1 Like

The much awaited wildlife approval has not provided any boost as far as stock price is concerned. Infact it has given up all the gains from 500+ to 430 now.

On the other hand Alkyl amines is consolidating nicely.

Are there any issues with the company?

@crazymama you have any insights into recent developments in the company?

Thanks

Disc. Invested

1 Like

Had seen an interview on BTVi dated 29.03.2019, where the management said “the wildlife clearance shall be obtained in coming one or two weeks”,

so, I guess, the issue of that wildlife clearance is still hanging!

Further, their proposal for mega project (at cost of Rs. 750.00Cr) is under process for environment clearance and entire proposal can be found at environmentclearance.nic.in.

Although exact reasons of the under-performance of the stock can’t be ascertained, it may have been hammered due to lack of clarity.

3 Likes

Further, I expect the price to remain subdued in the short run since the present growth triggers may start fully contributing in next 1 to 1.5 yrs only (hopefully!) -

- the operations of the subsidiary BSCPL is expected (might have already started also) to contribute by Q2

- If wildlife NOC is obtained, results from the Morpholine and Acetonitrile expanded capacity may be seen only in Q2.

- The mega project may contribute by Q2- next FY only.

Hence, full potential of the present growth triggers may give fruitful results by March 2021 only.

However, in the chemicals sector, things move too fast and hence there is the risk of those triggers getting offset by changing environment during the period also.

disc. Invested.

2 Likes

No special insights. Have not got the opportunity to engage with the management so far.

Based on the link shared by @paransaikia, the company seems to have cleared their LT debt. Mention of Betaine HCl is something new since it was not part of EC submission.

Updates from Jiutian Q1 CY19 results:

Jiutian’s Chairman, Han Lianguo, said, “We are disappointed to report a net loss in

1Q2019, with our main products of DMF and methylamine starting to face margin

squeeze arising from weaker demand for chemical products in general.

http://infopub.sgx.com/FileOpen/1Q19%20Press%20release.ashx?App=Announcement&FileID=555906

Revenues for 1Q2019 was RMB 300.64 million, a 8% decrease from 1Q2018 of RMB 325.98

million, mainly due to decreases in selling price of DMF and Methylamine partially offset by the increase in sale volume of DMF. For 1Q2019, average selling prices of DMF and Methylamine was RMB 4,464 per tonne and RMB 7,592 per tonne respectively, which were 27% and 17% lower than that for 1Q2018. The decrease in average selling prices of the products were mainly due to challenging market condition. Sales volume of DMF and Methylamine in 1Q2019 were 40% higher and 4% lower than that of 1Q2018 respectively.

Between 1Q2018 to 1Q2019, capacity utilisation of Anyang Jiutian Fine Chemical Co., Ltd’s (a

100% owned subsidiary of the Company) (“Anyang Jiutian”) DMF plant increased from 73% in

1Q2018 to 81% in 1Q2019, whilst capacity utilisation of the Anyang Jiutian methylamine plant

remained at 100%.

http://infopub.sgx.com/FileOpen/1Q2019%20result%20ann.ashx?App=Announcement&FileID=555905

Results appears flat, but the interesting part is the new capacity is operating from 20.05.2019 (including the much awaited morpholine, aceto-nitrile one).

This will be interesting to see the impact of the capacity addition during Q2 onwards.

1 Like

No word on the ethylene diamine capacity. I think environmental clearance would be granted together.

Inventories are up from 90crs to 160crs. Without much increase in sales. Not good. However, this could be because of volatility in methanol and supply issues from Iran. Also in expectation of new capacities coming on stream. Receivables are down YoY which is good.