Is anyone still tracking this co.? As per latest AR, the Mistral is fully in.

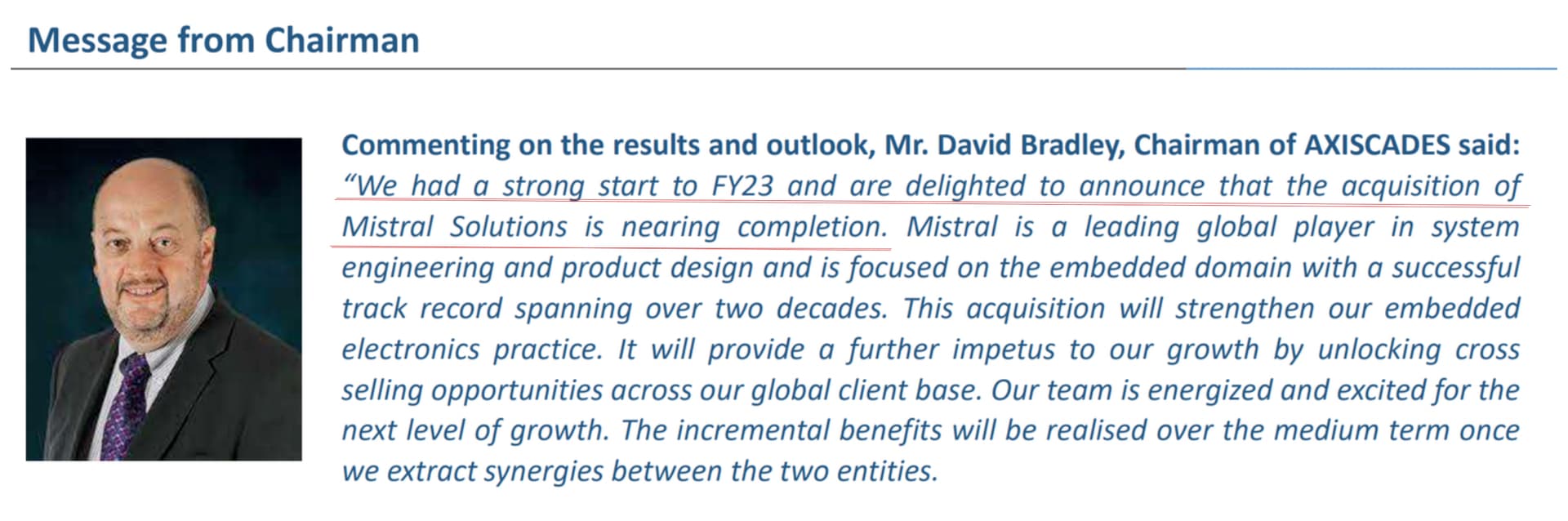

Share purchase agreement happened almost five years back. I am not really sure if the matter is still fully resolved. Chairman in Q1-23 results presentation, mentioned that the acquisition is nearing completion.

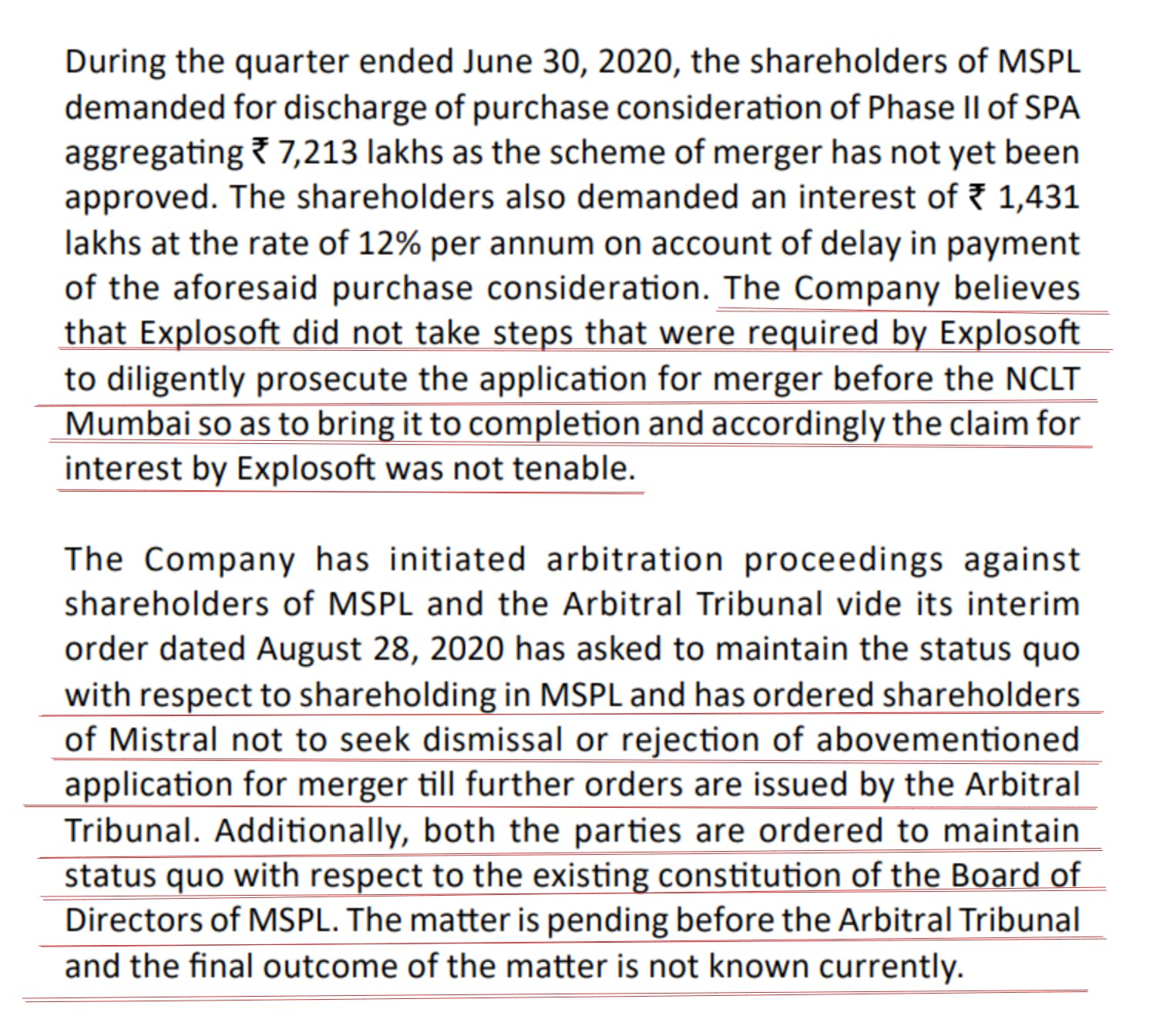

The annual report (page 27) states that the issue with Explosoft is still with Arbitral Tribunal.

Pledging of ~28 Crores in my view is mostly for phase-II of mistral acquisition. Any other reasons?

Miistral acquistion is completed

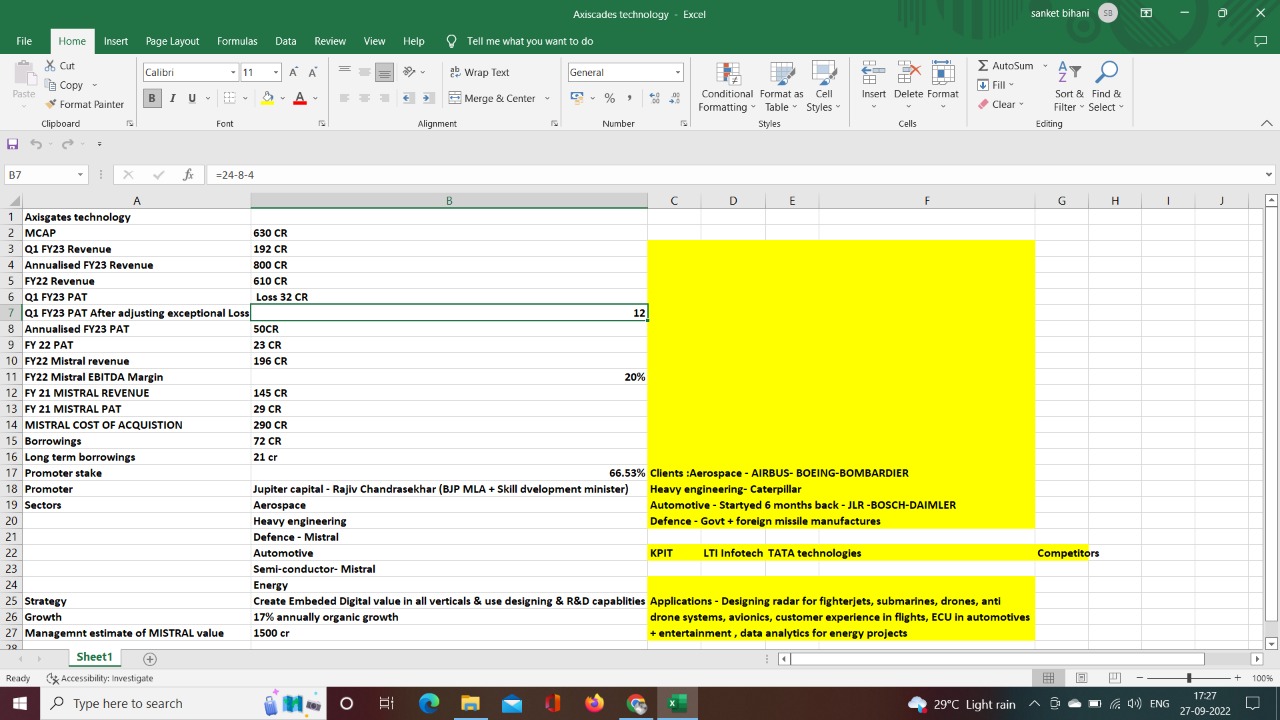

I haven’t been tracking this very closely but here is a snippet from two-month-old credit rating report.

While phase II was supposed to be funded by allocating shares to promoters of Mistal, there has been an additional charge of Rs. 44.45 crores as directed by the arbitration tribunal. I don’t see any discussions around it in the AGM transcript.

1 Like

Here are a few things that popped up on my search alerts on Axiscades.

- An article/interview from Arun K.

This is the bit I find interesting

- Mistral leadership receiving Licensing Agreement for the Transfer of Technology (LAToT) for the Ground Penetrating Radar.

I am sure Mistral is not the only one who perhaps got this in Defense Expo, held in Gandhinagar Gujarat, but important to note nonetheless.

2 Likes

This is what stands out in the Q2 23 results. Good numbers overall.

- Revenue growth of 43.4% Y-o-Y

- EBITDA Margin at 19.3% compared to 12.4% in Q1 FY23

- Acquisition of add solution, GMBH, Germany, specializing in Automotive Solutions to Global OEMs.

Notes from the Q3 FY 23 call

• Management background

o CEO Arun Krishnamurti was earlier with Tata Technologies in London (managed 200 mn dollar business engg portfolio). Prior to that had a long stint with Wipro -managed half a billion dollar portfolio in Utilities industry. Comes with a rich experience of 20 years , of working with customers closely– to win, grow & scale up business.

o CFO comes with an experience of 30+ years. Has been part of multiple business turnarounds in the past… Comes from the Tata stable, like the CEO.

• Business highlights

o 3-pronged strategy – Vertical diversification, Customer diversification (reducing client concentration) and Customer first ; focus on embedded and digital

o Highest ever quarterly revenue recorded by company in Q3 FY 23

o 15% Operating margin in Q3 FY 23 vs 12% in Q3 FY22.

o 9M EBITDA has crossed last year’s full FY EBITDA…

• Revenue contribution- 56% contribution by Axiscades parent entity, Mistral contributed 34% and 10% came from Axiscades Aerospace

• Segment wise growth

o Automotive & energy – 60% YoY growth

o Aerospace – 42% growth YoY; 13% QoQ

o Product Engg services – 29% YoY growth

o Mistral – grew by robust 68% yoy

o Heavy engineering saw a degrowth of 3% yoy

• Recently renewed contract with Airbus for the 4th time in succession. Close to 2 decades relationship with Airbus.

• Completed acquisition of Mistral.

o Value accretive business. Mistral margin is at 15.4% ; parent company is at around 13.7% … They have expertise in semi-conductors.

o Integration process is well underway & progressing very well. All 3 founders of Mistral are staying back.

o There is an exceptional item of 23.6 Cr in Q3 FY 23 owing to Mistral acquisition; No more exceptional item charge in the books going forward.

o The company has completed acquisition without diluting capital. Took on an incremental debt at higher interest rate to close the acquisition (tight timelines imposed in by the tribunal). Looking to refinance the debt at lower interest rate, by end of the year

• Lot of synergies with Mistral -

o Strong embeded electronics capabilities. Have seen a lot of clients pivoting to embedded and digital.

o All the verticals that they are currently servicing – looking to cross-sell embeded to all these clients. Since it involves rare and niche skills, rates are better and profitable will be way higher…

o Mistral – lot of capabilities in avionics – cross selling it to their existing aerospace clients. Similarly lot of capabilities in radar technology. Increasing focus on their strategic accounts, in order to grow share of the pie with strategic accounts & increase client stickiness.

• Strategy of Vertical diversification

o Earlier there were 3 verticals. Now 5 verticals… Now we have defence + 5 sectors. Whole idea is to reduce sector dependency & any one sector headwinds should not impact overall growth trajectory. Currently heavy engg is a little muted… But spread of the sectors – aerospace, automotive, etc will ensure we are on growth path…

o Customer concentration has come down –

o Top 5 customers in 9M of current FY – contributed 57% of total revenue. Last year for same period, it was 63%.

• Operating margin - Currently at 15.5% margin. Industry margin range 17 to 18%. Over next 3 years - striving for 400 – 500 basis points improvement

• Looking at internal automation very aggressively, to optimize efficiencies.

• Order book - 75 mn order book as of Dec 23. 45 mn order book would be carried forward to next FY. Healthy order pipeline of 280 mn dollars (other than Mistral). Mistral – 3000 Cr (prototypes that have been accepted; production orders may get phased out over 5-7 years; but it will all come in– long term projects)

Defence opportunities & tailwinds:

• There are 3 or 4 other companies in the space – Data patterns, Mistral, etc… Each of them has a niche. Mistral’s niche lies in radar and sonar…

• Working on laser guided drone protection system capabilities. Showcased some of these capabilities at the recent Aero show. Saw lot of interest from all the 3 streams of defence…

• GMBH acquisition called off – Upon due diligence, found that, out of 2 major contracts with VW, one of the two contracts was still not renewed. Saw a risk having to run the company without the contract being renewed. Risks associated with acquiring a company without a contract being there; Labour laws tilted towards employees, in Europe… Was therefore called off.

• Exploring a couple of other inorganic acquisition opportunities. One in energy space and other in industry 4.0 space - PLM space. In due diligence stage.

Disc: Invested

4 Likes

Order book - 75 mn order book as of Dec 23. 45 mn order book would be carried forward to next FY.

Does this mean Q4 is going to be big in terms of execution?

Can you share some insights here?

2 Likes

Looks like the Boss @ Jupiter Capital didn’t like the chairman. Today is his last day. Honestly, I never understood why he was brought in in the first place. David Bradley hardly has any digital footprint (or the company Inbis Ltd where he is CEO/MD) for normies like us to assess what value he brings.

2 Likes

Does anyone understands how this new acquisition gels with Axiscades? May be there are some parts of epcogen that are relevant but at the surface, it appears unrelated.

there is too much traction in energy segment whether it’s fossil fuel or renewable, as this co is mainly working on oil & gas and working on hydrogen & sustainable energy, the valuation is cheap & other big giants are making partnership in the same space, also they have strong foot hold in aerospace & this sector also looking for SAF & other option on sustainable energy, so getting an another business which helps their core business ( mechanical business) since inception

1 Like

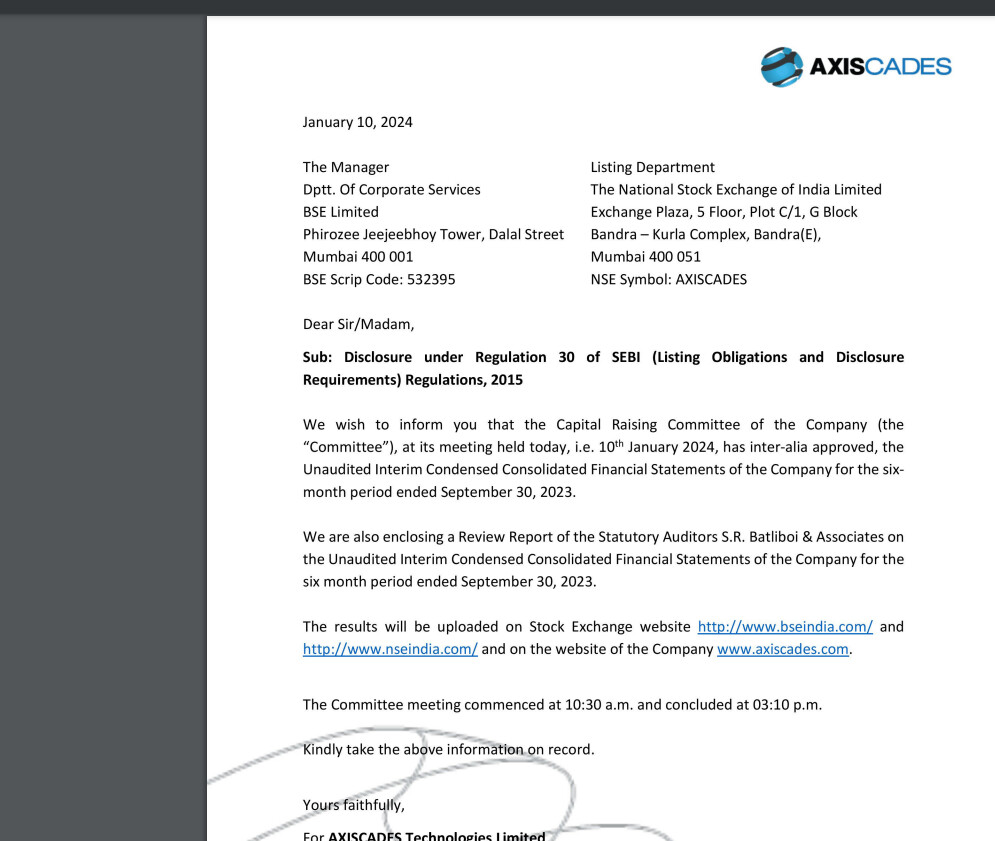

In the last concall, mgmt said they might raise money essentially QIP this year to pay off debt. I think with this they’re probably finishing required documentations that might be required to raise capital. I don’t understand what is the capital raising committee in general as well in the this context. If anybody who is from a finance background or have an understanding of these terms, please shed some light on this notification?

1 Like

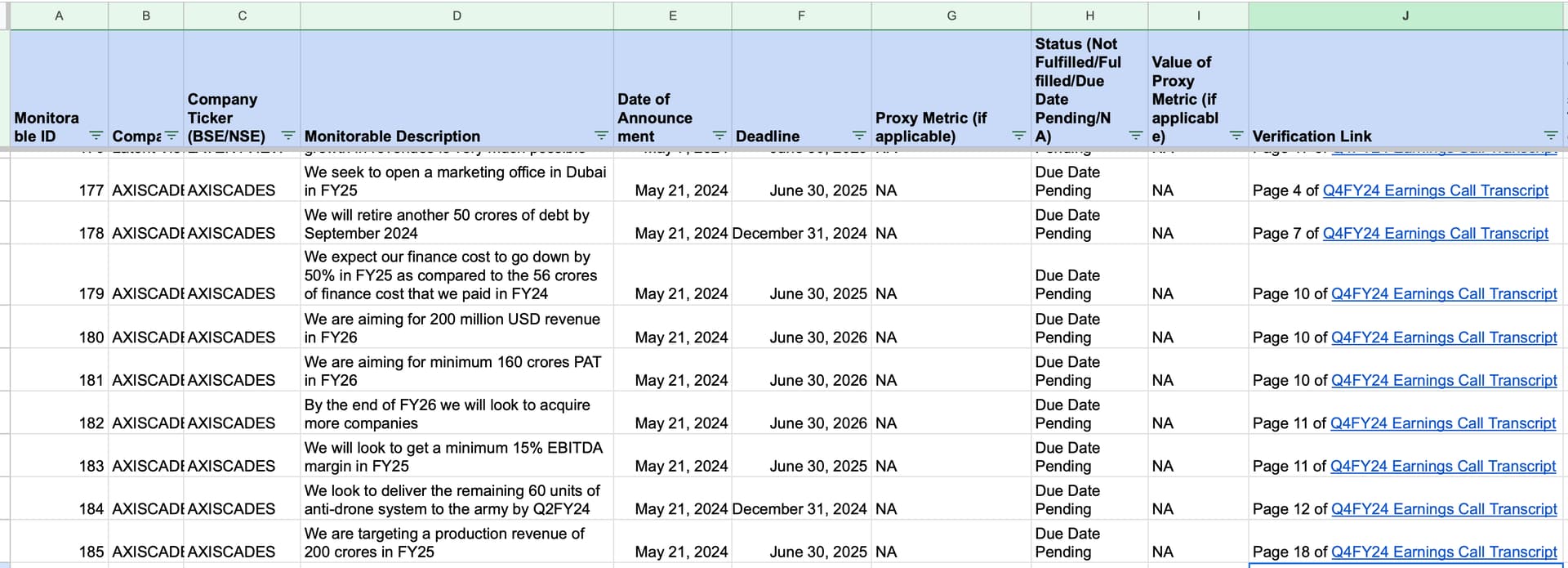

Hello,

In the below tracker, I have started tracking important company goals for AXISCADES.These goals are referred to as ‘monitorables’ in the tracker.I will update this document regularly to reflect the current status of these goals.

Here’s a snapshot of what the tracker includes:

- Company Ticker: For identifying the company

- Monitorable Description: Description of the goal or metric being tracked

- Date of Announcement: When the monitorable was announced

- Deadline: Target date for achieving the monitorable

- Status: Current progress (e.g., Not Fulfilled, Pending)

- Verification Link: A link to see where we got the information about the goal.

I hope this information makes it easier to observe how well companies are progressing towards their stated goals.

Screenshot of the tracker below:

Full tracker attached below:

Tracking Company Monitorables-9.xlsx (127.1 KB)

3 Likes