Many things have happened since the I started this thread and some of my thoughts as things stand today are written below.

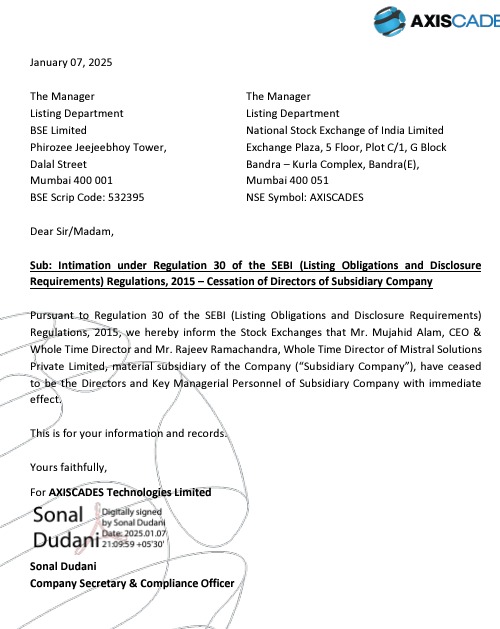

Resignation of Arun and Mistral Top Team (Muju, Rajiv etc.)

There were two ways the company could have gone when this thread was started - it could have become a decent engineering services company (like Cyient, Tata Elxsi etc.) or it could have gone on to become aerospace & defense technology company. My own preference has always been for the latter - as technology business > manpower business in my view and there is a large opportunity available in aerospace/defense over next several years.

I think Arun wanted to steer the company in the engineering services side given his background and hence he acquired Add Solutions, Epcogen and hired people to seed digital capabilities. I think the owner and board felt this was not the direction they wanted to take given the opportunity in aerospace & defense and hence this reset was needed.

I would still credit Arun for completing the Mistral acquisition through disputes, deleveraging balance sheet through fund raise, bringing relative stability in management and relatively improved communication.

Coming to resignation of Mistral Top team, there are two aspects that I wanted to understand -

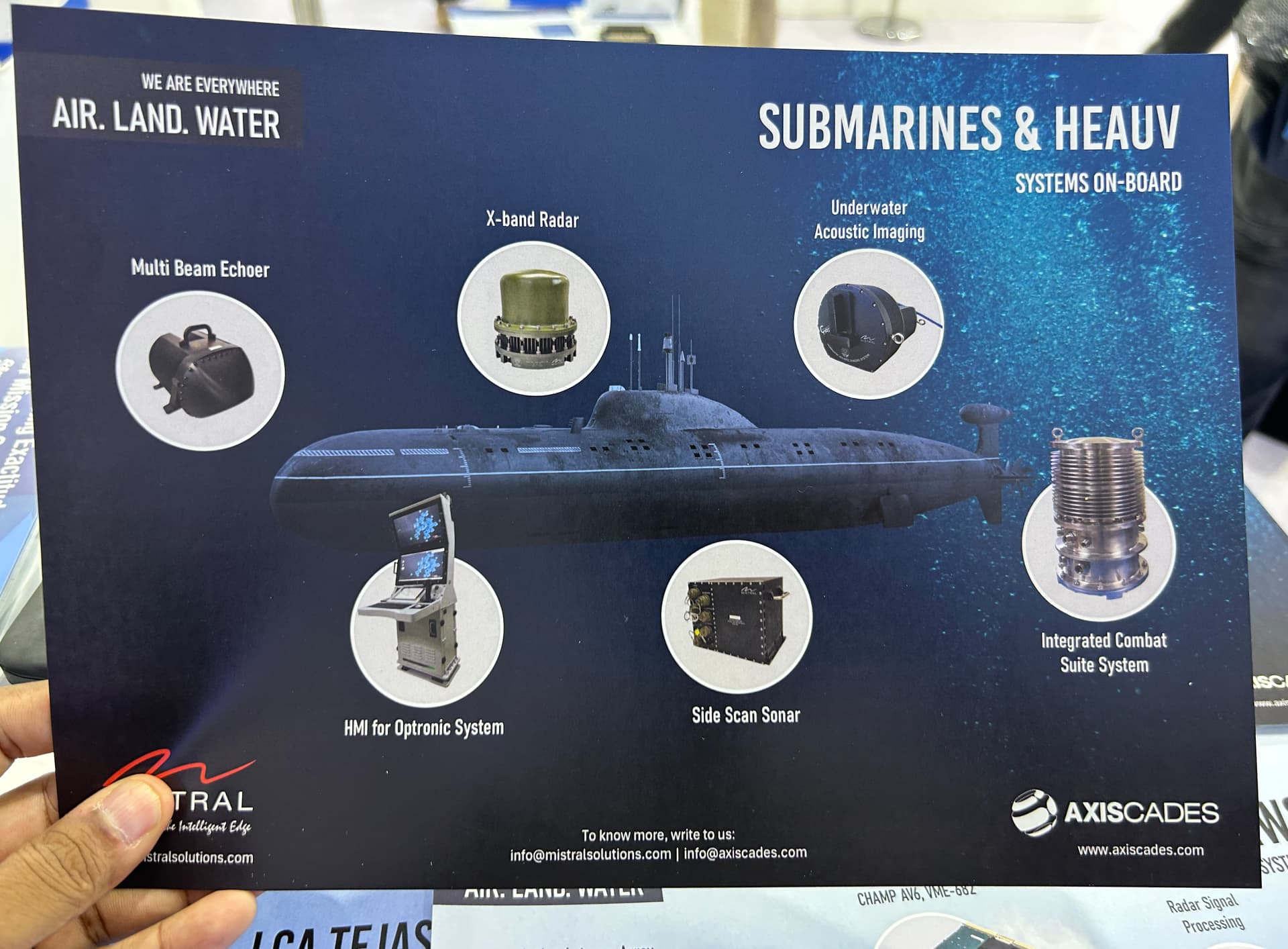

First was that whether this will impact relationship with DRDO/DPSU (BEL, HAL, BDL etc.) and various Shipyards. Over time with my interactions with management, I became convinced that the relationship has remained and not deteriorated. The next level leadership in Mistral has taken over this networking part within Indian Defense establishment.

The second aspect is usually the management in acquired company leaves or is asked to resign as new owner wants to imprint their vision on the company. This is fair in business. The owner/board wanted more aggressive pursuit of the opportunities in aerospace and defense, and they felt that there needs to be a shakeout in the leadership. I also got convinced, over time by talking to various stakeholders, that resignations were not due to any financial issues and more of an issue where board wanted more aggressive approach.

Now coming to new management and new approach, one thing that has definitely changed is that communication has improved and now analyst community is asking more questions on aerospace and defense and program specific details. In the equity markets, Axiscades is now at least considered part of aerospace & defense industry and hopefully we will get more coverage like other listed players in defense.

The second aspect is that the new management has set aggressive growth target of 1bn$ sales in 5-6 years and entire organization is asked to align with this. There will always be an element overselling that promoters/managements tend to do. We, as investors, need to validate management talk through scuttlebutt, talking to industry players, cross questioning and being generally conservative on timelines or revenue/margin guidance that management gives. I would be happy if the company achieves 500mn$ sales in 5-6 years.

So, I am happy that second and third level of management is at least thinking of faster growth, pursuing opportunities etc.

Operational Aspects

Now coming to some operational aspects -

LCA Tejas Mk1A Orders

GE recently delivered first engine needed for LCA Mk1A. Hopefully this supply chain will get revived and hopefully there will be no more delays.

Secondly, with events like - IAF chief’s public bashing, parliamentary panel’s comments on HAL’s inefficiencies and defense minister’s show of solidarity with LCA/HAL at Aero India – I feel that HAL is under tremendous pressure to deliver this program.

I feel orders for electronics components for the last 33 LCA from first order of 83 and second order of 97 (which have indigenous radars and EW components) are around the corner and are probably delinked from engine delivery supply. If one reads through conference call transcripts of industry players (Astra Micro, BEL, Axiscades, Data Pattern etc.) - it becomes evident that HAL would like to get everything ready and then wait for engines to show up.

My confidence on industry getting LCA orders in FY26 has gone up quite significantly. We need to observe how the execution of these orders is partitioned over the years. But if GE ramps up supply, then FY26 can see supply of components for 5-10 planes and FY27 onwards this number ramping to 15-20.

Su-30 Orders

What I understand through various conversations at Industry events is that final configuration of Su-30 is finalized, and vendors are getting development/prototype orders for various electronics components.

Su-30 is lower risk than LCA because there is no engine upgrade involved. My sense is that starting H1 FY27, we will start seeing some production orders for Su-30 and execution picking up space in FY28.

One thing that has become clear is that Su-30 tenders will have more competition from newer players as well existing players expanding into new products. So, there are chances that production orders might be split across multiple vendors and also chances at the other end that some of the players might increase their wallet share vs LCA.

I feel mixed about Mistral’s chances in increasing contribution in SU-30 - so we have to keep tracking these things as they evolve.

But Su-30 program is moving ahead from discussion to prototyping and hopefully it is on time for production starting FY28.

Other Orders at Mistral

Some of the areas where order visibility has increased are -

- BEL has received order for Ashwini LLTR radar. I think Mistral should get order for radar processor in next few months.

The X-Factors

These are the orders or areas where company is pursuing opportunities after change in management.

-

The first clear area where there seems to be progress is offset contract business. In recently concluded Arihant Bharat Conference - company said that they are negotiating a deal which will result in center of excellence (CoE) in missile testing for MBDA. The cost of one missile test bench is 4-5mn$. They are also hoping that the client will fund part of the capex. Let us see how this deal evolves.

-

The other thing company confirmed is that - they are thinking seriously about MRO business and thinking of establishing MRO facility near Bangalore airport. MRO business, if successful, can contribute 100cr to revenue as per management in 2 years time.

Both of these are fluid and negotiations/outcome can take a long time to materialize. But these are two programs where the probability of deal has increased.

There are several other programs which are slightly longer term and visibility will improve in the coming year (Netra AEW&C order, QRSAM order, HEAUV order etc.). We will talk about these as and when these programs make progress.

Finally, in Arihant Bharat Conference, participants managed to get some projections from management which are listed below -

- Mistral Revenue

160-170cr production revenue + 80-100cr prototyping revenue - FY25

250cr production revenue + 80-100cr prototyping revenue - FY26

- ACAT Revenue

50-60cr business in FY25, 120cr type of business in FY26 (offset contract, counter drone systems)

- Aerospace business - base business company expects growth of 20% (Excluding MRO etc.). One indicator of growth here is Airbus ramping up production run rate of planes.

- Heavy Engineering

This business has ~120cr revenue in FY24 and had -ve EBITDA margin. The company is making efforts to bring this business to 8-10% margin. Conservatively, I expect this business to have 8% margin on run rate basis from Q3 FY26 onwards.

In summary, the order cycle for Mistral seems to be improving, Non-Mistral (Direct to Defense) business has some deals under negotiations and overall probability of increased profitability in non-core areas has gone up.

Disc - Axiscades is the largest holding for me, no buy/sell transactions for more than 30 days. I am positively biased due to my holding. The stock has doubled from the lows and valuations are on the higher side. Please do your own due diligence. This is not a buy/sell advice, I am not a SEBI registered advisor.

")