Comparables analysis:

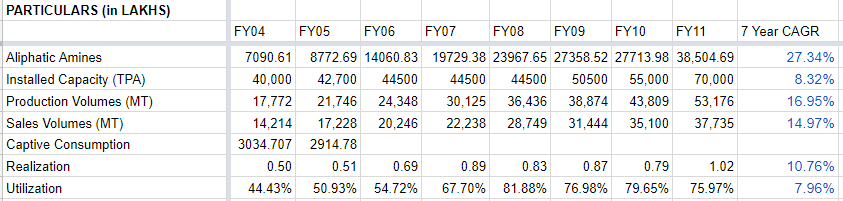

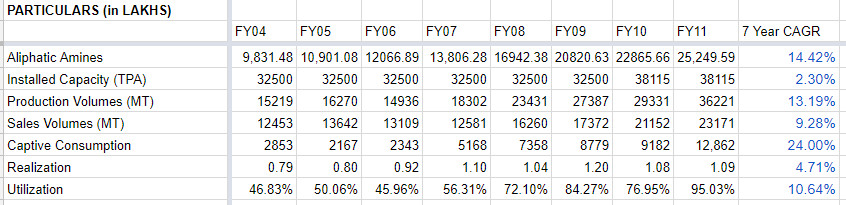

Taking figures from FY04 to FY11 only, since I could not find the data after FY12 in both the company Annual Reports.

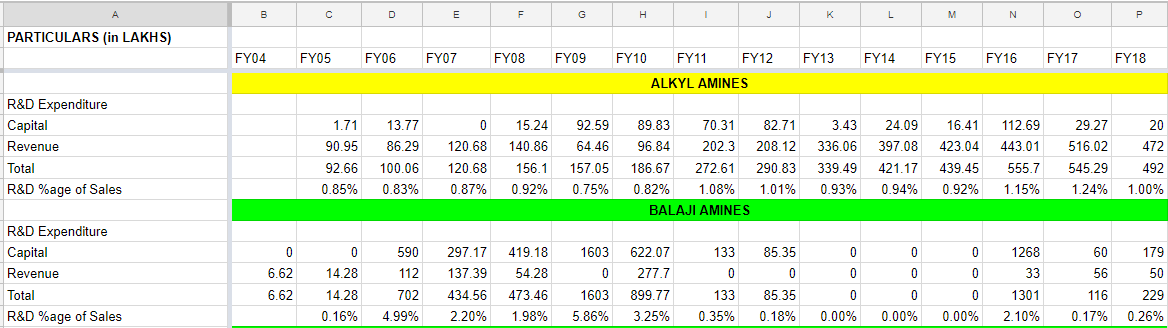

Comparative figures for Alkyl Amines

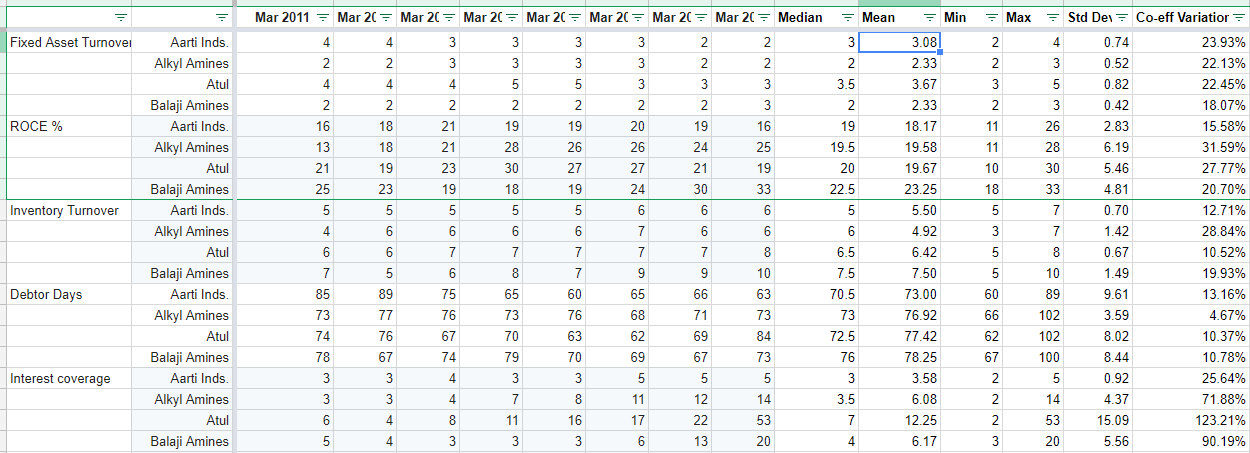

Despite BAL starting at a lower base, its revenues eclipsed Alkyl Amines by FY11. This repeats across other parameters as well.

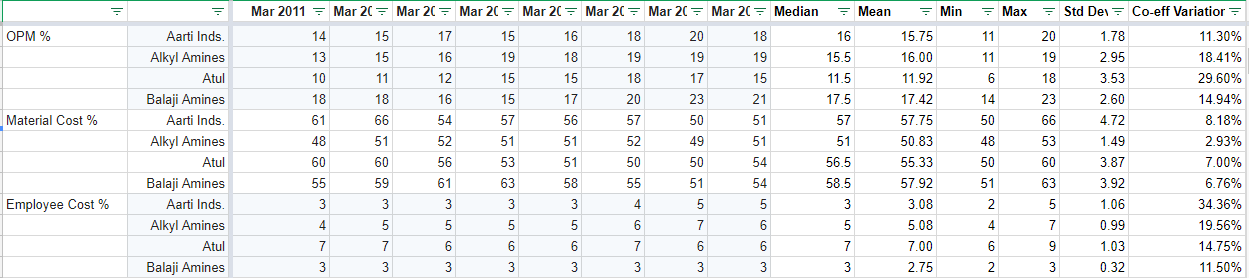

Below are statistical comparisons of key ratios

Lower the co-efficient of variation the better it is.

Closer the median is to the mean, better it is.

Comparing the R&D expenditure

Comparing Exports

BAL

Alkyl