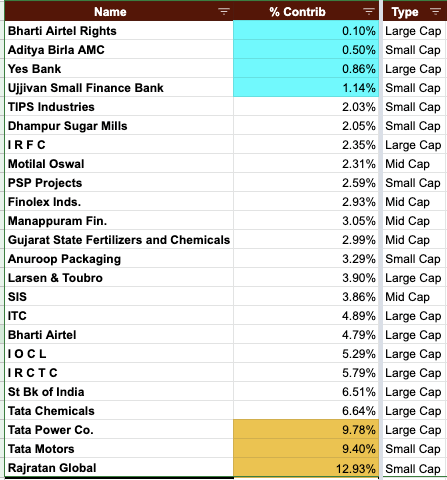

I have the following Portfolio, from lowest to highest contributors, haven’t cut down on my winners except IRCTC, which is currently trading at crazy levels. Been averaging up in most stocks since I brought them, as I like the businesses.

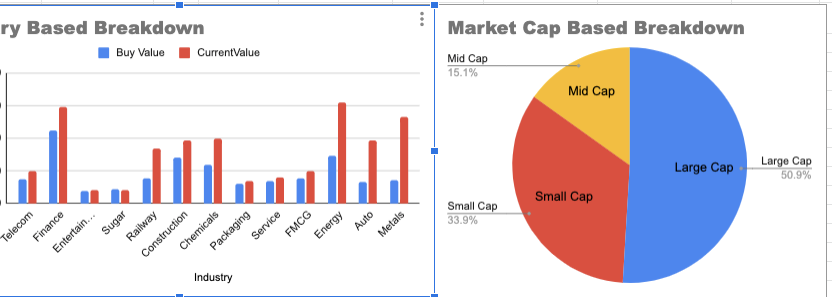

This is my current Industry and Market cap based breakdown:

Your thoughts/suggestions on my Portfolio? I hold 24 stocks currently, I’m wanting to cut it down to 14-15 stocks, with 30% allocation to relatively stable companies(Dividend paying largecaps at reasonable valuations) and rest in high growth prospect companies(Preferably midcaps or big small caps).

I don’t mind volatility in my portfolio(have seen it swing -4% in a day and +5% in another day with no reaction to it).

You should explain why you invested in these particular stocks & what’s your time horizon.

Also, I would say, trim everything that’s less than 4% of your portfolio, the time spent in studying those is not worth the return. Or you could either increase the investment in those to take them above 4%.

@Shakti_Srivastava@sham72942 have updated my reasoning for it. Some are pretty naive, have been investing for 2 years(Seriously for last 6 months only). All the No’s are the one’s I’m thinking of exiting.

Name

% Contrib

Solid reason to hold?

Reasoning

Aditya Birla AMC

0.52%

Yes

Good AMC only business, a good growth pathway and industry tailwinds, relatively cheap as compared to others in this industry. Also was brought in IPO.

Anuroop Packaging

3.52%

Yes

Yes, microcap with a changed promotor focusing on automating its factory, available at reasonable price. Also has a long list of clients which are ready for more orders if their capacity permits.

Bharti Airtel

5.33%

Yes

Duopoly in telecom, but more tech focused, especially with recent deals with streaming service providers and building great ISP infrastructure.

Bharti Airtel Rights

0.11%

Yes

Duopoly in telecom, but more tech focused, especially with recent deals with streaming service providers and building great ISP infrastructure.

Dhampur Sugar Mills

2.04%

No

Only for industry tailwinds from ethanol push, would be a big winner with soaring petrol prices and govt push for ethanol. Also, UP ethanol plants are in much better position than others. Likely to exit soon.

Finolex Inds.

3.11%

Yes

Reasonably priced, has shown good growth in past

Gujarat State Fertilizers and Chemicals

2.95%

No

No solid reason

I O C L

5.44%

Yes

Brought it for the dividends at all time lows

I R C T C

2.29%

No

Has gotten extremely expensive now, sold off more than half stake in it, will sell off rest once price stablizes

I R F C

2.45%

No

Thought it to be a proxy on railway development in India, has been consistently growing in terms of sales and profits, but I dont understand the business well enough, will probably sell.

ITC

4.93%

Yes

Brought at lows for the Dividend. Also a good business being ignored by market for 2 reasons: sin stock and poor capital allocation.

Larsen & Toubro

4.23%

Yes

Infrastructure tailwinds, one of the biggest infra companies in India with good growth and consistently growing, bagging new and notable projects.

Manappuram Fin.

3.24%

No

Want to cut out financial companies, dont understand them deep enough.

Motilal Oswal

2.44%

No

Multuple business areas not performing well, spread too thin, not a focused company. Also not ready to adopt good tech like angel broking. Most of its profits are just paper profits

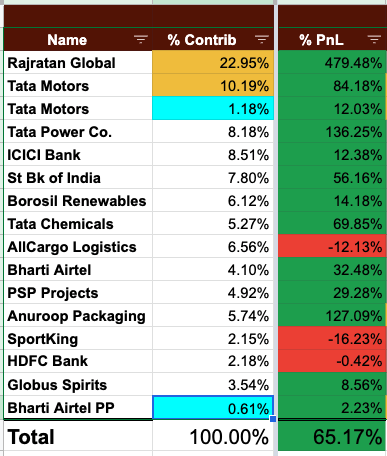

PSP Projects

2.79%

Yes

Good in terms of orders in pipeline, revenue growth and project execution with minimal debt. Very efficient in terms of project completions. Risk: Getting projects could be due to political connections

Rajratan Global

13.16%

Yes

Huge customer base, have some pricing power, expanding capacity rapidly, setting up a new plant in Thailand and South india, no competitor currently in segment in which they operate.

SIS

4.04%

Yes

Increasing market share in Australia, Barrier to entry is high as they have presence in every tier 1 & 2 city with multiple offices, management’s focus on shifting towards tech could increase profit margins from the same customers. Risk: Tech like this is easy to develop

St Bk of India

7.02%

Yes

Improving asset quality, reasonably priced, growing customer base(also customer loyalty due to trust factor), huge AUM for MF business, Risk: Govt controlled, has been asked to save multiple companies by taking a hit(Yes Bank most recently)

Tata Chemicals

6.71%

Yes

Yes, strong book value and expansion in other areas(Especially EV) with improving margins and China + 1 play

Tata Motors

9.66%

Yes

JLR business finally getting under control. Short term could be jittery due to chip shortage, but it has first mover advantage in EV, has a huge booking backlog to clear and sales are improving. PLI scheme and Vehicle scrapping policy, could be a huge boost to it.

Tata Power Co.

9.30%

Yes

Toll tax business for the future, everything would work on electricity. Have been expanding renewable energy capacity at breakneck speeds and it has started to pay off. Investments would go down after 3-4 years, and existing infra would continue earning similar revenue

TIPS Industries

2.20%

No

Brought at somewhat expensive levels, given the industry transformation that is happening. Could be a bad bet, would want to get out of this soon, maybe buy back at loower levels in future

Ujjivan Small Finance Bank

1.62%

No

Short term bet on revival with very low capital invested

Yes Bank

0.89%

No

Short term bet on revival with very low capital invested

Read the reasons yourself & you know which ones to trim out, for ex

Reasonably priced, has shown good growth in past: Don’t focus just on past see instead growth oppourtunities.

Short-term bet on revival with very low capital invested: We don’t gamble in the stock market.

would want to get out of this soon: Please as soon as possible.

Multuple business areas not performing well, spread too thin, not a focused company. Also not ready to adopt good tech like angel broking. Most of its profits are just paper profits: Why are you still invested?

Want to cut out financial companies, don’t understand them deep enough: Please cut them if you don’t understand

None of the suggestions are based on stocks, but instead only on your reasonings

This also has good growth opportunities in future as well. It is a market leader in agriculture pipes and has a strong brand name. Also existing competition from local manufacturers will be lowered and a licensing wall being set up will act as a barrier to entry for newer players. They’re also continuously growing their manufacturing capacity. In comparision to their peers, they seem to be available at a much lower valuation.

I was probably no clear enough on what I meant by bet. It was in terms of Mohnish Pabrai’s Dhandho concept. I want to keep these as my Coffee Can stocks and only want to keep 2-3% of my Portfolio in these.

Will cut these out. I cant currently because of compliance reasons at work(Need to hold any stock I brought for at least 90 days from the day I brought it last).

What are your thoughts on the other stocks present in the portfolio, any reasoning you don’t agree with:?

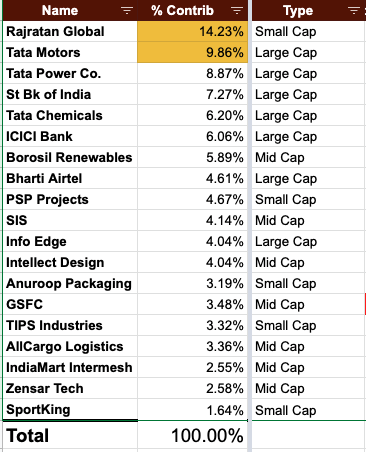

Made some progress on removing stocks I didn’t have much confidence in or was holding on to without any solid reasoning. Also added all stocks in my portfolio with at least 1.5% weightage.

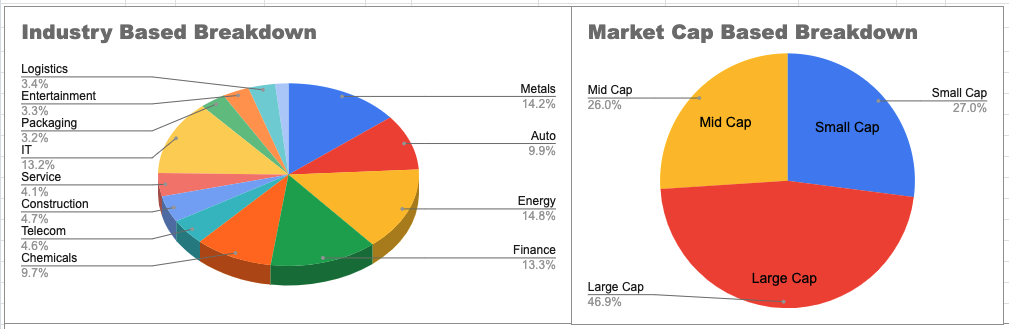

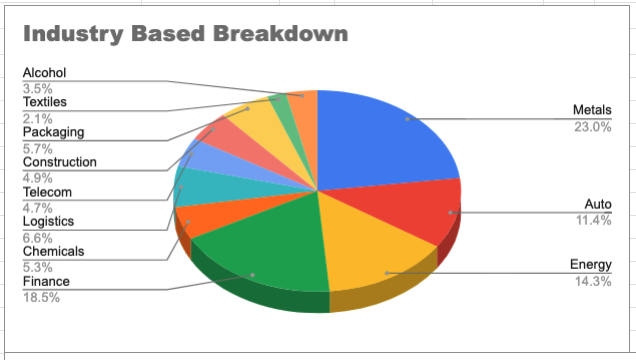

Industry based breakdown and market cap based breakdown of current PF

Reasons for cutting out some stocks from previous update

Removed Ujjivan small finance bank and yes bank: Low quality, used the capital to invest in more robust companies.

Removed Motilal Oswal: Looking at ICICI Sec or Angel broking currently as they’re in similar business but have been much more adaptive to the current scenario. Also they’re more focused in terms of the area they operate in and also more tech focused and have increased their user base substantially.

Removed LT: Feel like GR Infraprojects could be a better substitute. It is growing very fast and consistently. LT also seemed a little overvalued at 30+ PE with a 6% 5 year avg sales growth

Removed ITC, IOCL, IRFC: Good businesses but I’ve changed my view from dividend to growth investing, especially given the 30% tax on dividends.

Dhampur Sugar Mills: Ethanol play working out for the industry, especially given the Russia Ukraine situation. I removed it from my portfolio after its recent run up.

Next steps I’m planning:

Currently planning on cutting down on some IT stocks and add a little bit more of Sportking. I find the business to be really high quality combined with being at the right time to be expanding.

TIPS: Need to watch it for a few quarters to understand the consistency of revenue and profits as recent past has been fluctuating. Especially as streaming seems to be gaining more steam.

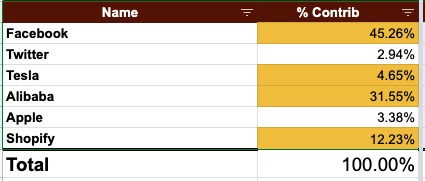

Apart from the above, I also added some US stocks to my portfolio:

Strongly believe all these stocks fell with the broader market unnecessarily and their growth story is still intact, especially Facebook and Alibaba which seem deeply undervalued to me. Brought almost all of them at their absolute bottoms around 1-2 weeks back.

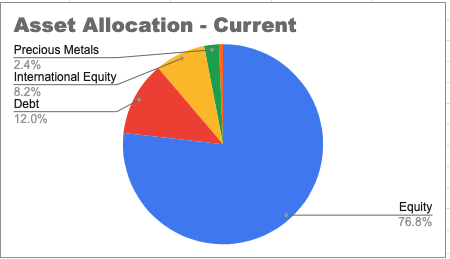

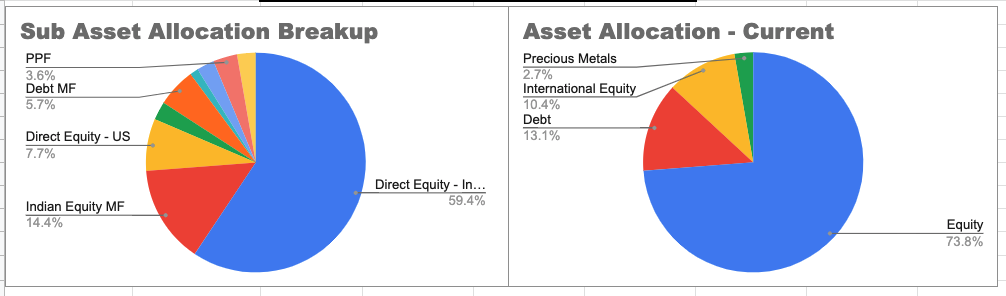

Finally my asset allocation looks something like this:

Based on earlier suggestion of cutting everything less than 4%, I don’t feel like that’s a right strategy for me as I like to add a stock with <1%(just to have some skin in the game) and then dive more into it. If I feel confident enough in the business and current valuations, I start adding more slowly, else I exit.

For Sportking, do you have any update on their expansion plans. I also have a tracking position on Sportking but since they dont have any disclosures(ppts, concall etc) dont have a conviction on their growth path, business fundamentals etc.

How do you build a conviction on a stock like Sportking when disclosures are not there. The company looks good to me from various aspects but since disclosures are not there(not even PPT) i an thinking of moving out of it. Whats your view on this ?

Moved out of short term investments before the recent fall. Got stuck in some with heavy losses.

Intellect design was one of those.

What happened: Stock kept falling and promoter kept selling, business was solid and they were getting deals every other week. But due to falling market and sharp correction in this stock with promotors selling every week, lost confidence and sold with ~20% loss.

Lesson Learnt: Watch the business for some quarters before taking decision to exit. Especially if you’ve researched and followed the stock for previous 1-2 quarters.

Got out of SIS, GSFC, IndiaMart, TIPS, Info Edge and Zensar.

Reasons:

For all 3 IT stocks: Attrition and wage correction. It is a huge risk for these companies and will cause margin compression.

TIPS: Seeing what happened to a solid business like spotify and the valuation metrics for TIPS, made sense to exit. Also, not a lot of great content is being produced by them and they might end up like Netflix with derating.

GSFC: Sold around peak. No reason as such, was my least conviction stock.

Had brought GR Infra during this time, but got out of it ASAP with CBI and IT raids on them. Faced ~7% loss but worth it for me as I do not want to lose sleep over a business which might have potential corporate governance issues. Want to avoid this risk almost always.

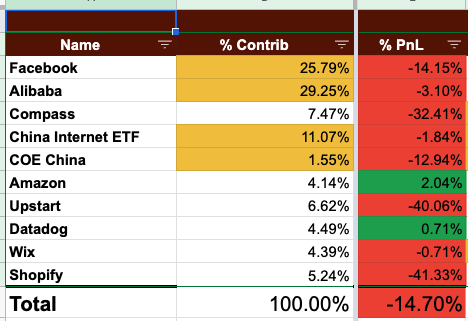

While I managed to cut down on India stocks, US/Chinese stocks were too hard to resist for me.

Portfolio is in deep red, but I have high conviction on all of these businesses. Will keep adding quality businesses like Datadog and Alibaba. Also thinking of adding Atlassian to this list. In short term Facebook will be a looming risk to my portfolio, depends on how it does with its earnings over next few quarters.

Compass and Shopify will continue to struggle through under US slowdown, but again they have come down a lot from huge valuation bubbles and are good businesses, looking like good investments finally. Will add them when I see conditions improving, holding on them for now.

The tech platforms these all have are HUGE moats and are No. 1 reason for me to be invested.

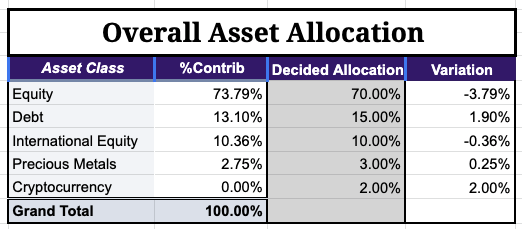

Overall portfolio asset allocation looks like the following:

I had exited Crypto(Had only about 1% allocated to it) during march to avoid any tax hassles. Bitcoin looks good now, but would wait for the crypto exchange scam dust to settle before I buy in any more of crypto.