Incorporated in 1994, Baheti Recycling Industries Ltd manufactures and trades non-ferrous metal.

Business Overview: [1]

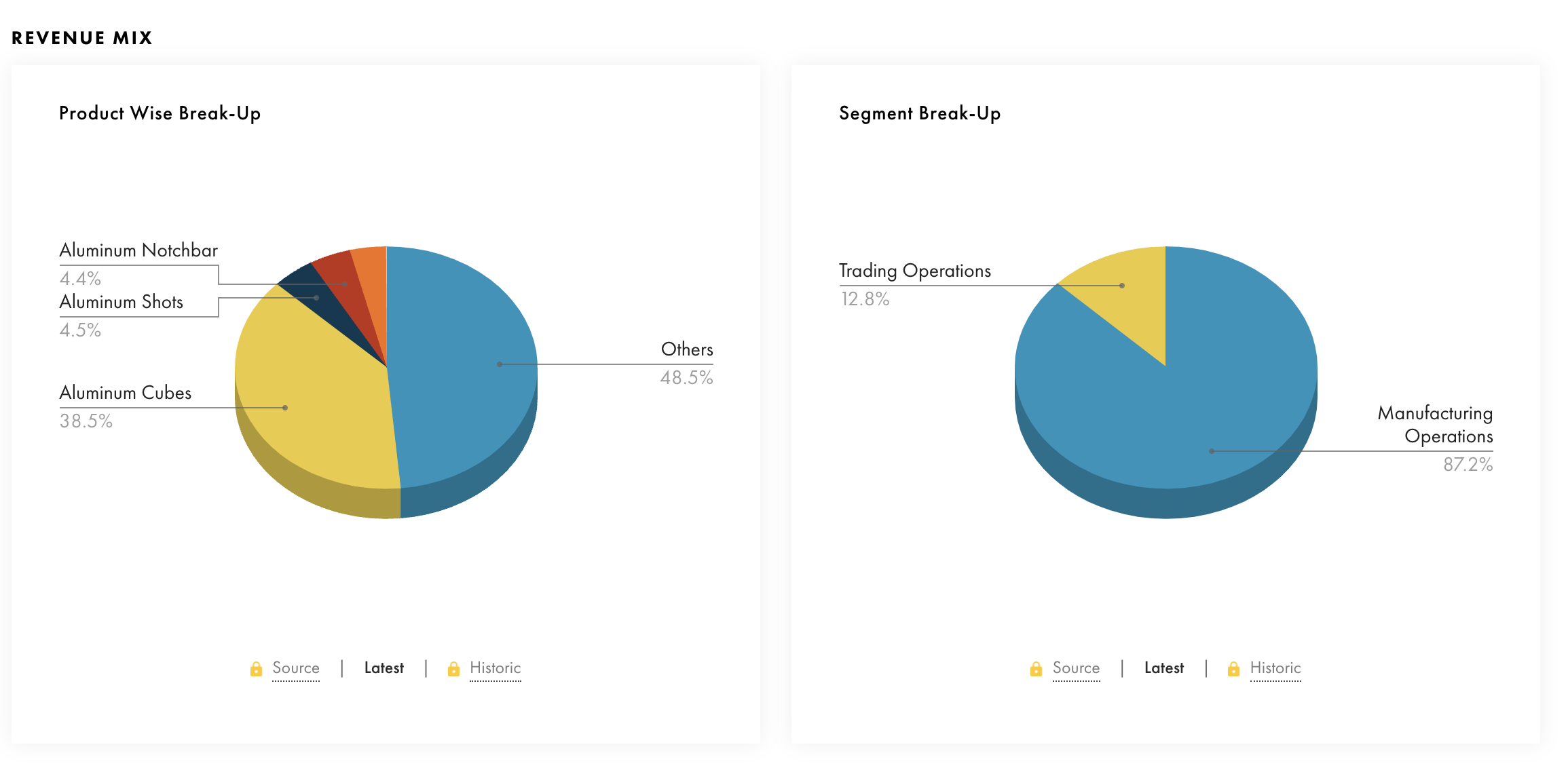

BRIL is an aluminum recycling company primarily engaged in processing aluminum based metal scrap to manufacture aluminum alloys in the form of ingots and aluminum deox alloys in the form of cubes, ingots, shots and notch bar.

Product Use case [1] Aluminum alloys are used in automobile components due to their stiffness, corrosion resistance, and strength to weight ratio, while Aluminum de-ox alloys are used as deoxidizer in steel manufacturing units.

Trading Business [1] Company is also engaged in the trading of scrap materials such as aluminum scrap, brass scrap, copper scrap, zinc scrap, etc.

Product Profile: [2]

- Aluminum Ingots:

Corrosion resistance, Seamless finish, Tensile strength, Dimensional accuracy - Aluminum Cubes:

Accurate dimensions, Fine finish, Corrosion resistance, Optimum heat tolerance - Aluminum Shots:

Fine finish, High tensile strength, Corrosion & Abrasion resistance, Easy to mould - Aluminum Notch bar:

Optimum resistance against corrosion, Fine finish, Durability, Lightweight - Aluminum Alloy Ingots:

Optimum resistance against corrosion, Fine Wrap up, Capable to withstand High Temperature, Dimensional Accuracy

Manufacturing Facilities [3]

Company’s manufacturing unit is at Dehgam, Gujarat with an installed capacity of 12,000 MT for processing aluminum. Its manufacturing facility is strategically located near some of its customers’ manufacturing facilities allowing it to optimize deliveries, and reduce lead times.

User Industries: [4]

Auto, Power, Electronics, Railways, Aerospace & Defence Construction,Solar Energy and Aluminum packaging, etc.

Geographical presence :[5]

- Domestic:

12 states & Union Territories in India, mainly in Gujarat, Maharashtra, Orissa and Jharkhand - Exports:

Japan, Canada, USA, China, Hong Kong, UAE, Taiwan etc.

Revenue Breakup - FY23: [6]

Company generated its entire FY23 and FY22 revenue from Sales of Traded Goods.

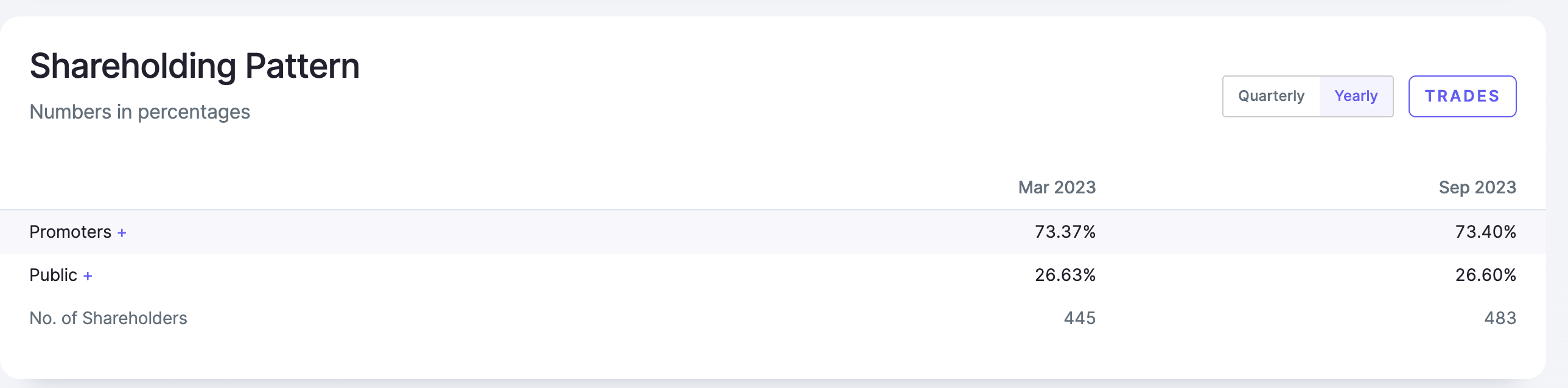

Promoter Holding

As it is new listing there is no data on how they behave but for now it is 73%

Red Flags

-

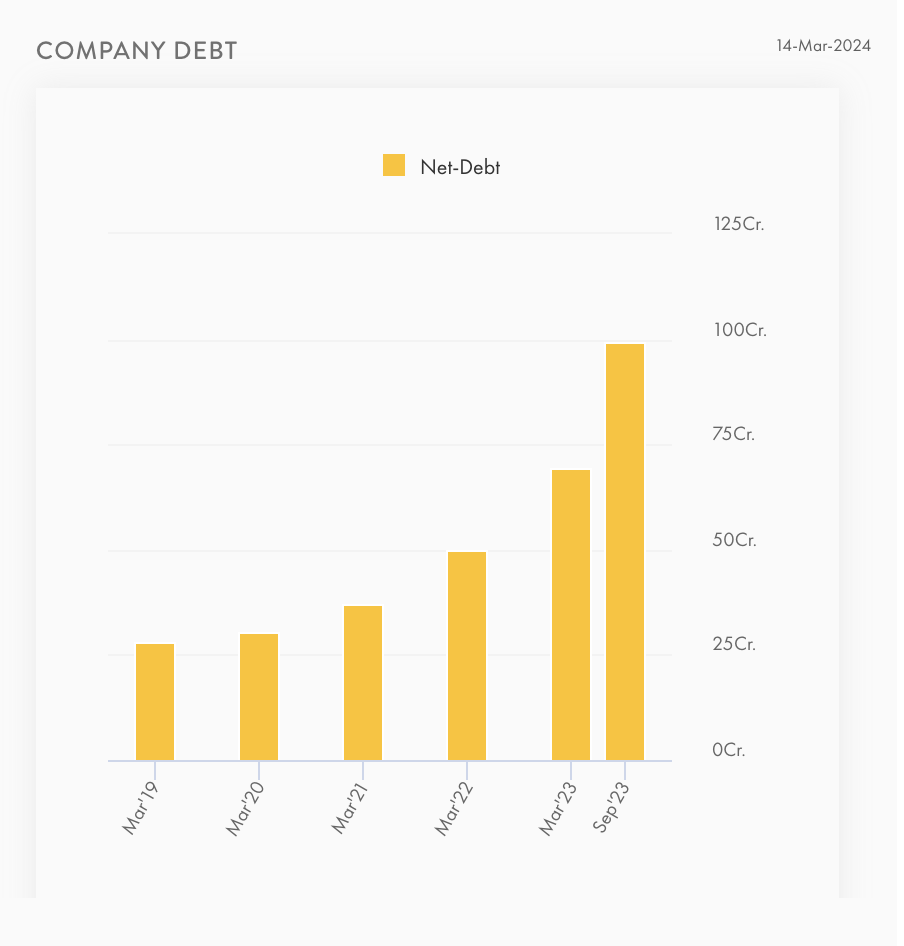

Debt

The company currently have debt of 100cr vs 180cr of market cap which is higher for me

-

CashFlows

Not sure if it is bad but there is some negetive cashflows

Good

-

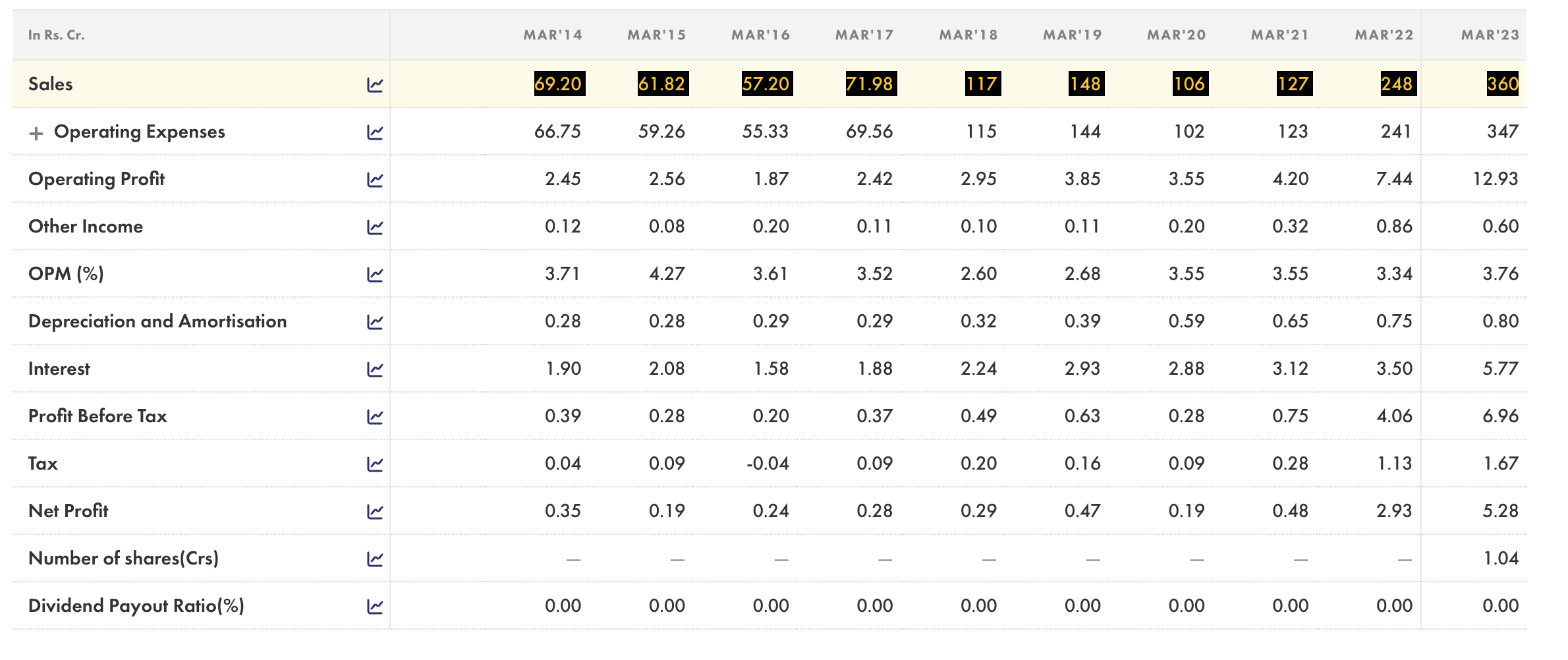

Sales Growth

The company has seen exponential sales growth in last 3-4 years

-

Profitability Ratios

I belive more in ROCE and that ratio is looking good if they maintains this then it could turn into something good. ROIC and ROE are also looking good

-

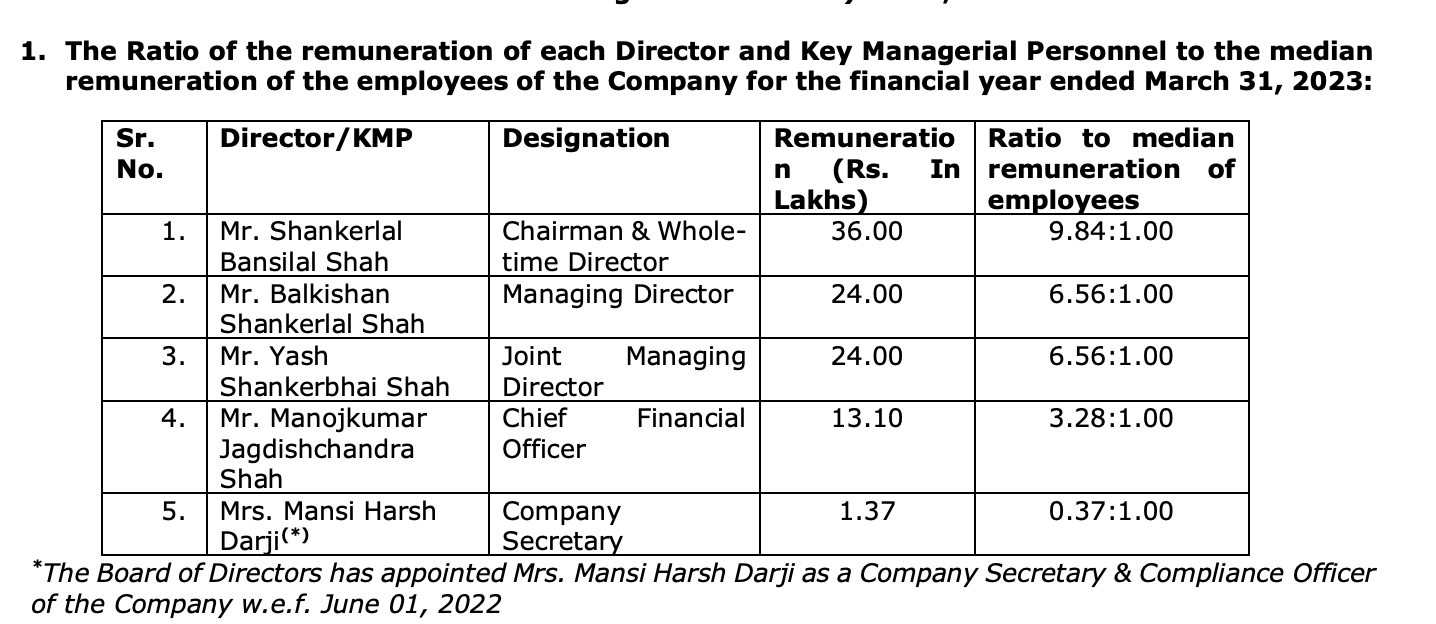

Salaries

I would say they are under control for the company of this size

I have started keeping track of this company, will make decision post March 24 results. Just for reference in Listed in Dec’22 and 4X the IPO price, so that’s also one thing to consider.