MRO (Maintenance, Repair and Overhaul) Growth Opportunities in India

• MRO activities are shifting towards India and Asia. The regional shift presents a growth opportunity for Axiscades also as they are planning to establish MRO facility near Bangalore Airport.

• As per Anand Rathi report on Unimech Aerospace and Manufacturing, following are the upcoming MRO facilities in India.

9 Likes

They seem to be building a good management team. This one for instance looks like a great move.

" AXISCADES Technologies Limited (BSE: 532395 | NSE: AXISCADES), a leading end-to-end technology and engineering solutions provider, is pleased to announce the appointment of Mr. Anurag Sharma as CEO of add-solution GmbH, a Germany-based subsidiary of AXISCADES specializing in Wiring harness design & testing for aerospace, automotive and industrial sectors. add solution GmbH also leads the Specialized Drone development and Thermal management offering of AXISCADES group in Europe.

Welcoming Anurag, Alfonso Martinez, CEO and MD of AXISCADES said, “We are excited

to welcome Anurag to our leadership team. He embodies the rare blend of technical expertise and executional foresight that defines AXISCADES’ ambition. The future of engineering value is being created: at the intersection of electrification, AI-driven industrial transformation, and

semiconductor-led innovation and he brings these talents to the table.

Anurag’s track record in scaling engineering businesses gives add-solution the exact leverage

needed to dominate the software-defined era. His work in EDS and cross-border industrialization aligns with our strategy to embed deeper into European OEMs’ R&D cycles. In Europe, the sector contributes 4% to the GDP and is home to several leading premium car manufacturers, making it a highly attractive market. As part of our restructuring, AXISCADES is doubling down on aerospace, defense, and engineering services powered by Electronics, Semiconductors and Artificial Intelligence (ESAI). add-solution plays a central role in this vision, bringing software-led scale and agility to these high-priority verticals. We’re building a leadership team that doesn’t just respond to industry shifts it shapes them.”

"

8 Likes

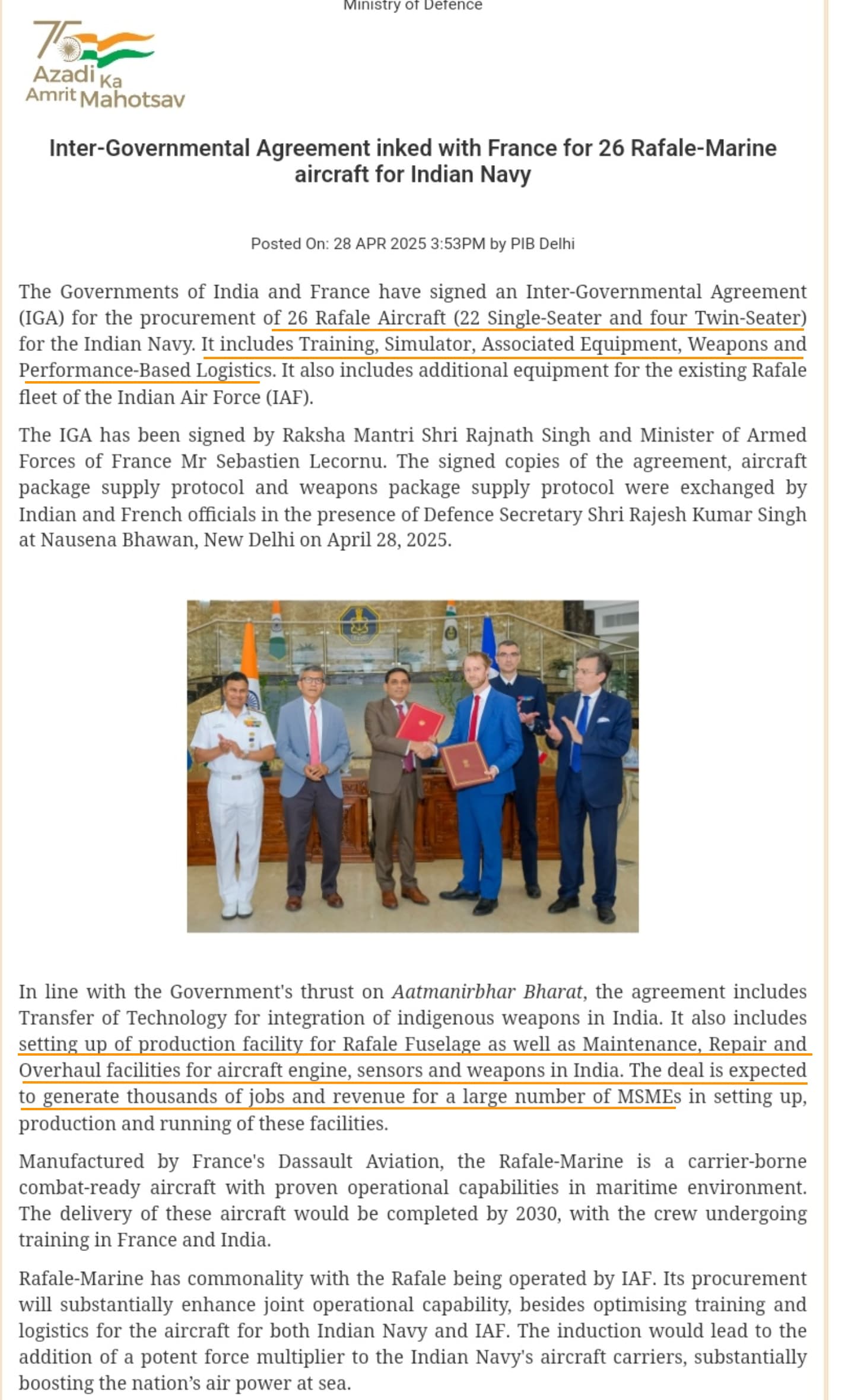

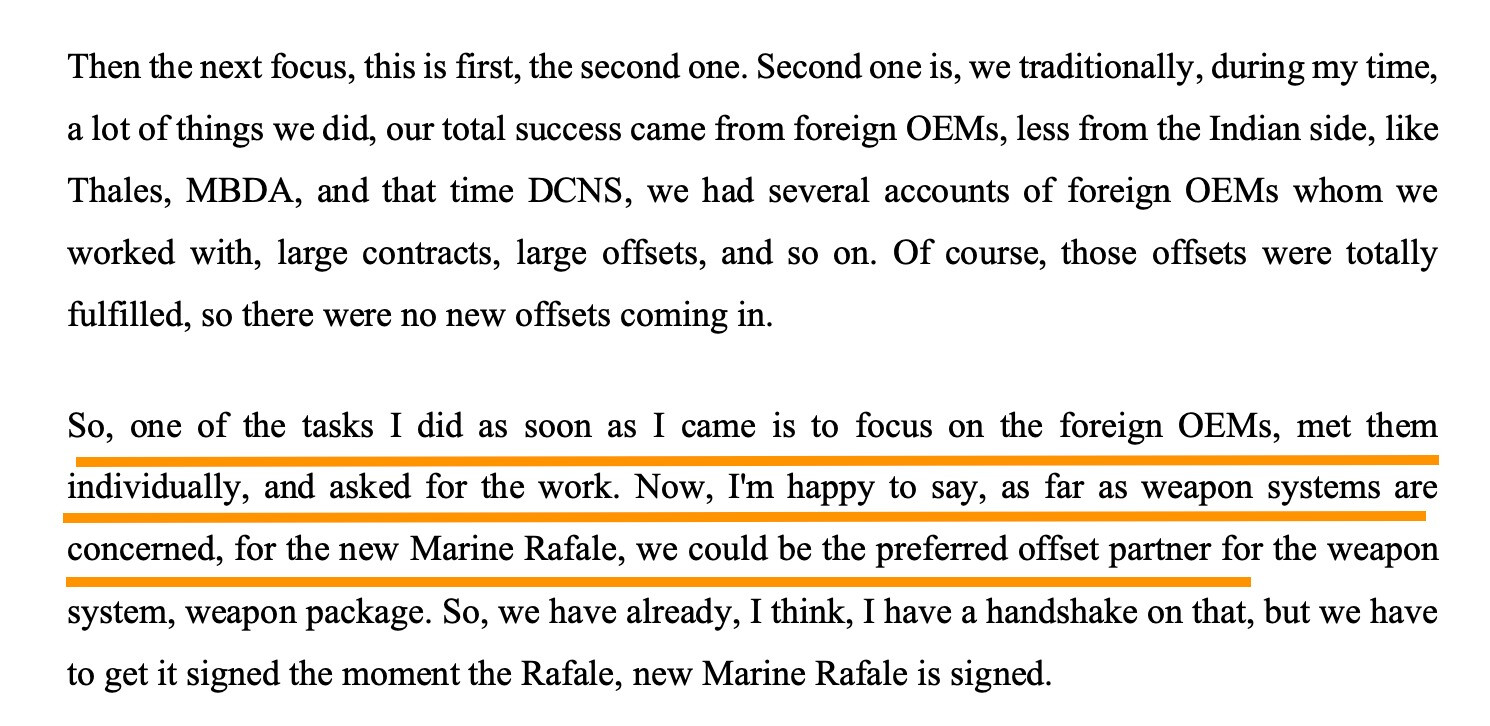

India has signed a purchase agreement for 26 marine rafale fighter aircrafts to arm INS Vikrant (to replace the aging Mig-29k). The deal value is 63k Cr.

I had come across another piece from a defence forum (can access with free signup)

which speculated a few things and was interestingly postulating Axiscades involvement in few things

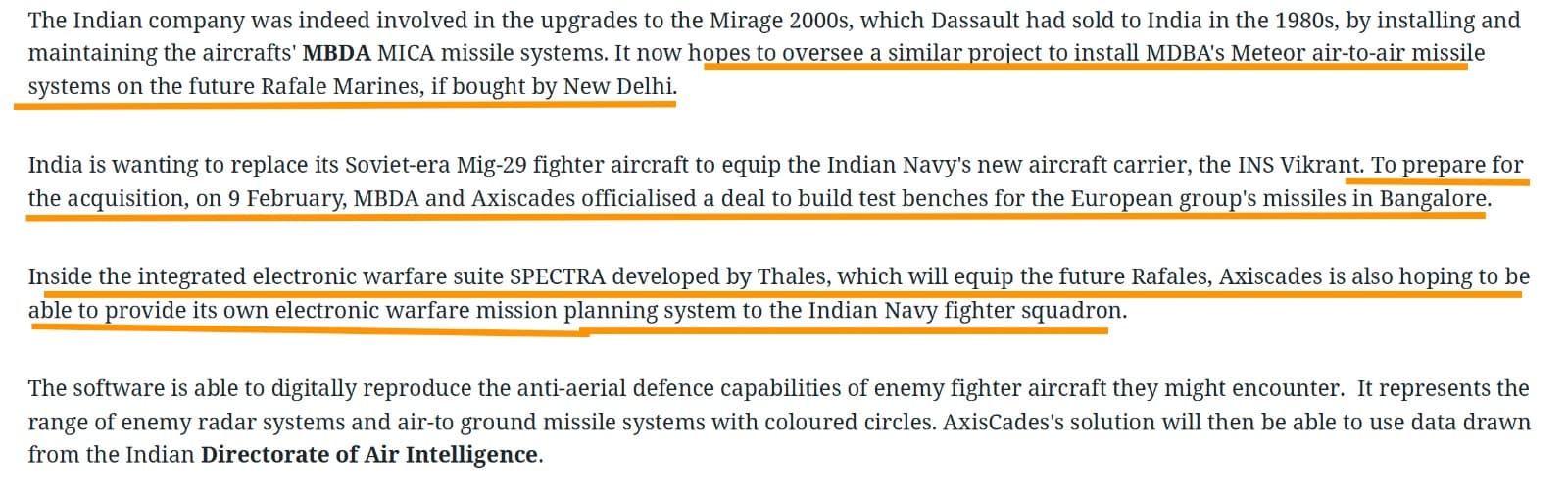

It looks like the test bench collab with mbda announced in Feb (CoE spanning 42000 sft with MBDA) is closely linked to rafale-m offset going by this piece. Axiscades could be involved in the weapons package integration as well

Not just that, according to the piece, Axiscades could be involved in avionics and electronic warfare systems as well

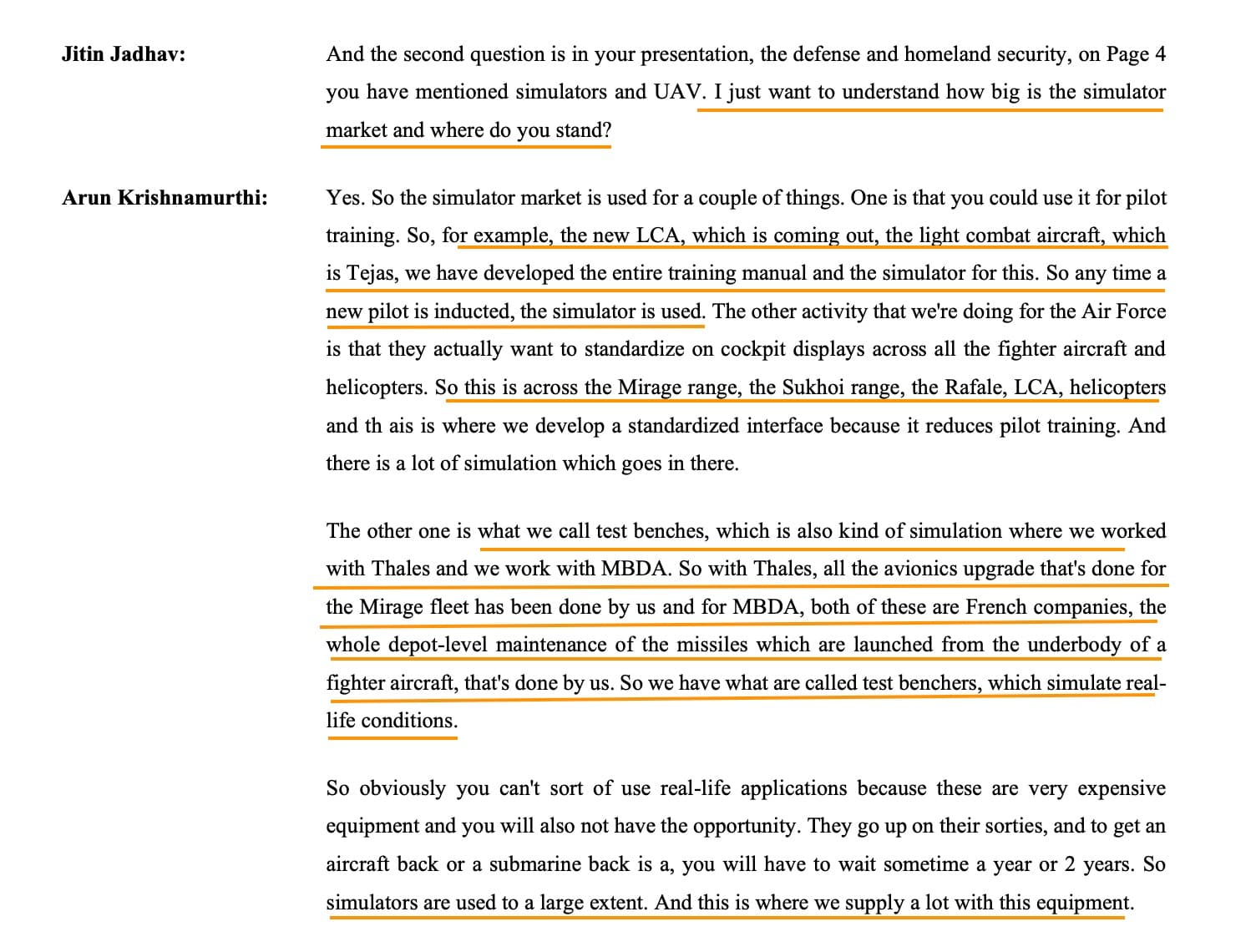

and also the flight simulators (of which, the test benches are also a part)

There were some signs of this in Dec '24 concall where SRN mentioned this

It now sort of adds up - but it is still all speculation. I have been optimistic on this and see all these as steps in the right direction. If some announcements on offsets being signed between Axiscades and Dassault/MBDA/Thales comes through, it will confirm it.

Something like this will not be totally new to Axiscades which has been involved in the past in Mirage 2000

This is from Feb '23 call where Arun speaks specifically on capabilities on simulators and also mentions having worked on avionics upgrade for Mirage fleet.

Hoping some of this translates to actual business along side the test benches which in itself could be decent size opportunity.

Disc: Invested, have some recent buys

82 Likes

Some Positives and Negatives about the Company

Integration of Mistral and ACAT – ACAT’s operations will be integrated with Mistral. ACAT will continue to exist as an entity to leverage its Defence Industrial licence and other crucial defence OEM contracts until all components of ACAT are fully integrated into Mistral. Post-restructuring, the vision for Mistral is to be a significant global player in Defence and AI powered Hypergrowth sectors, with 60% coming from Defence and 40% from Hypergrowth sectors as a result of growing demand for Mistral’s semiconductor expertise.

Anti Drone and Drone Opportunity - Company has already supplied 75 (Order of 100) Anti-drone systems and is the only company to do so. The TAM is exceeding INR 30000 Mn, here competition is limited to 3-4 players. Company is expecting another INR 1000 Mn order from the Indian Military in FY25 for the supply of these Anti drone systems.

- Heavy payload drone from Mistral, capacity to lift 30 Kgs is currently under certification, trials and demonstration to the military has been done. Indian Military uses Mules for transportation at higher altitudes and this high payload drones can substitute this. The Indian Military has an INR 7500 Mn budget per annum for transportation of these heavy items, which can completely get transferred to drones in future.

Shift from Defence Prototyping to Production – The Prototyping is a long process and generally has lower EBITDA margins sometimes even negatives. Currently company has Approved Design Wins and is Awaiting Production orders valued at ₹8 – 10 Bn, which is a high margin profile. The Défense which currently contributes around 27% of the total revenue, is projected to increase to >50% of the total revenue of FY26, with major portion coming from production.

Moving Beyond Manpower Based Revenue - The company is transitioning from a traditional, service-based, linear growth model to a non-linear, product-driven strategy, ensuring scalability and profitability. The focus is now on AI and semiconductor based electronic solutions, Unmanned Warfare systems and production-based revenues. Company has even talked about reducing the workforce (35% Workforce in Non-Core Domain).

New Strategic Investments – Company has announced 3 strategic investments in existing land parcels that they own, One in Electronic City (40K Sqft) and the other is the Aero land near Bangalore Airport (1.8 lk Sqft)

The Electronic City facility will serve as a GCC for Unmanned warfare, also include Drone/Counter Drone/Radar Hangars and is scheduled for completion in June 2025.

The Area near Bangalore airport will serve as the hub for product development and a global capability centre for ESAI. For these two, company plans to invest ₹1800 Mn in two key facilities focused on radar hangars and electronic high-end manufacturing. This new facility is more than double the size of the current operational space.

The company also has the plan to establish a DAC (Defence & Aerospace Cluster) Ecosystem to cater to foreign Aerospace and Defense OEMs, more details will be announced by Q4FY25.

Company has acquired 20 acres of land near Bangalore Airport, where it will set up a 180,000 sqft facility, expected to be operational by end of May 2025. This new facility is more than double the size of the current operational space.

Negatives

Revenue Lumpiness – The sector in which the company operates in is cyclical in nature. For example - The irregular nature of defence contracts, influenced by, lengthy procurement cycles, governmental budgets and geopolitical factors, performance in this vertical can fluctuate significantly between quarters. Thus, Défense is a long cycle business where things might not move from quarter to quarter.

The same goes for Aerospace vertical, which is influenced by the spending by large clients, geopolitical factors and is dependent on the contract renewals.

Lack of Skilled Personnel - The major MOAT in ERnD industry is specialization in particular verticals and services. This specialized expertise comes from the employee workforce in the company, Like Axiscades has almost 800 employees certified workers working for Airbus. But the lack of trained and experienced personnel can hamper the growth of the business.

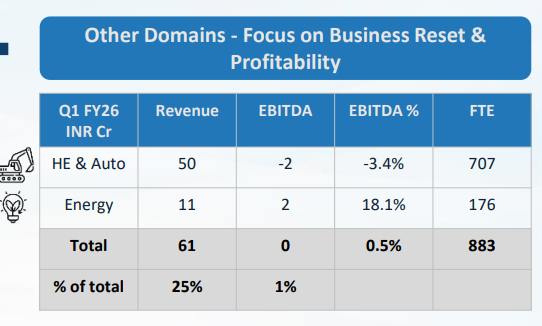

Non-Core Segments – The Non- core segments of the company especially Heavy Engineering vertical has not been growing and has also not been profitable for the company. For example, it contributes almost 28% to the revenues and only 1% to the EBITDA of the Company.

Client Concentration risk - As of FY24, Top 5 Customers contribute almost 56% revenues of the company. Aerospace vertical is heavily dependent on the Airbus, Semiconductor is dependent on Qualcomm and Texas Instruments. Also, on a consolidated basis, ~26% of ACTL’s revenues in FY23 were from its top two clients (35% in FY22)

Over-Diversification – The company has 5 business verticals – Aerospace, Defense, Semiconductor, HE and Energy and Automobile, which would lead to not focusing on the segments that are actually growing and are profitable.

Politically Connected Promoter - Jupiter Capital Pvt Ltd Holds ~60% and is headed by Rajeev Chandrasekhar who is currently Union Minister of State for Electronics and Information Technology. He is an Indian politician and entrepreneur, technocrat and a Member of Parliament in the upper house (Rajya Sabha) from Bhartiya Janata Party (BJP) representing Karnataka.

The promoters have pledged 21% of its Holding as of March 24 as compared to 68% in March 2021.

Disclosure - Not Invested, But Tracking and Learning

35 Likes

Source: https://www.bseindia.com/xml-data/corpfiling/AttachLive/873aefd5-bab6-443a-930a-6382fe9a89cc.pdf

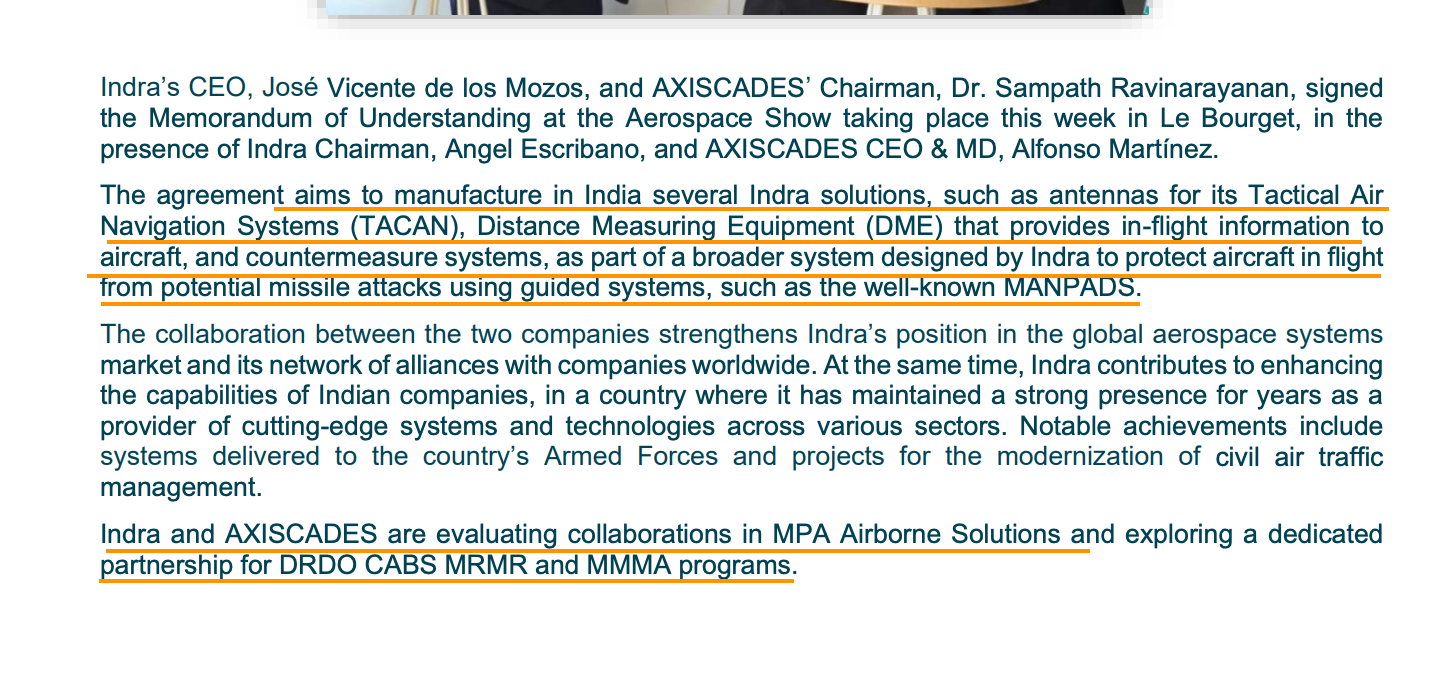

Indra appears to be a much larger company with €5b in sales. To be jointly developing products for Indian and global markets with such a large company is in itself an achievement for Mistral. There’s some indication on what the collaboration might be for

Indra seems to have won a contract with Indian Navy for upgrading radars in 23 warships to their Lanza 3D radars over the next decade. Looks like TASL is handling the tech transfer and manufacturing for this. Hoping there’s some scope for Axiscades in this as this is Mistral’s area of expertise as well.

Lot of overlap in Indra’s products’ and Mistral’s. Mistral provides long-range radars, EW suites, RWRs, IFFs etc. as well

Their products are used across NATO fleets - here’s a recent win. So if the collaboration involves making components for these systems in India to be exported to Europe and elsewhere as well, the opportunity size is quite big. Hopefully we get to hear the specifics soon.

Disc: Invested

66 Likes

This looks really interesting. Not sure but this sounds a different “Space” in which Axiscades is entering.

@phreakv6 your views on this strategic partnership?

6 Likes

Based on little I analysed, Aldoria uses powerful telescopes and radio receivers to continuously watch the sky and track all the satellites/floating junk. They know where the objects are, speed and which direction they’re going. They predict whether any of these might collide with a satellite, missile, drone etc.

Axiscades complements Aldoria. It can integrate Aldoria’s SSA data into tactical ground or airborne systems and allows this tech to be used by ISRO. Before any rocket launch, ISRO (or any space agency) needs to check, if the launch path and the initial orbit insertion route are clear of existing satellites and large space debris. Tech is helpful even after deployment of satellites.That’s about ISRO.

This can also be used in defence. Countries like China, US, Russia already have anti-satellite weapons, that are capable of shooting down satellites. Beside civilian uses satellites track missile launches, guide drones, and relay encrypted battlefield data. If space is compromised, it weakens air and missile defences on the ground.

22 Likes

Gujarat’s Minister of state for Home posted this today. Anti drone devices may have a large market in police forces too, not just the defence. Add to that the promoter being close to the ruling party. Tailwinds.

30 Likes

Axiscades gets defence orders across airborne, naval and radar-based platforms from defence labs in India, worth Rs 600 crores. Nice.

e9be9073-7350-4f06-903b-536e04d43311.pdf

More technical details in this write-up on idrw.org

AXISCADES Secures Tender for VIRUPAKSHA AESA Radar Program to Support Sukhoi-30 MKI Upgrade - Indian Defence Research Wing

19 Likes

Indian Army has signed a contract worth Rs 223.95 Crores with M/s Axiscades Aerospace and Technologies Private Limited for the procurement of 212 state-of-the-art 50 Ton Tank Transporter Trailers.

The contract was signed on August 1, 2025 under the Buy (Indian-IDDM) category, reinforcing the commitment to indigenisation in defence manufacturing.

Quick lookup on Axiscades credit report shows that Axiscades Aerospace and Technologies Private Limited is a 100% subsidiary

21 Likes

I read that and am wondering why is a company focussed on supplying defence electronics supplying tank transporter trailers? Isn’t it weird? Or am I misunderstanding?

4 Likes

Mentioned that AXISCADES Aerospace division will execute the order.

Company has legacy business called HEAVY ENGINEERING where company working for the last 35 years having Caterpillar as its largest customer. As part of org restructure not sure where they moved it but looks for me it is that segment capability as per my minimum understanding.

8 Likes

Axiscades Q1 FY 25 earning call highlights :-

-

Regarding Brahmos management said that other than the wire harness, they are in the process of a major development, which they cant disclose right now. May be in Q2 call they will be able to disclose. In my opinion it can be about AESA seeker for Brahmos NG (Next generation). Total opportunity size can be 1500 crores here (500*3) across 5 years. (Defence forces plan to aquire 100 Brahmos NG per year for the next 5 years to begin with). Recent success in Op Sindoor is one of the reason for increased attention to this system. Order can be split between Axiscades and other approved vendors.

-

Its clear that they are not involved in the development of indigenous maritime patrol radar for LUH (Light utility helicopter), in fact there is no radar in LUH in the current production version. MR radar may find place in LUH when future weaponised version of LUH come into picture.

-

Question on Kusha needs to be asked again either in AGM or Q2 call, it appears that even management has not much of idea regarding Kusha components. Good thing is that they said that they are trying to develop missile components for Kusha excluding the warhead. Basically rocket motors, on board computer and the Seeker. Kusha total missiles production will run into 1000s because it has 03 different type of missiles with different ranges for different type of targets (M1, M2, M3). If they are able to extract 5 crores per missile than it will really be a huge opportunity for them. Currently they got development/production order for 75 long range battle management radar for this system.

-

Tejas per aircraft content is 12-13 crores now (against earlier 7-8 crores). Further trials and approval process are going on, which are likely to add another 2 crores. They are into EW, ERP of radar, Mission computer and smart multi function display. It means 3 years down the line only Tejas revenue will be (24*14=336) crores per year. One ofvthe analyst in the call even asked that HAL has ordered Israeli Elta 2052 AESA radars for the entire current batch of LCA Mk1A. They replied by saying that they will share a very good news in Q2 call. Most likely next batch of order for 97 Tejas Mk1A will get finalised soon and this batch will be fitted with indigenous radar as well as indigenous EW suite. Government is very serious about increasing the domestic content in Tejas program in phased manner.

-

New programmes with MBDA (test benches) and Indra (TACAN antenna to start with) are progressing well.

-

Torpedo homing seeker for Indian Navy opportunity is about 30 crores per year for next 5 years (20*1.5).

-

Defence Ministry has approved new military acquisitions worth 67000 crores recently. Among that order Axiscades is present in Brahmos and Mountain radars.

-

Promoter is politically exposed person, thatswhy due to pressure from foreign firms, promoter is reducing stakes. Promoter holding will be reduced below 50% in next few months. Dilution through fund raise will also achive the same results but they dont want to dilute at these valuations. It is good for minority shareholders and it also means that management believes that fair valuation is higher than the current price.

-

Total capex on new Bangalore facility will be 1500 crores in phased manner. No dilution or new debt for this year. They will decide about it later on.

-

There was no discussion on projects like Su-30 upgrade, Netra, Scorpene class Submarines, C-295 Awacs, MRO and marine Rafale offset programmes in the call. However, these projects are also very important for the future cashflows of Axiscades.

-

As per management they will be able to grow 40-45% in core business segment per year for next 2 years. Thereafter 70% growth per year for next 3 years once thier Bangalore capex goes live progressively in phased manner.

Disclosure: Most of the content of this post is from the call, however for few of the things i have tried to connect the dots out of my domain experience and some aquired data from previous calls and by visiting thier exhibition during Aero India 2025. Invested.

51 Likes

Thank you for the insightful update. Did they talk about any plans for tapering down/selling the HE & Auto business line which is a drain on their profitability? I don’t remember if they had touched upon this in earlier calls?

8 Likes

Interesting development. Alfonso Fernandez is now Head of International Business and Dr Sampath Ravinarayan is redesignated as ‘Chairman and Managing Director’**.

Tbh, it did feel odd that though Mr Fernandez was the CEO, on the concalls he would be restricted to just a short couple of lines and Dr Sampath would do all the talking. I read this as a redesignation in line with the actual situation, perhaps?

4 Likes

Nice!

AXISCADES Secures Strategic Order for Electronic Control Units in Su-30 “Super-30” Upgrade Program

AXISCADES Technologies Limited (BSE: 532395 | NSE: AXISCADES), a chip to product company and a pioneer in Defence, Electronics, Semiconductor and Artificial Intelligence (ESAI) applications, today announced that its subsidiary Mistral Solutions has been awarded a major order for the supply of Electronic Control Units (ECUs) for the Su-30MKI “Super-30” modernization program.

Mistral Solutions, a subsidiary of AXISCADES has received the development contract from

CASDIC (Combat Aircraft System Development and Integration Centre) for the development

of 10 nos. of Electronic Control Unit of cooling system for Su-30 MKI upgrade. **The said order **

**is awarded for prototype development and will be followed by a forecast production order for **

an estimate of 600 numbers, with value of Rs. 150 crores over a period of 5 years.

e6eee6ff-d88b-4722-96b1-fcb9c35d7714.pdf

It’s raining orders! This time for designing aircraft interiors - perhaps a new line of business? This must be for Airbus with whom they said they have very good business relations.

AXISCADES Accelerates Aerospace Growth Strategy with Entry into Aircraft Cabin Interiors

Bengaluru, India – 01st September, 2025:

AXISCADES Technologies Limited (BSE: 532395 | NSE: AXISCADES), a leading technology solutions and products company addressing Aerospace and Defence, today announced two new wins in aircraft cabin interiors design, development, and retrofit solutions.

The pilot orders valuing USD 1.2 million have been awarded by two global leaders – a global

aerospace OEM and a world-renowned aircraft cabin interior company based out in Europe

and USA.

7 Likes

Good flow of orders but its concerning that the management is continuously selling their stake ( Jupiter Capital) . Seems unusual

Any insights on this would be appreciated

1 Like

The only insight I have is what the management had shared earlier - that they requested the PEP (Politically Exposed Person - Rajeev Chandrasekhar’s fund) to reduce their holding. How far it is true - up to you to judge.

2 Likes