Found no thread for the company hence starting one… I have no investment here. Just starting a discussion on a pure commodity story to see if any investment thesis can come out through deliberation.

Welspun Syntex is a company in Welspun Group manufacturing POY (Partially Oriented Yarn) and FDY (Fully Drawn Yarn) … The product list is available here

http://www.welspunsyntex.com/content.asp?Submenu=N&MenuID=12

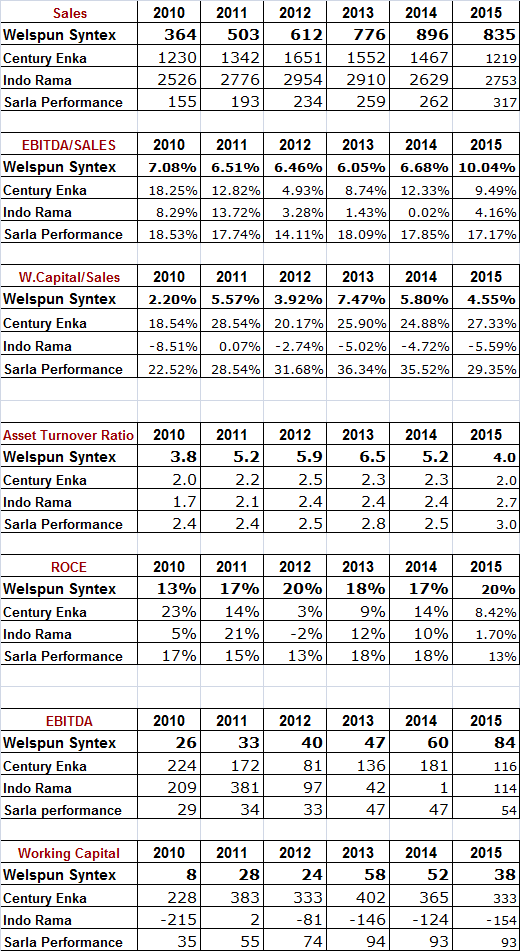

The finacials of the company can be checked from Screenr site.

The Global and Indian demand supply scenario is available here DEMAND SUPPLY.pdf (158.9 KB)

The main Raw Materials are PTA (Purified Terephthalic Acid) and MEG (Mono Ethylene Glycol). Both are downstream products of Naptha as depicted in the following diagram Naptha Downstream.pdf (270.1 KB)

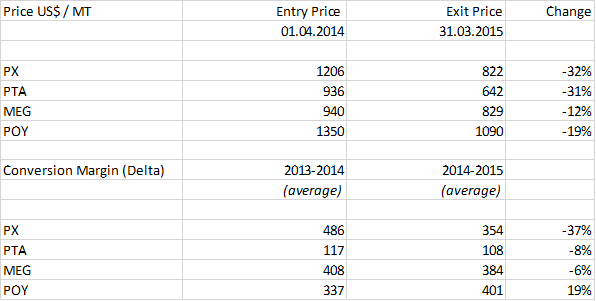

60% to 80% of the product cost of POY and FDY are PTA and MEG. Also, as per Welspun "Margins of POY producers are calculated as domestic prices of POY (126 D) less the raw material prices of PTA and MEG (0.86 units of PTA

- 0.33 units of MEG per 1 unit of POY)".

Presently cost of PTA is about Rs. 68 - 72 per kg and MEG about Rs. 63 - 65 per kg. Sale price of POY is about Rs. 110 - 125 per kg. (All data from Filatex Limited 2014 AR) . But fully drwan, dyed, texturised arn price varies significantly depending on various quality parameters. One can get a good idea of the wide price range from the below link

Main PTA producers are BP, Amoco Chemicals, Alfa Mexico, Reliance Industries Ltd, Mitsubishi Chemical Corporation (MCC), Sinopec, Zhuhai Biyang Chemical Co., Luoyang Petrochemical Co., Tianjin Petrochemical Co., Xiamen Xianglu Petrochemical Co., and Jinan Qilu Group Synthetic Fiber Co.

Technology licensors for PTA are Dupont, Mitsui, Dow/Inca, Mitsubhishi, Tuntex, Interquisa, Eastman, Lonza and Hüls/Witten.

Main MEG producers are Shell, Equistar SABIC, INEOS, LyondellBasell, Reliance Industries Ltd, Akzo Nobel, BASF, Clariant, Dow Chemical, Huntsman, LG Chem, Mitsubishi Chemical Corp, Mitsui Chemicals, Sasol, Shanghai Petrochemical, and Sinopec.

In India PTA capacity is about 7.1 million TPA and main producers are RIL, IOC (Panipat), MCPI (Haldia) and MRPL.

In India main MEG producers are RIL. IGL and IOC. Total capacity is about 2 million TPA. India has presently shortfall of MEG and import is made from Saudi Arabia, Kuwait and Singapore.

POY and FDY are inputs for making Polyester Fabric and global usage pattern of pattern of Polyester / Cotton is 60 / 40 while in India it is reverse (40 / 60) and varies inversely with Cotton Price. In India the demand is rising around 4% - 6% per year.

Industry characteristics are well summarised in Welspun Syntex AR 2014. It says,

“Overcapacity is the main characteristic of the domestic POY industry with operating rates declining to about 61 per cent in 2012-13 from 67 per cent in 2011-12. Demand for POY is mainly impacted by the comparative prices of cotton yarn, blended yarn, and VSF, and also their relative availability. In 2012-13, margins for POY players remained under pressure to average at Rs 13 per kg because of high input prices and overcapacity.”

Margin of POY players were about Rs. 24/- per kg in 2008. However, as Welspun is continuously increasing the sale of Dyed Texturised Yarn (almost 85% of sales), it would be interesting to know their average price realization per kg of the FDY.

Their export sales is about 25% of total revenue.

In India the main competition is from Filatex, JBF Industries, Indo Rama, Raj Rayon etc. but Welspun as lowest RM cost among them at about 60% - 65% compared to 70% + for all others. Also in 2015, their EBITDA margin on YOY basis improved from 7% to 10% … During this period PTA and MEG price didn’t go through any wild variation. Net profit more than doubled between 2014 and 2015.

Technology and Infrastructure is almost standardised in this industry… Either you get it from PFY manufacturing company like Dupont, Samsung, Hitachi, Teijin, Enka or from Engineering companies like Zimmer, Lurgi, Chemtex, Didier, Inventa, Oerlikon Barmag, TMT Machine (Japan) … Second option is cheaper and less efficient but seems from the technology used by Welspun, they preferred a bespoke engineering route to create its capacity.

Presently, none of the financials look very appealing … Profit fluctuating, uncomfortable interest coverage and huge repayments (about Rs. 23 - 25 crore for next 4 years) due in coming years… However, promoters increased their stake by about 5% in last six months through open market purchase.

How they go up in the value chain in coming years, if at all in this commoditised industry may be something interesting to watch out. Generally, one / two players always come out winner in a commodity play.

Add your inputs …

Also, the pains you take to concise the links and highlight the relevant information only!!

Also, the pains you take to concise the links and highlight the relevant information only!!