Axtel industries Ltd. is engaged in the manufacture of custom designed food processing plants and machineries as per the requirements and specifications of food and pharmaceutical industries. The company was founded by Shri Ajay Nalin Parikh and Mr. Ajay Desai in 1992, both of who continue to be Executive directors with Axtel Industries Ltd. since its inception.

Industry Landscape: The process equipment industry for food can be categorized into two different kinds depending upon the complexity:

-

Standardized equipment: These are standardized equipment like flour mills which are more capacity driven and does not require much engineering skill.

-

Specialized custom equipment: These are specific equipment which requires highly specialized design and engineering capabilities. The equipment is built to specifications from client and requires deep understanding of food handling, flow engineering, electrical and automation capabilities. This is dominated by European and American players like Buhler, SPX, GEA Group, Russell Finex, Rockwell, CM-OPM etc. These companies specialize in certain equipment and a product line (e.g. a chocolate line for Nestle) would generally involve equipment from some of these. Most large food companies have internal design teams who work with these companies to come up with designs who work with these companies to develop the right process and equipment. The smaller companies can hire external consultants for this part.

Axtel manufactures highly specialized process equipment for food industry. They have capabilities right from Project advisory-> Process Systems->Process Equipment. The company provides process systems for the following food industries:

Why Axtel?: Axtel operates in a field which is currently dominated by the European companies. For any large food company the cost of setting up a line is very low as compared to the impact a faulty/badly manufactured line can have. This results in orders going to the existing set of suppliers who have a proven track record of quality. This also creates large entry barriers for newer players and also explains why despite being in business for 28 years Axtel’s turnover is just 110 cr. Today though Axtel has a large range of both International and Indian food companies as its client including Nestle/Mondelez/Hershey’s/GSK/Puratos/ITC/HUL/Heinz/Kellog’s etc.

https://www.axtelindia.com/ourclients.

Axtel has a very large opportunity ahead as the packaged food industry/packaged chocolate is growing at over 15% in India and with Axtel having relationships with all large players in these segments it is well poised to exploit this opportunity. There is also an opportunity in automating the existing facilities to reduce manpower costs. The other large opportunity is the export market. Axtel with its high quality products, international relationships and large labor arbitrage vis a vis the European players can grow significantly in the export markets.

Financials:

| (in Rs. Cr) | FY19 | FY18 | FY17 | FY16 | FY15 | FY14 | FY13 |

|---|---|---|---|---|---|---|---|

| Sales | 111 | 82 | 76 | 67 | 40 | 48 | 60 |

| PAT | 13 | 6 | 7 | 5 | -8 | 3 | 3 |

| Gross Margin | 50% | 50% | 52% | 53% | 50% | 57% | 41% |

| EBITDA Margin | 20% | 12% | 14% | 15% | -6% | 19% | 11% |

| PAT Margin | 12% | 7% | 9% | 7% | -19% | 6% | 6% |

| RoE | 25% | 15% | 20% | 17% | -29% | 11% | 15% |

| Cash Conversion Cycle | 69 | 70 | 80 | 87 | 156 | 98 | 84 |

| Dividend (in Rs. Cr) | 1.5 | 2.4 | 0 | 0 | 0 | 0 | |

| Domestic Sales | 65 | 59 | 66 | 32 | 46 | 54 | |

| Export Sales | 17 | 17 | 1 | 8 | 2 | 6 | |

| Inventory | 21.7 | 17.8 | 12.2 | 13.7 | 17.8 | 10.8 | 7.65 |

| Trade Receivables | 19.4 | 20 | 18 | 18 | 13 | 17.6 | 17.2 |

| Advances from Customers | 11 | 11 | 6 | 6 | 11.7 | 1.7 | 4.2 |

| OCF | 9.1 | 11.8 | 15.1 | -1.2 | 6.7 | 8.28 | 1.26 |

| Debt | 1 | 4 | 5 | 10 | 12.5 | 17 | 15 |

| Cash + Investments | 20 | 18 | 7 | 1 | 6.3 | 1.7 | 1.3 |

| Net Block | 16 | 17 | 18.3 | 18.3 | 21 | 24.2 | 16.8 |

| CWIP | 0.2 | 0 | 0.3 | 0 | 0.3 | 0.4 | 0.3 |

| Intangible Assets | 0.3 | 0.3 | 0.2 | 0.37 | 0.07 | 1.2 | 2.7 |

| Discount/Debts Written off | 1.3 | 0 | 0 | 0.18 | 0.7 | 0.13 | 0.35 |

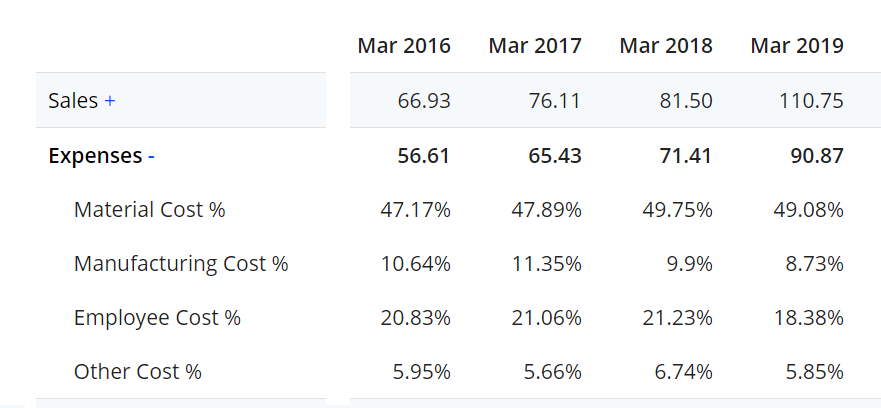

As is evident from the financials Axtel’s sales have grown steadily from 40 cr to 111 cr in last 4 years. What is more heartening is the improvement in margins, operating cash flows and virtually zero debt. The company’s RoE today including the cash+investments is a healthy 25%. Axtel had one bad year in FY15 which was probably due to order cancelations from a significant client.

Risks: Axtel operates in cap goods and there can be significant volatility in QoQ and YoY performance depending upon demand supply to order execution. Axtel is a microcap with 110 cr sales and 180 cr market cap. Small caps have inherent profitability and business performance risks. Investing in small/micro caps comes with liquidity risks.

Disclosure: Invested with 5%+ holding. Views are biased please do your own due diligence. I am not a SEBI registered advisor and this is not a stock recommendation.