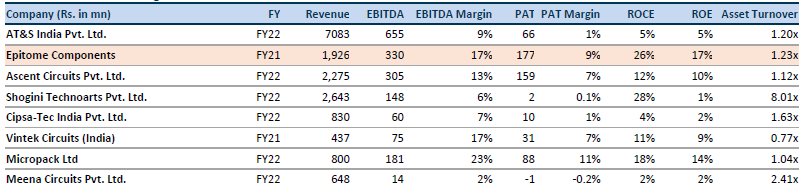

The asset turnover is around 1x for most players and margins vary depending on the complexity of PCB manufactured. PCB may be single, double or multi layered. Smartphone PCBs for example can have more than 16 layers while military electronic equipment have hundred layers.

There is another listed company called Fine line which does 30 cr of topline in the same business. Topline has been stagnant since the past 10 years.

India has been doing PCBA and backward integrating into PCB is the next natural step for the industry. How does one understand the competitive positioning or capex plans for the company going forward?

I was looking at the annual revenues of BCC Fuba. In FY19 they saw a revenue jump of almost 170% (41 Cr v/s 15 Cr in the previous year). However the operating margin was only about 1.75%. In the previous years they were making losses at the operating level. The operating margins seem to have improved in post-covid years. In FY23 it was about 10.7%.

My question is - what is the level of sustainable margins that one can expect in this industry?

I think in terms of value addition, bare PCB manufacturers do the least amount of value addition in the electronics manufacturing industry. I have seen some videos on the how bare PCBs are manufactured and it looks like there are no barriers to entry, which means there will always be competitive pressure on margins.

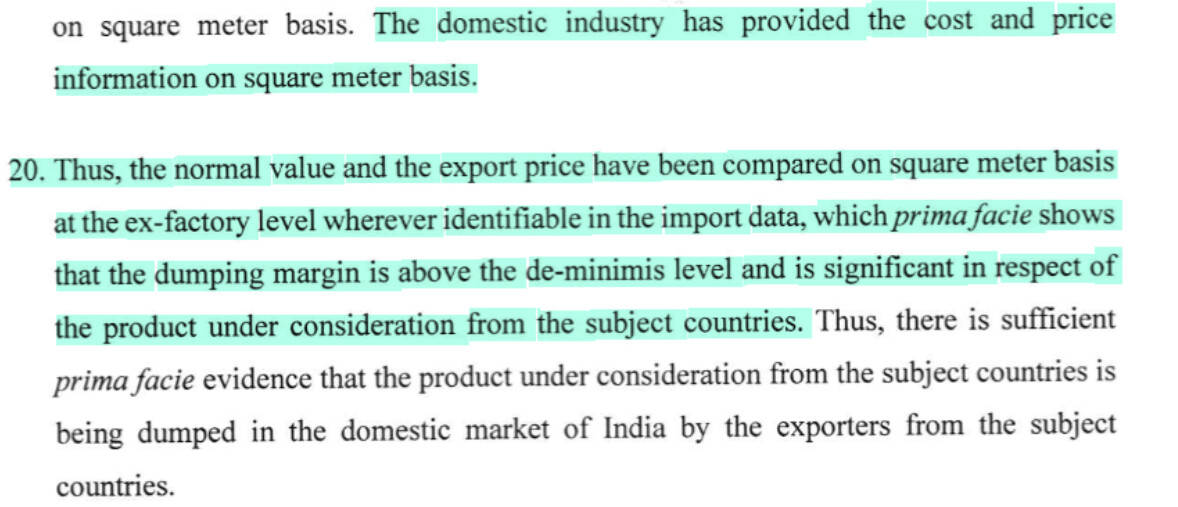

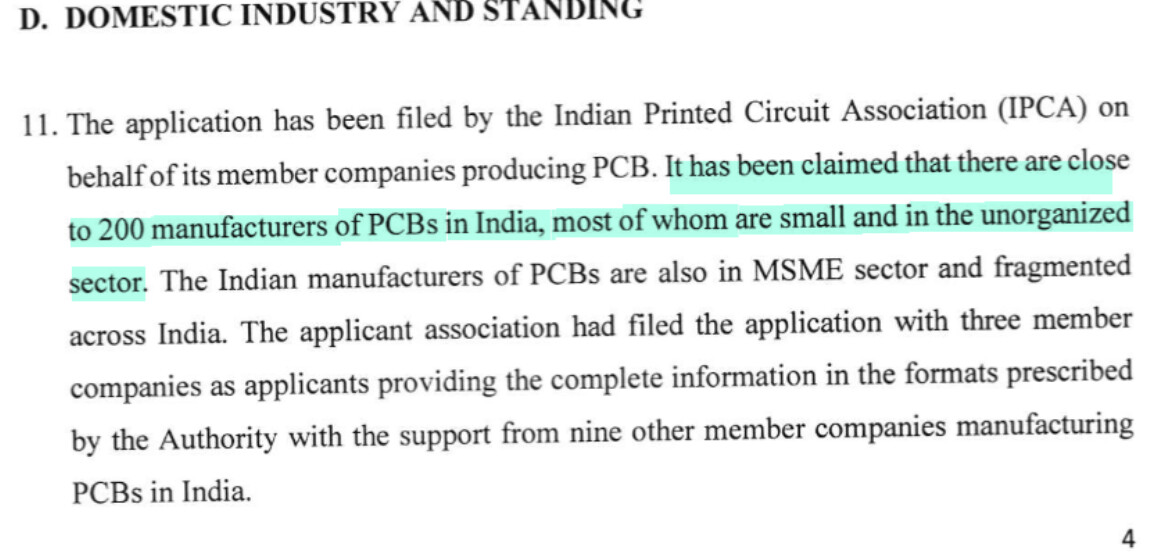

Here is latest on Anti dumping duty case status filed by IPCA(India Pcb mfgr assicoation) on behalf of PCB manaufactures in india, details for folks interested to check out are here

Prima facie there seems to be a merit in case as evaluated at time of admission

some more intersting data of industry size/ players in case details - 200+ small manufactuers, however top few players contribute a 25%+ share (per case doc) - indicates a fragmented industry - if we look at margin range as showon in above post its all over and will likely differentiate efficient players - would be worth investigating as to what are the drivers working for some players (e.g. one factor for Fuba seem to riding on Auto industry incldg EVs where it takes longer time to qualify and become supplier).

Good insights from an industry insider on potential/challenges - he sounds quite bullish for industry growth and investing for growth

While case is still ongoing and may see outcome soon, whats interesting is that players like BCC Fuba seem to be doing well (incldg AGM commentary from mgmt) irrespective of this case ADD outcome, it may create additional tailwind for industry itself if ADD were to be imposed on imports of PCB. In general clear mandate of make in india and domestic industry focus from Govt - its more likely to see favorable outcome - extent/impact to be seen.

Yes, it is automated but requires qualified technicians. Leave alone PCB, we can have finest machines but we need skilled manpower to do the job. Machines alone in isolation won’t be able to do it reliably and repeatedly until we have a well trained manpower and have learnt our lessons to deliver quality product.

Sony Financial Services invokes 10,00,000 pledged shares of Vishal Tayal, constituting 6.53% of the total shares of the company 251ea801-bfaf-4890-8e5a-a78d04c37e6f.pdf (723.9 KB)

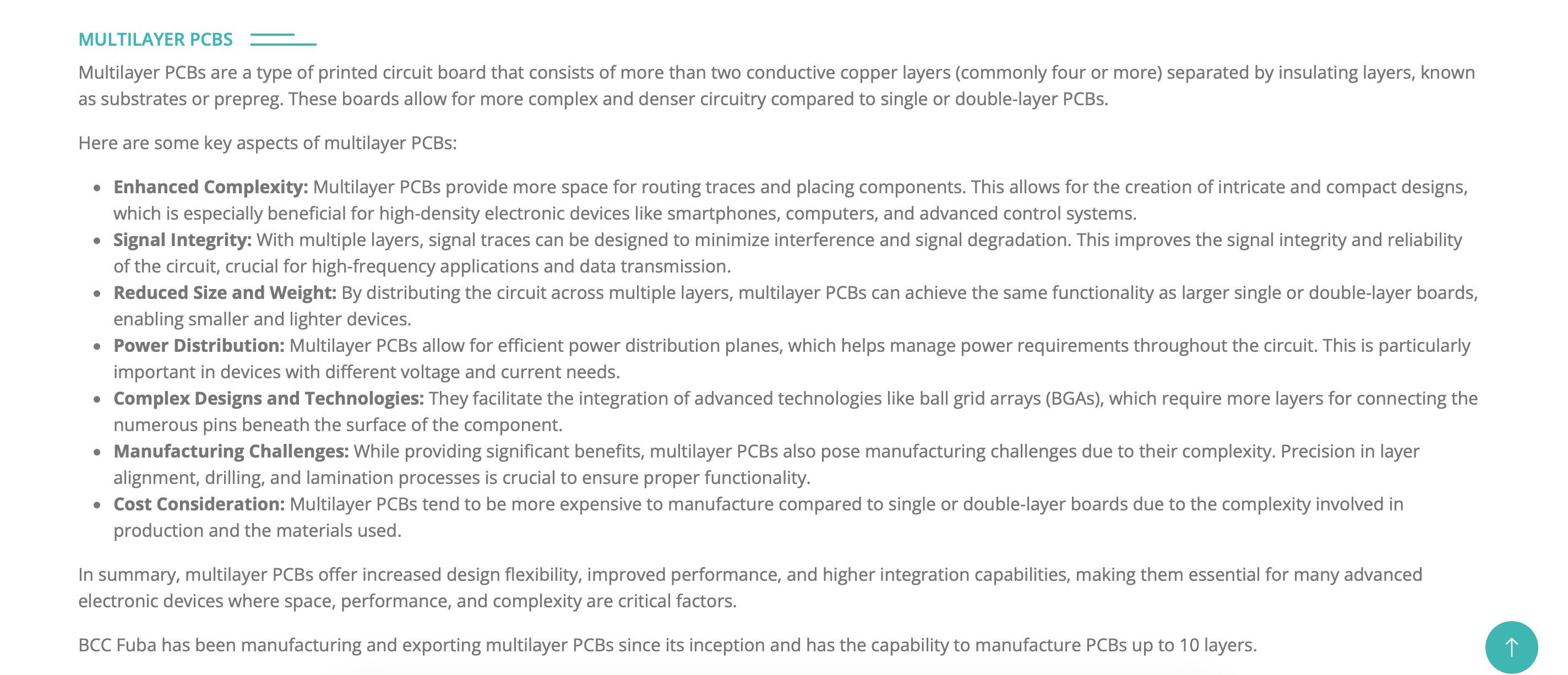

You are right there are simple PCBs like two layers and then there are multi layer impedance controlled PCBs. Another complexity is the size of pitch(ball to ball distance) that needs to be imprint to solder complex semiconductor chips. There are various kinds of materials used in different kind of PCBs, that requires material knowledge. PCB manufacturing is also understanding, a bit of chemistry. In recent budget we saw some duty on PCBs imported that shall provide some tailwind. This would take off when component manufacturing takes off Vs assembly we are mostly doing in India.

Disclosure: Invested from much lower levels.

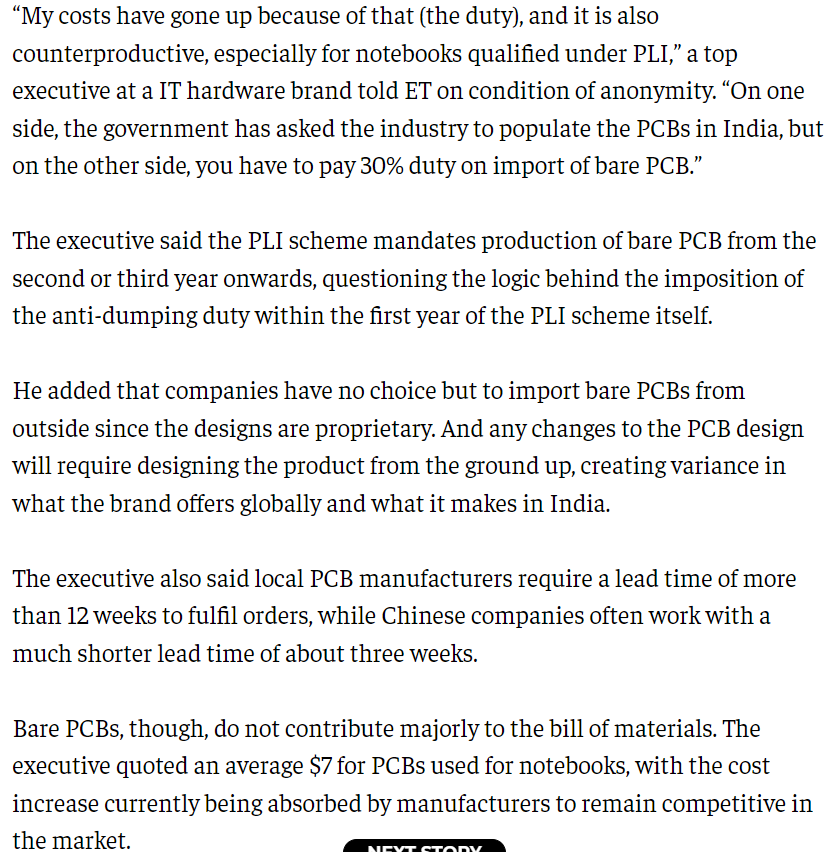

1. Do you think there is a risk of the government reducing the import duty on Bare PCBs due to the above mentioned reasons (plz refer the image)?

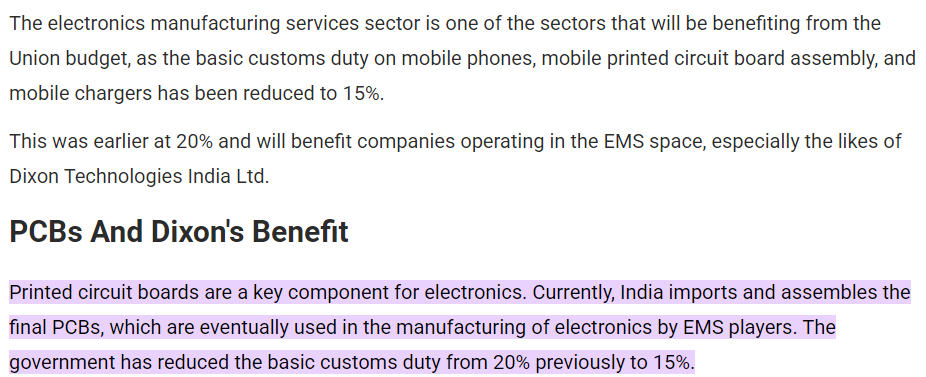

2. Also plz refer to the below image as well. It says that the govt has reduced the import duty to 15%. Am I misunderstanding something? I’m confused at one place it says the duty has been raised on Bare PCBs at another it says it has been reduced (and both are very recent news) would really appreciate some clarity

With the government focusing so much on bringing the semiconductor manufacturing and assembling in India, do we see bright prospects for local PCB manufacturers like BCC? They’re also undergoing significant capacity expansion.

We have lot of EMS companies with huge SMT lines. SMT machines solder components on bare PCBs. So basically we have more EMS companies than bare PCB manufacturers. Recently Govt offered PLIs for laptop , tablet etc. These are pre-designed PCBs and factories already manufacturing PCBs would be much more efficient Vs new PCB manufacturer. PCB manufacturing has it own share of challenges hence it is not possible for new player to start manufacturing. PCB manufacturers want higher duty so that people buy from them, however due to less PCB manufacturing capacity they are not keeping pace with EMS demand. Most of bare PCBs are still getting imported form China. Once India PCB manufacturers have enough expertise and capacity then increasing duty makes sense until them they need to keep a balance. Please remember, bare PCBs are each gadget is different and requires different level of competence. As Govt pushes more and more value add benefits we would shift to PCB manufacturing slowly and we would see scale. Few good EMS companies has already started building capability and it would all be fine in medium term.

thanks for the insights, sir!

I believe that since Indian PCB manufacturers aren’t currently keeping pace with EMS demand, companies like B C C Fuba, which have established capabilities, could benefit from the supply gap by ramping up production. The reliance on imports from China creates a space for domestic manufacturers to grow if they can scale efficiently.

The gradual shift toward local PCB manufacturing, aided by government incentives, suggests a positive medium-term outlook. If B C C Fuba continues to invest in increasing capacity and modernizing its processes, it could capture a larger share of the growing demand, especially as EMS companies develop further capabilities and shift to local sourcing.

Also as correctly pointed out by @rambaranwal, bare PCBs for each gadget, segment and industry is different and I believe B C C Fuba caters to all the most promising and flourishing sectors/spaces currently (including Automotive, power infrastructure, telecom, defense, medical, and railway). Moreover they cater to all the varied types of PCBs

As per their website,

Apologies for the delayed response, @HarshVijay. I’ve stopped tracking this company as I’ve shifted to other opportunities. If you’re invested, you might want to look into a newly listed company called Sahasra Electronics. About 87% of their revenue comes from PCB assembly, and 78% of that is exported to the USA. They also have a very high net profit margin. I’ve only glanced at it, so I haven’t done a deep dive, but it could be worth exploring further if you’re interested in this industry.