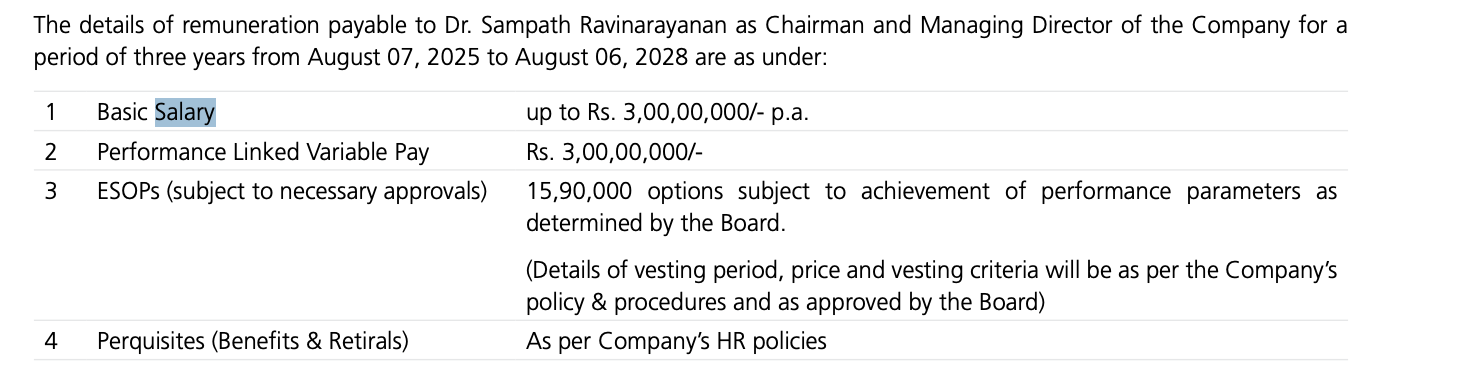

This salary is very high. Very surprised to see this kind of renumeration in such a small company.

3 Likes

AXISCADES TECH announces strategic electronics, semiconductor and artificial intelligence (esai) division wins powered by its unit mistral solutions

- High growth and futuristic theme with good Govt/ Private sector demand.

- Good wrt diversification too

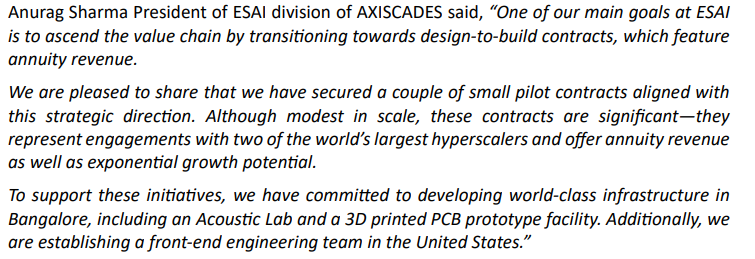

- They’re now scaling Mistral’s capabilities under a broader ESAI umbrella.

- Axiscades can be viewed as semiconductor + AI solutions company,

Also, more into the infra investments :

- An Acoustic Lab in Bangalore.

- A 3D printed PCB prototype facility.

- A front-end engineering team in the U.S..

Pilot Wins with Hyperscalers

- They’ve signed two pilot contracts with two of the world’s largest hyperscalers (likely Google, Amazon, or Microsoft).

- These are small in scale (~$1 million total value) but strategically very important since they bring annuity revenue potential and open the door to long-term, scalable engagements.

7 Likes

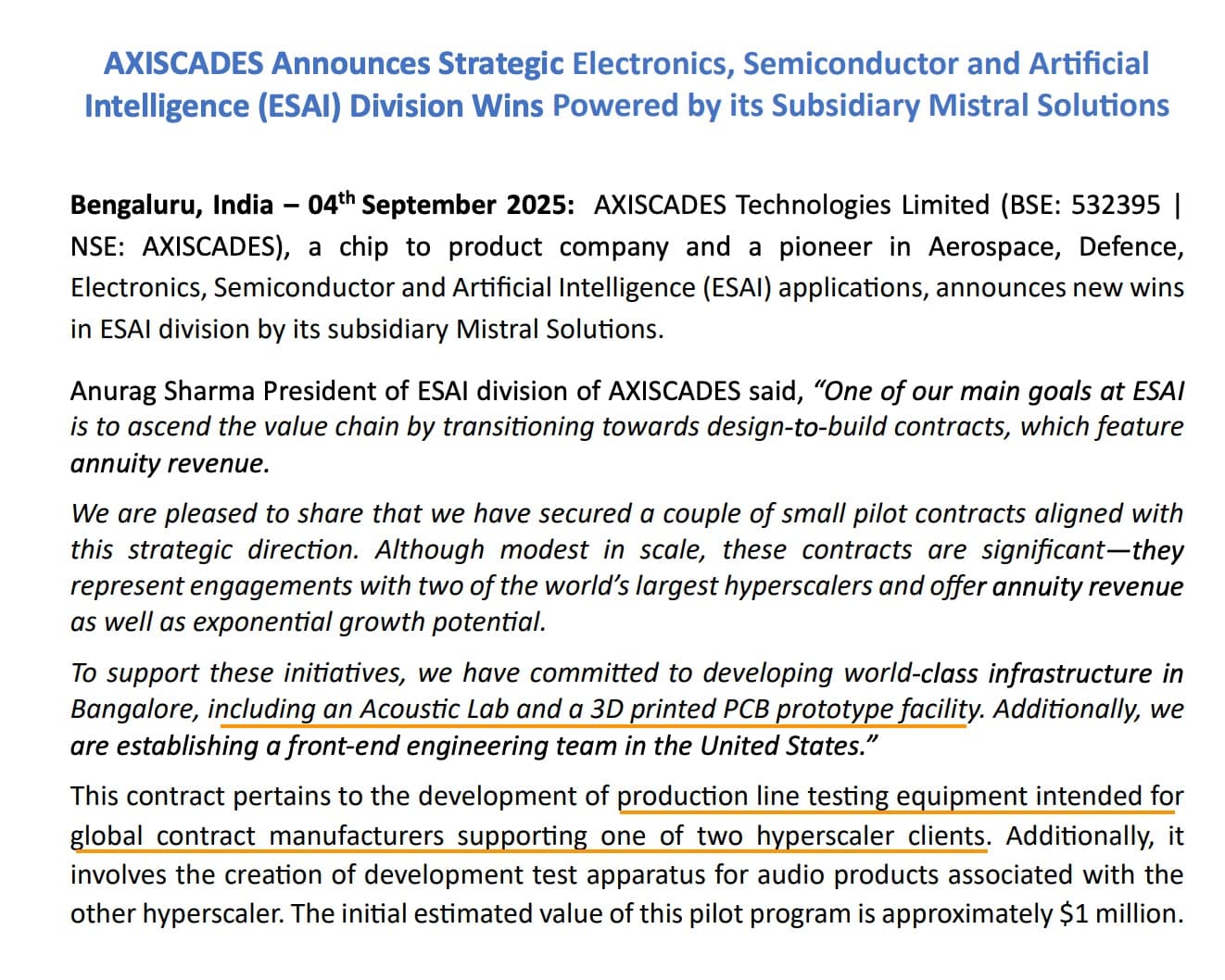

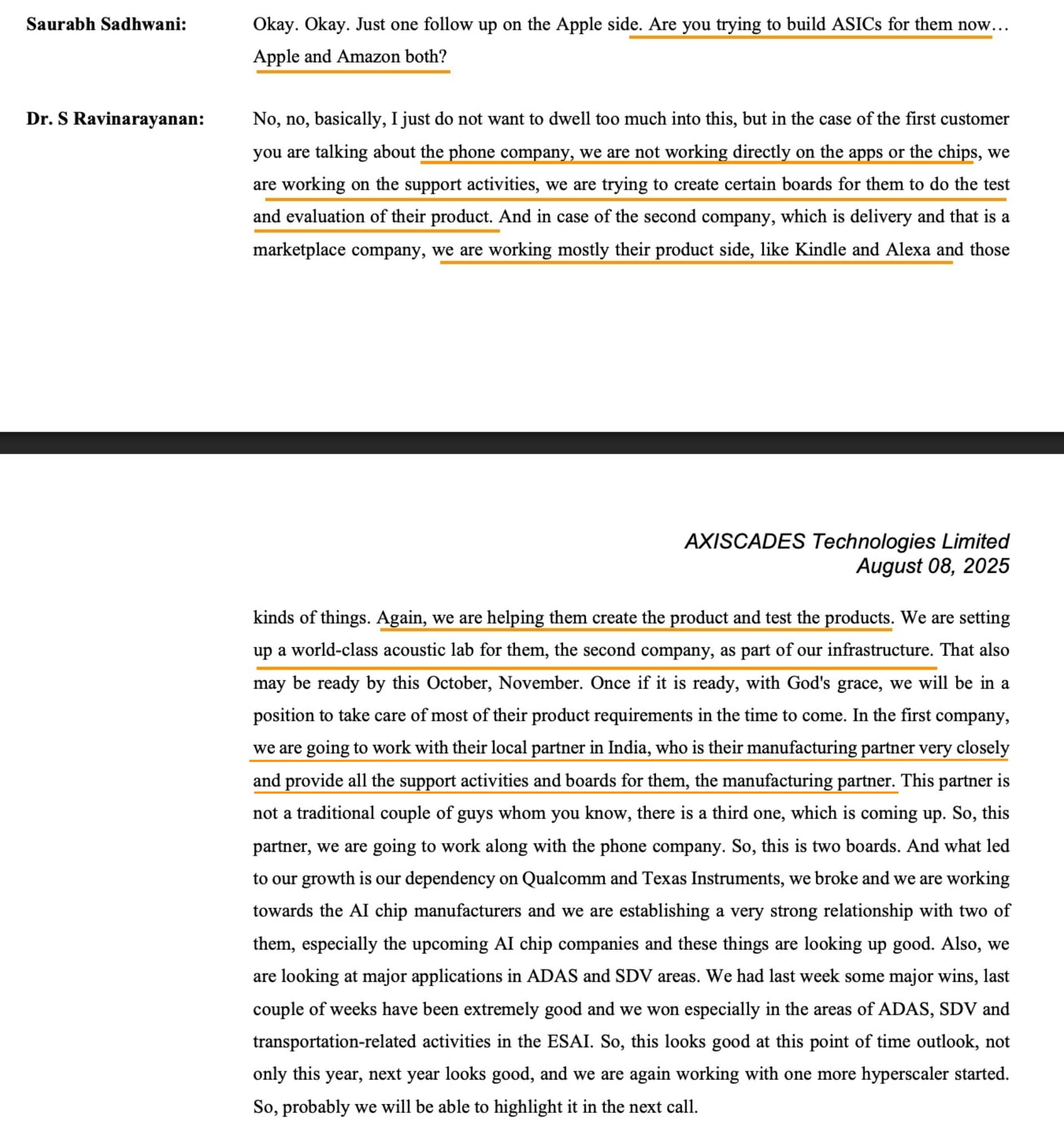

Though value-wise this order is small, I think it is an important one due to the clients likely being Amazon and Apple. Similar stuff was mentioned in last call.

The product most likely is Amazon Echo (referred to as Alexa here) and Mistral might be working with Foxconn (who seems to be the contract manufacturer for Echo).

With Apple, they seem to be working with Pegatron/Wistron (who are scaling up production now in India, which fits their description). Since the line of work is Testing equipment for production line - there’s a pretty large scope here for more work since this will scale with production lines. Also testing equipment in general makes up 2/3rd of the production for Apple (something i noticed in “Apple in China” book) - which is what excites me since cracking this relationship and way of working (with Apple/Amazon and their contract manufacturers) opens the gates for more such work.

Disc: Invested. No recent transactions

71 Likes

This MRFA tender has a long history from 2007 (MMRCA then). There were rumours that this would be a G2G deal over the last few months and looks like it has now come to fruition. It could be a positive for Axiscades if there is offset business to be had from this deal - like the 36 Rafale-M deal. If they manage, the quantum could be higher as well as this is for 114 planes and deal size itself is near 2 lakh Crore compared to Rafale-m’s 63k Cr size.

31 Likes

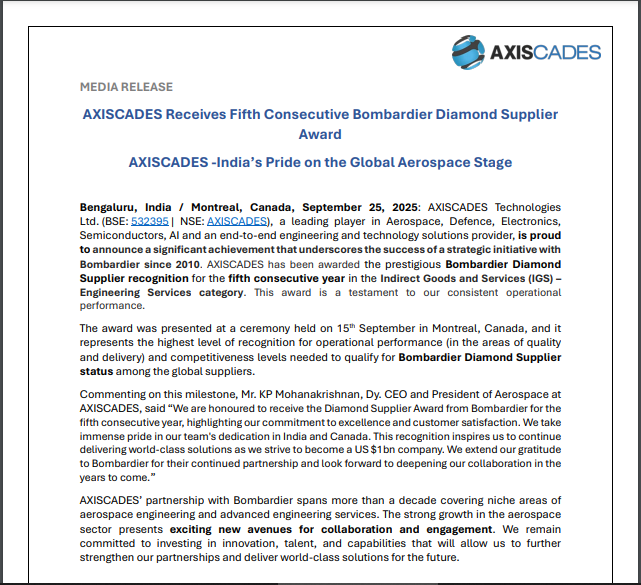

This should be good for Axiscades.

6 Likes

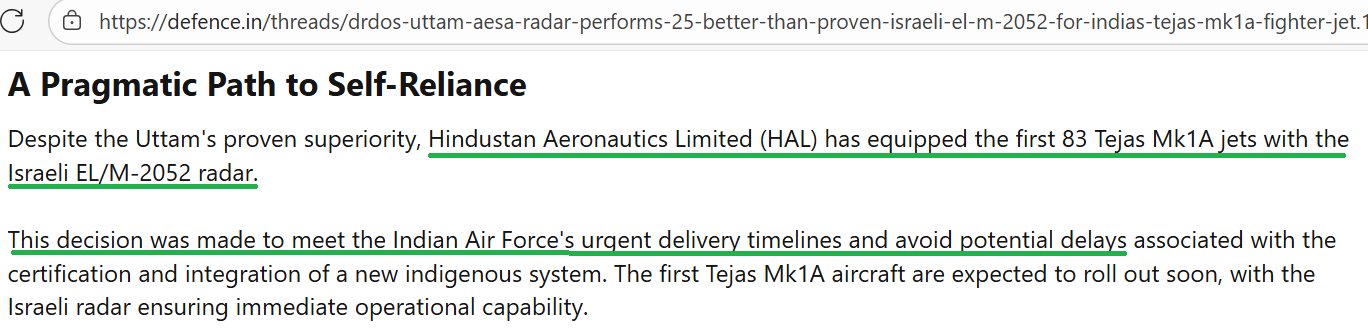

- It seems the speculation that all 83 aircrafts are to be fitted with Israeli EL/M-2052 is correct. This means the management is possibly referring to batch 2 of 97 Tejas when they say they will share good news in Q2 call.

- This article also says that the Uttam AESA is intended to be used in Tejas MK2 and AMCA as it is nearing the trails and certification (though i think it could take a few more years). Does anyone have any idea how / if Axiscades is involved in this Uttam AESA development? Sorry if this is already covered in the thready and if I have missed it.

2 Likes

First order for ‘Man Portable Counter Drone System’. Sound very interesting! I wonder how many more to come..

af90452f-d9db-4424-9587-3cb4cd9fc1de.pdf

"… its wholly owned subsidiary AXISCADES Aerospace & Technologies Private Limited has won a **prestigious order from the Indian Army to supply *Man Portable Counter Drone Systems (MPCDS).

This is among the first man-portable counter-drone order placed after Operation Sindhoor under emergency procurement, making it a major milestone for AXISCADES. The new system can detect drones up to 5 km away and block their signals across a wide frequency range, ensuring soldiers on the ground have reliable protection from hostile unmanned aerial threats…"

19 Likes

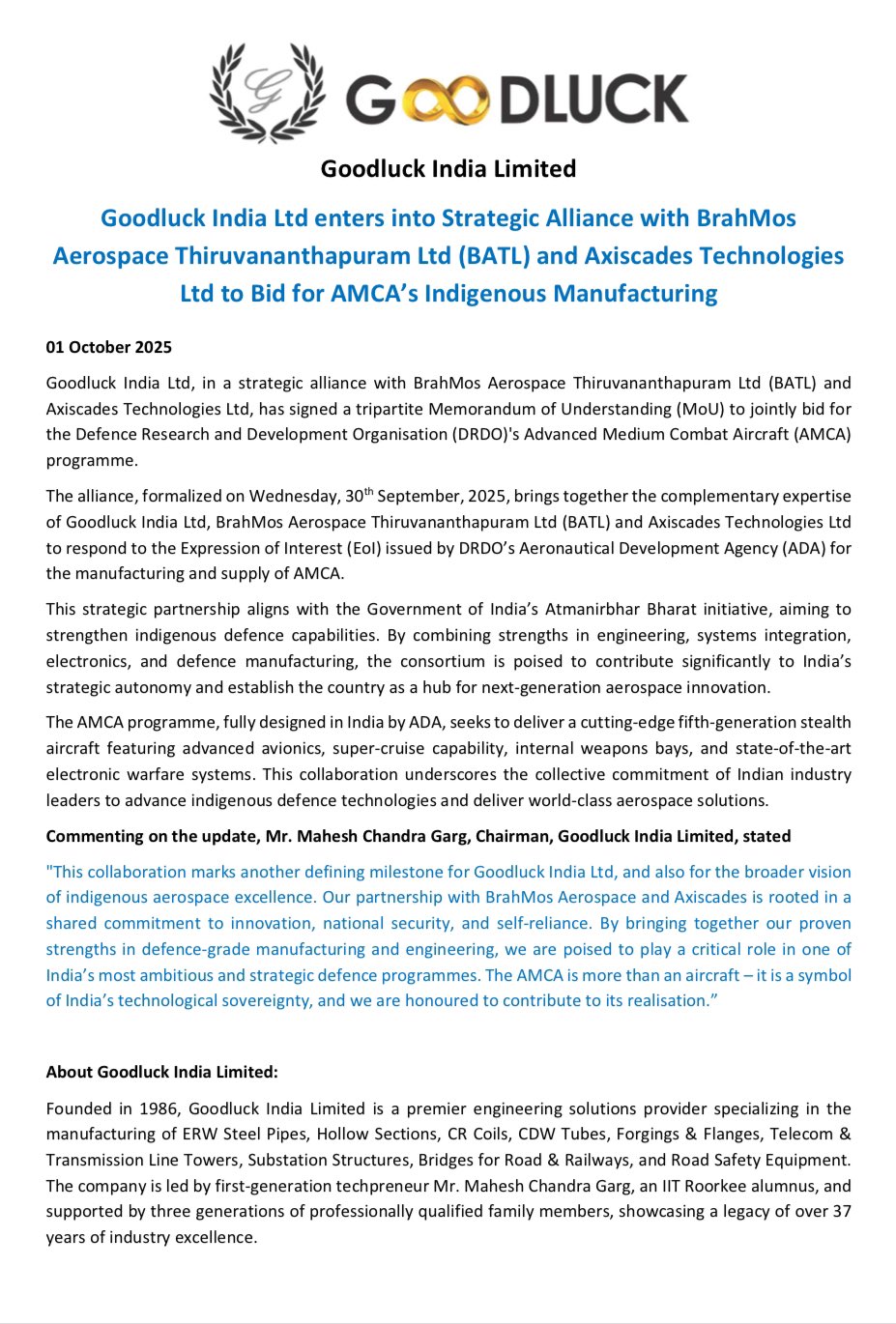

BrahMos Aerospace Thiruvananthapuram Ltd (BATL) and Axiscades Technologies Ltd along with Goodluck India Ltd enters into Strategic Alliance and submitted the Bid for AMCA’s FSED.

4 Likes

Solid results

5 Likes

Q2FY26 Concall Notes

- Revenue 13% YOY, PAT 84% YOY.

- Core business (Aerospace, defence and ESAI) contributed to 75% of H1 revenue with an EBITDA margin of 19%.

- Defence revenue growth of 37% YOY & 31% in H1.

- Defence margin at 22%.

- Not expecting defence margins to increase further as the segment is getting competitive.

- Aerospace revenue growth of 16% YOY and 12% in H1.

- Lower margins due to summer break in Europe

- Margin recovery in Q3.

- Expecting margin to stabilize around 18.5%.

- Slowdown in ESAI because we are transitioning to manufacturing.

- Till now we were only doing the design and giving it to 3rd parties for manufacturing.

- Aeroland facility will cater to manufacturing and is almost ready. Equipment to come in a month.

- Working with two hyperscalers

- Building an acoustic lab for one.

- Building a flex board facility for another one.

- Both facilities will be ready by March, 2026.

- No improvement in growth in ESAI in H2.

- Hyperscaler-1 will have exponential growth in FY27.

- From $2 million to $6 - $7 million in FY27.

- Hyperscaler-2 we are doing $0.5 - $1 million which will double in FY27.

- EBITDA Margins 15.7% vs 12.6% YOY. Q1 was 14%.

- Power930 initiative

- Revenue target of INR 9000 Cr by 2030

- YOY growth target of 40% in core business for FY26 & FY27

- YOY growth target of 70% in core business for FY28 to FY30.

- On track to achieve 45% growth in revenue & EBITDA in core business in FY26.

- Forecast visibility to achieve similar numbers for FY27.

- Transitioning from services to solutions.

- FY26’s goal is to improve per capita EBITDA by 30%.

- Capex

- Total Capex of INR ~1500 Cr over 3 years.

- Phase 1: ~150 Cr; Phase 2: ~450 Cr; Phase 3: ~900 Cr.

- Investments will be funded by internal accruals, strategic investments by partners and bridge funding by the bank.

- Net worth of INR 700 Cr and net debt of INR 50 Cr

- Plan to divest non profitable assets to generate cash

- Devanahalli Atmanirbhar Complex (3.12M sq ft)

- For defence & aerospace manufacturing

- Large scale system integration

- Secure build-to-suit zones for global OEM partners.

- Backbone facility for future export orders.

- Phase 1 is expected to be operational by FY27 (September)

- Radars, antennas, assembly and support systems for Indian defence and INDRA.

- Aeroland facility, Devanhalli (160K sq ft) [Partially operational]

- EMS for missiles, drones & radars.

- MBDA global competency centre

- Mistral HQ relocation

- Unmanned Warfare Facility [Expansion]

- Drones, Counter drone systems, UAVs, MPCDS.

- Avionics, Telemetry and Electronic warfare systems.

- Missile Atmanirbhar Complex

- Dedicated missile manufacturing hub for next gen missile systems

- Recently sanctioned. Construction starting with plans to go operational by FY27 - FY28.

- Full production capacity post FY28.

- Average tax rate for FY26 should not be more than 25% - 26%.

- Very few companies are working on laser based hard kill options and we are in the forefront.

- Emergency Procurement

- First to receive orders on MPCDS and work on delivery is going on. Expect to receive further orders.

- Plan to be in the top three players in man-portable, vehicle-mounted and hand-held counter drone systems. Capture 20 - 30% of the market.

- Developing ESA based seeker for BrahMos (2 companies are developing it).

- Hoping for a successful trial before March, 2026.

- Seeker is 30% of the cost of BrahMos missile.

- Developing Test benches for MBDA and will be exporting globally.

- Plan to build 10 test benches per year.

- Will be completing 3 test benches by FY26.

- Developing QRSAM (Quick Reaction Surface to Air Missile) systems.

- Expecting 7 systems in the next 2 months which will contribute to revenue from FY27.

- Hopeful of being a net exporter in defence in 2 to 3 years from now.

- Mistral (EMS facility) expected to go live by March, 2026.

- Expected revenue of INR 66 - 83 Cr in FY27.

Disclaimer: Invested & Biased.

15 Likes

Axiscades good one

-Defence now contributes ~40% of revenue but ~65% of segment profits.

- Programs listed include LCA Mk1A, BrahMos, submarines, counter-drone

- 18.3% margin for them : highest ever

- Revenue +25% : EBITDA +55% :PAT +87% Oper leverage phase

- Revenue per employee up 29% YoY (saw this in ppt) - Very nice metric to see :)

- RPE growth >20% is usually a business model inflection

- USD 300 mn international pipeline

“This amount pertains exclusively to new customers anticipated to close in Q4 FY26 and Q1 FY27

- Bas legacy drag is left which they are pruning.

Last results had some angle around either Alexa or google Home/nest. So US opening up kinda does help (yet to be seen)

14 Likes

Disc - I have exited from Axiscades in the last 30 days.

The reason for selling is twofold -

a) I am in need of some funds

b) I feel broader markets valuations have corrected and there can be better risk/reward opportunities.

30 Likes