Balaji Amines Limited Q4 FY20 Earnings Conference Call

1 Like

Hello @crazymama Are you still tracking this company?

After going through the VP thread, your presentation and 3 conference calls I figured out a couple of things and need your opnion

- Current margins are elevated and we should rather make our assumptions on 18% EBIDTA assumptions.

- Company is not able to scale up Acetonitrile because they have been saying that they will do 15-20 Tons per day however they are still at 9 tons.

- DMF can be a big opportunity with ADD and this current China situation might favour. I am not able to understand that despite DMF prices to be around 75/Kg in Q3 and Q4 FY20, why they are still not able to scale up the capacity utilisation.

- Unable to figure out rationale for delaying Ethyl Amine and DMA HCL capex because it takes time for company to stabilize the production.

- Proposed 5-7K tons growth for FY21 will come mainly from DMF, Acetonitrile and Morpholine.

Please give your inputs.

Kanv

Disc. - Took a trading position yesterday and the DMF story looked convincing but still unsure.

2 Likes

Balaji Amines AR 2020 Notes

Company’s annual report was very detailed and the MDA report gives good insights into the Aliphatic amines Industry. Management’s tone in the AR is very optimistic for the next 3-5 years and focus is on new greenfield project and a lot of first time import substitute products in India. Management does indicate short term headwinds for the next 2 quarters.

- Chairman’s Speech

- In our endeavour to pursue future organic growth opportunities, FY20 has been a very rewarding year as your company received the environmental clearance for 90-acre Unit IV Greenfield project and also your company’s subsidiary Balaji Specialty Chemicals Private Limited received consent to commence operations from Maharashtra Pollution Control Board (MPCB).

- We have already spent more than Rs. 70 crores in the Greenfield project as on 31st March, 2020.

- Over the years we have developed expertise to set up chemical plants in a short period of time. A decade ago, it used to take us two years to set up a chemical plant with a capacity of 50 Metric Tons/day. Today, we can do the same in six months. The new plant we set up in Balaji Specialty Chemicals was commissioned in a record 12 months.

- We have plans for a capital expenditure of Rs. 70.00 Crs. in the next financial year.

- Your company’s strategy has been to gradually launch new products which are cost-effective and technology based with import substitutes that can enable us to capture market share in India. In line with the same we are planning to introduce Dimethyl Carbonate which is a complete import substitute into our product portfolio in the next financial year.

- Exports: Rs. 181.95 cr in FY20 compared to Rs. 209.50 cr in FY19.

Imports: Rs. 134.70 cr in FY20 compared to Rs. 270.36 cr in FY19. - In about 60% of our products, we are the only manufacturer in India for products like NMP, NEP, GBL, 2P, Morpholine, DEAE, DMAE, DMU, DMF, PVPK-30.

- Our selection policy for end product is to either be the first or second manufacturer in India - to substitute products that are being imported into the country.

- Key customers include Sun Pharmaceuticals, Dr. Reddy’s, Aurobindo Pharma, Jubilant Lifesciences, Teva API, Hetero Drugs, Kores India Limited, Venky’s (VH Group), Wanbury, ZydusCadila, Indian Oil, Hindustan Petroleum.

- Revenue from pharmaceutical sector constitutes about 55% of your company’s revenue, followed by agrochemical sector at 20%. Other segments like dyes, textile, animal feed, water treatment chemicals and refinery contributed about 5% each.

- Total Capex spend during FY20 is Rs. 70 crore. The capex has been towards construction of Unit IV plants (Greenfield project) as well as construction of Morpholine and Acetonitrile plants.

- Benefit due to lower crude prices have not percolated down to us, as the prices of our key raw materials like methanol have not witnessed much decline due to the fallout of USA sanctions on Iran, which is one of the dominant manufacturers of methanol in the world. At the same time, your company has no dependence on China for its raw material requirements.

- The company has extended corporate guarantee to institutional lenders to an extent of Rs. 225.00 Crores to secure the borrowings of its subsidiary. The said borrowings of the subsidiary are also secured by personal guarantees of the Directors Sri A. Prathap Reddy, Sri N Rajeshwar Reddy, Sri D Ram Reddy. Sri G Hemanth Reddy and Sri. A Srinivas Reddy

- Balaji Speciality Chemicals Pvt Ltd.: FY20 Sales Rs. 53.89 cr., PBT Rs. -21.88 cr and PAT Rs. -15.55 cr. Company owns 55% of the subsidiary. Total investment in the subsidiary Rs. 112.34 cr which constitutes Rs. 66 cr as equity investment and Rs. 46.34 cr as loans given.

- Received consent to operate by Maharashtra Pollution Control Broad (MPCB) in June 2019. Post the consent from MPCB, the subsidiary has commenced production of niche products like Ethylenediamine (EDA), Piperazine (PIP) and Diethylenetriamine (DETA).

- The subsidiary’s plant has capacity of 37,350 TPA (Metric Tons per Annum) for EDA; 4,050 TPA of PIP and 3,150 TPA for DETA. Thus, your company is the only manufacturer of EDA, PIP and DETA in India

- India is currently importing about 29,000 tons of EDA; 8,000 tons of PIP and 3,000 tons of DETA. EDA basically goes in to end user industry of agrochemicals for manufacturing mancozeb. PIP and DETA is consumed for applications in pharmaceuticals, polymer, coatings, etc. All three products have good demand.

- The volume off take from the subsidiary plant has gradually increased and witnessed the best performance in Q4FY20, despite the initiation of lockdown in later half of March 2020

- Your company has signed contracts from leading agrochemical companies in India for their product requirements for Q1FY21 and subsequently envisage to sign long-term contracts with them.

- Subsidiary is expected to witness a volume offtake of about 15,000 tons in FY21.

- Greenfield Project - Phase 1 (Unit IV)

- In November 2019, your company received the environmental clearance for 90-acre Unit IV at MIDC, Chincholi Greeneld project and the construction of the plant has begun since then.

- In Phase I, your company has planned to install 15000 tons per annum of Ethylamines and 9,900 tons per annum of other products.

- Phase I of Greeneld project involves capex of Rs. 150-170 crore (which is funded from internal accruals) out of which Rs. 70 crore capex (including Rs. 20 crore for 90-acre land) has already undertaken in FY20.(The peak asset turnover achievable is 2x).

- Post the commencement of plant at the Greenfield Project, your company will have the largest installed capacity of Ethyl Amines in India at 22,500 tonnes per annum. The new plant of Ethylamines at Unit IV will lead to lower cost of production due to new technology. Demand for Ethylamines is growing at 10-15% p.a. in India

- Acetonitrile

- Your company commenced manufacturing Acetonitrile from November 2019 onwards. We have installed capacity of 9,000 tons p.a

- We commenced production by manufacturing about 8 tons per day, gradually improving to about 12 tons per day in March 2020, which we steadily plan to increase to about 25 tons per day in coming year.

- As the higher price Acetonitrile may not be sustainable on long-term basis, your company has also developed another fungible product Tetrahydrofuran (THF), which can be manufactured on the same plant of Acetonitrile. If there is any volatility in price of Acetonitrile going ahead, your company plans to switch between manufacture of both Acetonitrile and THF.

- Currently, no company in India manufactures THF and its demand of 15,000 tonnes per annum is currently met fully by imports.

- Morpholine and Di-Methyl Formamide (DMF)

- Your company’s production capacity for Di-Methyl Formamide (DMF) is 30,000 tons per annum whereas the total demand in India is for 45,000 tons p.a. However, your company has historically been able to achieve capacity utilization of only about 30% due to dumping by China and other Manufacturers.

- We have made an application to the Government of India for levying antidumping duties on DMF.

- Nevertheless, in recent months we have witnessed better pricing of DMF, which has made the manufacturing of DMF viable. If the price realization remains steady, we anticipate gradual improvement in capacity utilization to 60% from around 30% in FY20, which was about 20% in FY19.

- Hotel Business

- IN FY20, the occupancy rate of the Hotel was 58%.

- In FY20, Average Room Rate (ARR) and Revenue per Available Room (RevPAR) was Rs.3,452/- and Rs.1,994/- respectively.

- Hotel division did sales of Rs.20.40 crore in FY20 with Cash Prot of Rs. 4.51 crore.

- As mandated by the Government, the hotel has been shut down and is non-operational from the lockdown period considering the safety of employees, customers and tourists. We have initiated cost reduction measure programs to reduce the xed cost of the hotel.

- Covid19 impact

- Your company, being engaged in essential goods, has been operating at around capacity utilization of 70%, even during lockdown.

- Since the majority of our products are used in pharmaceuticals we decided to produce and supply as much as we can in this difficult time to indirectly serve the county and to the world for medicines. However, the capacity utilization was affected owing to varied factors like nonavailability of labour, disrupted supplies of packing material, delays in port clearances, limited availability of trucks and tankers for movement of raw material and finished goods.

- As lockdown eased, your company ramped up capacity utilization levels and has sustained to original levels.

- Overall, the demand contraction from the domestic market and fall in exports for products consumed in other end-user applications like dyes, paints, coatings, textiles, polymers and refineries are likely to persist for at least first two quarters of FY21.

- Aliphatic amines Industry

- Aliphatic amines are hazardous in nature when not handled with proper safety during transportation and hence the hazardous nature reduces the threat of imports. Specialised vehicles are required for movement of these chemicals which restricts the distances over which they can be transported. As a result, consumers prefer to source locally.

- Globally, the amines industry is well structured with a small number of participants, typically not more than 3-4 players per region and relatively balanced in terms of demand and supply.

- The industry is driven by regional supply and demand dynamics, due in part to the high cost and logistical challenges of transporting amines. As a result, roughly 80% of amines production in India is sold and consumed within the country. Only 5% of the Indian demand for methylamines is catered by imports.

- Secondly, freight is a big element of cost, which makes imports uncompetitive.

- Indian aliphatic amines market is substantially consolidated with two companies (including your company) accounting for 95% of total market share.

- Given the growing thrust of demand from pharmaceuticals and agrochemicals industry, Indian amines market is likely to record double-digit growth over next 3 to 5 years. The growth in margin-accretive amine derivatives is likely to surpass the growth in basic amines.

- Of the three raw materials, while prices of ethyl alcohol are relatively more stable, both ammonia and methanol have historically been volatile. However, raw-material cost pass-through to end customers is standard practice in the industry.

Regards

Harshit Goel

28 Likes

significant upswing in bottomline can be expected if imports of DMF from China is restricted.

disclosure: holding

Hi Folks,

I guess that some of you had a look at the AR. So I went through yesterday and was working on refining my valuation model. I thought its good to discuss some of the key pops and risks that I have noted down for you.

| Key strengths | ||||

|---|---|---|---|---|

| New growth avenues | Max new capacity | price | Max rev. impact(cr) | |

| Ethylamines | 15,000 tonnes | New capacity | 80/kg | 120 |

| DMC | 9900 tonnes | New capacity; Import Substituion | 70/kg | 69.3 |

| Growth in Amine derivatives | margin increase in derivatives over basic amines | |||

| BSCPL | 15,000 tonnes | growth in EDA, PIP, DETA | 100/kg | 150 |

| Acetonitrile + THF | 25 tonnes/day | started in Nov 2019 @ 8 tons/day and increased to 12 tons/day in March 2020 | 350/kg | 288.8 |

| DMF | 9,000 tonnes | increase in capacity utilization from 30% to 60% on 30k tonnage plant; Additional increase on Chinese ban | 70/kg | 63 |

| Overall amine growth | 9% | Cagr 9% | 82.8 |

Total Upside = 774 crore (>80% of current topline)

Key risks

- hotel business - Covid19 impact on 20 crore turnover

- Lower capacity utilization - Already at 70% and with more lockdown and logistical issues this will bring the revenue down

- Business segment(Dyes, Polymers) - Lower demand on business segments that contribute 25% to topline

- Raw material price increase - Methanol, and ammonia.

Cheers!

Uzi

6 Likes

Good Presentation on AR 20.

What is forcing promoters to lie so much?

When DACL only makes these for past decade or more already:

4 Likes

Q1 FY 21 results are out. Looks like Balaji Speciality( subsidiary) is not getting traction.

In the Press release company has mentioned that subsidiary plant was shut for April and May. Current monthly turnover in subsidiary is 10-12 cr . This can be verified in Q2 results.

Disc.invested

ADD on DMF recommended by DGTR. I understand that Balaji amines is the only producer of DMF in india and capacity utilisation was about 30% due to dumping. ADD of 23/kg to 35/kg recommended awaiting final notification from finance ministry.

http://www.pharmabiz.com/NewsDetails.aspx?aid=130565&sid=1

Will this help Balaji is increasing the capacity utilisation of DMF at decent margins?

Disc. Invested in Balaji amines

1 Like

If the history is to be believed, every upmove has the same story. I will remain cautious. Current price has more risk than the steam.

1 Like

This is going to benefit Balaji Amines these product choline-chloride is made by them. https://www.moneycontrol.com/news/business/dgtr-recommends-anti-dumping-duty-on-choline-chloride-imports-from-china-malaysia-vietnam-5757461.html

1 Like

Balaji Amines is in a sweet spot . The Environment is also favourable as Growth In Pharma and Agro Chem sector is driving growth in Amine Sector. In Q1 FY 21 Concal , management also Said ““We are very focused on next level of growth and upscale for Balaji Amines over the next three to four years .””

4 Likes

Q1 FY21 Earnings call transcript:

2 Likes

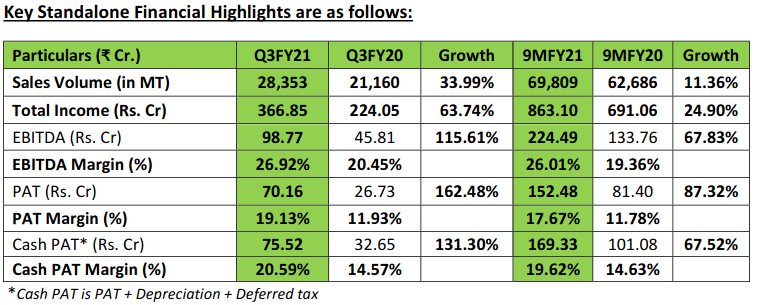

Good Q2 results postes by Balaji. Snippet from broker note…

Balaji Amines Q2FY21 Results (First Cut): Gross margins improvement leads to best in class EBITDAM reported; highest sales recorded (unrated)

Result Highlights

Balaji Amines consolidated Q2 revenue came in at Rs2.8bn up 24% yoy, driven by better performance in Amines division.

EBITDA was at Rs737mn up 65% yoy. EBITDAM expanded 640bps to 26.1%, on lower RM costs and better product mix. Gross margin grew ~600bps yoy to 45.8%

PAT (after MI) grew 60% yoy to Rs458mn on higher operating income base, lower interest costs (down 25% yoy to 54mn) partially offset by higher ETR (26% vs 8% last year).

Amines division sales up 34% yoy to Rs3.12bn, EBITM up by 700bps yoy to 23.3%, EBIT at Rs728mn up 88% yoy

Hotels division sales down 86% yoy to Rs8mn, reporting a loss of Rs15mn at EBIT level

Board has approved to set up separate plant of methyl amines of 40-50kmt for which EC is already received. Also a separate plant for DMF for 30kmt is approved.

Concall scheduled on 2nd Nov’20 at 4pm. (+91 22 6280 1325/+91 22 7115 8226).

Regards

5 Likes

Business:

-

Recorded 21% YOY growth in total revenue from Rs.233 crores in Q2FY20 to Rs.283 crores in Q2FY21.

-

Capacity utilization this quarter was similar to pre-covid levels.

-

Products like acetonitrile, DMF, MGP, DMA & EEA will continue to remain elevated in terms of demand as they are intermediate for drugs required for covid-19 treatment.

-

Total values recorded a growth of 8% at 23,150 MT as compared to 21,376 MT in Q2FY20.

-

The values of basic amines for Q2FY21 stood at 5,094 MT, derivative values at 9,916 MT & speciality chemicals at 8,140 MT.

-

EBITDA: Rs. 72 crores in Q2FY21, up by 49% as compared to Rs.49 crores in Q2FY20.

-

EBITDA margin expanded by 467 bps in the current quarter i.e from 20.8% to 25.5%.

-

The improvement in EBITDA margin was due to the improvement in operating leverage, increase in value uptake, price variation & benign raw material prices.

-

PAT grew by 37% at Rs.48 crores in Q2FY21 as compared to Rs. 35 crores in Q2FY20.

-

PAT margin stood at 16.8% as compared to 14.9% in Q2FY20.

-

H1FY21 Performance: Revenue from operations- Rs.496 crores, up by 66% as compared to Rs. 467 crores in H1FY20. EBITDA witnessed a growth of 43% i.e Rs.88 crores in H1FY20 to Rs.126 crores in H1FY21. PAT grew by 51% from Rs.55 crores in H1FY20 to Rs.82 crores in H1FY21.

-

The subsidiary i.e Balaji Speciality Chemicals which largely caters to the end-user industry of agrochemicals had an improved sales run rate of Rs.10 crores per month in Q2FY21.

-

The prices of finished products as well as raw materials of the subsidiary company have fallen.

-

The subsidiary company received reach certification from Europe.

-

In FY20, received reach certification for thee export of other products ethylenediamine.

-

India currently imports 29,000 MT of EDAs & 7000 MT of PIP.

-

Currently manufacturing 9 tons per day of acetonitrile.

-

De-bottlenecking exercise which has recently commenced & will gradually ramp up the production of acetonitrile to 18-20 MT per day.

-

Pharmaceutical companies increasingly preferring to buy acetonitrile which is manufactured by a direct route.

-

Balaji Amines is the market leader in methylamines production in India. Methylamines is a key raw material & the base product for manufacturing value-added derivatives required by pharmaceutical & agrochemical companies.

Management:

-

Witnessed increase in demand across the product portfolio with improved realisation.

-

Expect better value markets in the second half of the fiscal year especially with the expected

revival of the entire economic value chain across industries. -

Operating performance is strong despite the losses due to inventory markdown from the legacy

-

CFL business & the losses may continue for some more time as we continue to liquidate

inventory. -

Looking at the revaluation of the land and building of CFL business to offset this.

-

Expect demand for acetonitrile to remain elevated as it has emerged as preferred solvent by

-

various end-user companies as compared to other solvents

-

Striving to further improve acetonitrile through R&D.

-

Completed capex of 105 crores in the 90-acre greenfield project out of the total capex of 150

crores. -

Expect to commission the production of ethyl amines by the end of this financial year.

-

The shortfall of supply in ethyl amines in India is likely to increase to 15,000 ton per annum by

FY23 from 9000 MTPA currently -

Demand for ethylamines is likely to improve as it will find its application in covid-19 medicines

also. -

The production of dimethyl carbonate is expected to commence during FY 2022. Dimethyl prices

have improved due to higher import prices from China as well as Saudi Arabia and also a

case for anti-dumping is pending with the govt. of India -

Setting up separate plans for methylamines aligned with a capacity of 40,000 to 50,000 MTPA &

DMF with a capacity of 50,000 MTPA at unit 4 which will be a greenfield project. The company has

already received approvals for environmental clearance for methylamines. -

First time in history seeing export enquiries for DMF

-

DMF capacity should increase to more than 1,500MT per month.

Risks:

-

Raw material volatility

-

Hike in Acetonitrile prices

-

Poor capital allocation in CFL & hotel business.

8 Likes

Expanded capacities will start coming online this quarter onwards. Big question mark is about the sustainability of margins. On other parameters, Balaji Amines with its bouquet of products is streets ahead of competitors like Alkyl Amines which is dependent on just

Acetonitrile riding high zooming global prices for a while now.

disclosure: holding Balaji Amines and hence biased.

6 Likes

I was wondering if anyone here had any insights on Acetonitrile, it has been a big contributor to revenues and margins for both Amines companies in India, Alkyl and Balaji. Both are also expanding capacities. This clearly has been a BIG tailwind for the stock. Neither company, however, provide much colour on revenues/margins related to Acetonitrile.

Anyone with any insights on demand/supply dynamics and pricing going forward?

1 Like

Notes from the Q3 call:

Increase in Margin in Q3 – due to Better product mix and raw material availability

- 22 to 23% EBITDA margin sustainable going forward

Acetonitrile capacity ramp up by end of fy 21 post debottlenecking.

- Capacity will increase to 18 to 20 tonne per day from 8 to 9 tonne per day

- R &D efforts are on to further produce Acetonitrile at more competitive cost

Gathered from earlier calls,

- Prices were around Rs 250 to 270 - 6 months back and continue to remain at Rs 280 now

- Management has denied any change in supply side scenario in the last call. (no noteworthy capacity addition globally)

- With doubling of capacity – augurs well for FY 22

Ethyl Amines

- 128 cr capex completed - out of 150 cr capex .

- 15,000 tonne - shortfall of ethyl amine. Shortfall has increased from 9000 tonnes per annum.

- No captive usage. Will be selling entirely in market

Methyl Amine – Additional capacity of 40,000 ton likely to come in by Nov 2021

Total Capex

- 150 cr for Ethyl Amine, 75 cr for DMC; Methyl amine: 300 cr ; DMF: 250 Cr (Mid of 2022)

- 70 to 80% will be funded from internal accruals

Export - Will try for 20% for FY 21. Next 1 to 3 yrs – will target 30% from exports

Balaji Speciality – yet another good quarter.

- 40 to 50% utilization currently; by mid of next yr 80% to 85%

- Volume in Q3 is almost half of 9M volumes . Likely to break even soon,

- EDA & DETA - now being exported to China; was earlier dumped to India

- Getting better price realization in China

- Can explore favourably towards merger if good show continues over next 2-3 qtr

- Witnessing improved sales run-rate of Rs 12.5cr/month

DMF – driving specialty chemicals volumes with 40% contribution.

7 Likes