Hi Guys, have been doing research on AVG logistics and thought will share with the group. Stocks looks v cheaply priced givens strong bullish guidance by management. I have tried to keep my view balanced by also highlighting the risk factors. Any thoughts?

1. Company Overview:

AVG Logistics Limited is a leading Indian logistics company offering transportation, warehousing, and cold chain services. Founded in 2010, the company has grown rapidly and established itself as a reliable partner for numerous clients across diverse industries.

2. Management:

AVG Logistics boasts a strong and experienced management team led by:

Sanjay Gupta: Managing Director and CEO with over 20 years of experience in the logistics industry.

Asha Gupta: Whole Time Director with expertise in finance and accounting.

Vinayak Gupta: Vice President with a proven track record in operations and business development.

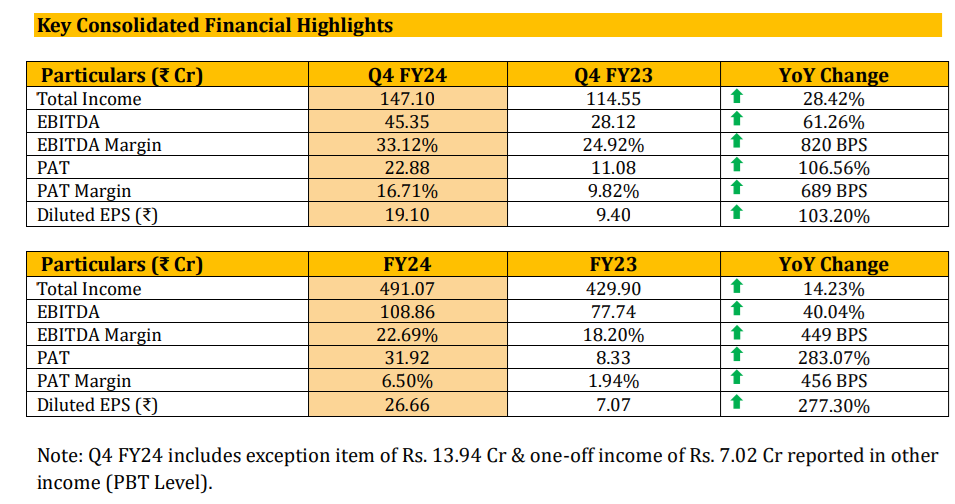

3. Financial Performance:

H2 FY24 (October 2023 - March 2024):

Revenue: INR315.70 crores (reported as of November 2023)

EBITDA Margin: 13.40% (reported as of November 2023)

PAT: INR13.40 crores (before tax)

Expected Growth:

Revenue: 65% increase from H1 FY24

EBITDA Margin: Increase to 18-22% range

PAT: Increase to INR30-35 crores

Key Drivers of H2 FY24 Performance:

Increased demand from existing and new clients across diverse industries.

Optimization of transportation routes and logistics operations.

Improved fleet utilization and cost-control measures.

Contribution from new business ventures like reefer logistics.

AVG Logistics Strengthens Cold Chain Capability by acquiring fleet of 50+ Cold Chain vehicles.

This greatly enhances AVG’s ability to service recently signed long term contract with India’s largest MNC FMCG Company both on the dry and frozen goods side. This fleet represents 20% of AVG’s current cold chain fleet strength and takes up AVG’s total cold chain fleet strength to 275+.

Prominent clients: Nestle, HUL, DS Group, Apollo Tyres, JK Tyres, ITC, Airtel, MRF, Jubilant Food, UltraTech Cement, Coca Cola and more.

Newly added clients: PepsiCo, Leap India, Colgate, BigBasket, Loreal and many other retail companies.

Fleet compromise over 3,000 vehicles which includes 550 owned vehicles allowing us to dedicate the details of the transportation effectively.

Working with OEMs to launch EV electric vehicles and LNG fleets to our existing fleet and target to add 100 vehicles till December 24.

Added 50 high quality cold chain vehicles from multinational logistics company consisting of 20% over existing cold chain fleet.

As of Sep-23 Balance Sheet, the company is having 139Cr of receivables out of which 50cr is more than 6 months. Why are the receivables so high when the company is doing business for Reputed customers like Nestle and Pepsico?

FY24 Highlights:

Company had over 467 owned vehicles in FY23 and by FY24, this increased to 574, with an addition of 107 vehicles.

The Company expands its rail network with the addition of 3 new routes, bringing the total to 8rail

routes by FY24.

The company’s debt reduced from ₹112.74 Cr to ₹88.88 Cr in FY24, reflecting effective debt

management and improved financial health.

Company has declared the dividend to its shareholders consecutively for this year also at a rate of 12% on face value as compared to 10% in previous year.

Commenting on performance, Mr. Sanjay Gupta Managing Director & CEO, said,

With substantial year-on-year growth in revenue, EBITDA, and PAT, AVG Logistics is reaffirming its

commitment to excellence.

The award of the significant Indian Railways contract is a testament to our strategic long-termvision. Recent acquisition of a fleet of high-quality cold chain vehicles further amplifies our capabilities and demonstrates our dedication to providing top-notch services to our customers.

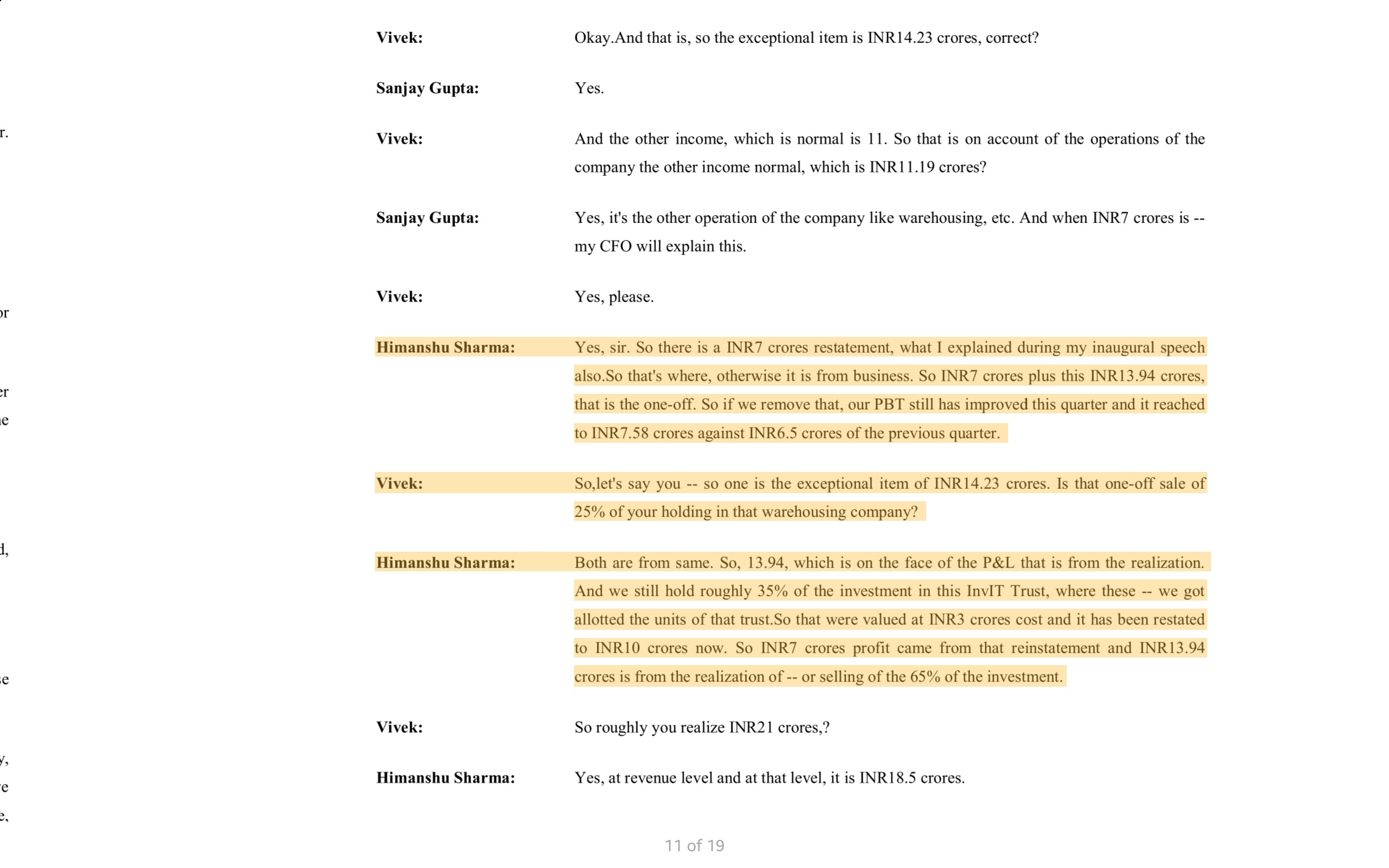

In my opinion, this is an unduly glorified press release. One should carefully read the published financial statements along with note 6 and note 9.

There are some contentious points -

In point 9 they have mentioned about “a fair value gain of Rs. 702.65 lakhs” against the allotted Invits which is being reflected in the P/L but I think that is more of an asset till not sold/encashed.

The rectification details mentioned in note 6 are resulting in a more glorified QoQ result. Just a point that one should be aware of.

The other income of 1015.77 lakhs, which includes ”the fair value gain of 702.65 lakhs" as per the press release, but yet the difference of 312.35 lakhs remains unexplained.

I am not an accounting expert but point 1 and 3 above may need further explanation.

I have not yet heard the earnings conference call, the recording and transcript of which have been published. I had infact even missed its schedule announcement. Rather when was it announced?

I hope to review that soon and find answers to my outstanding questions therein. Would appreciate if anyone knowledgeable can throw some light on these points.

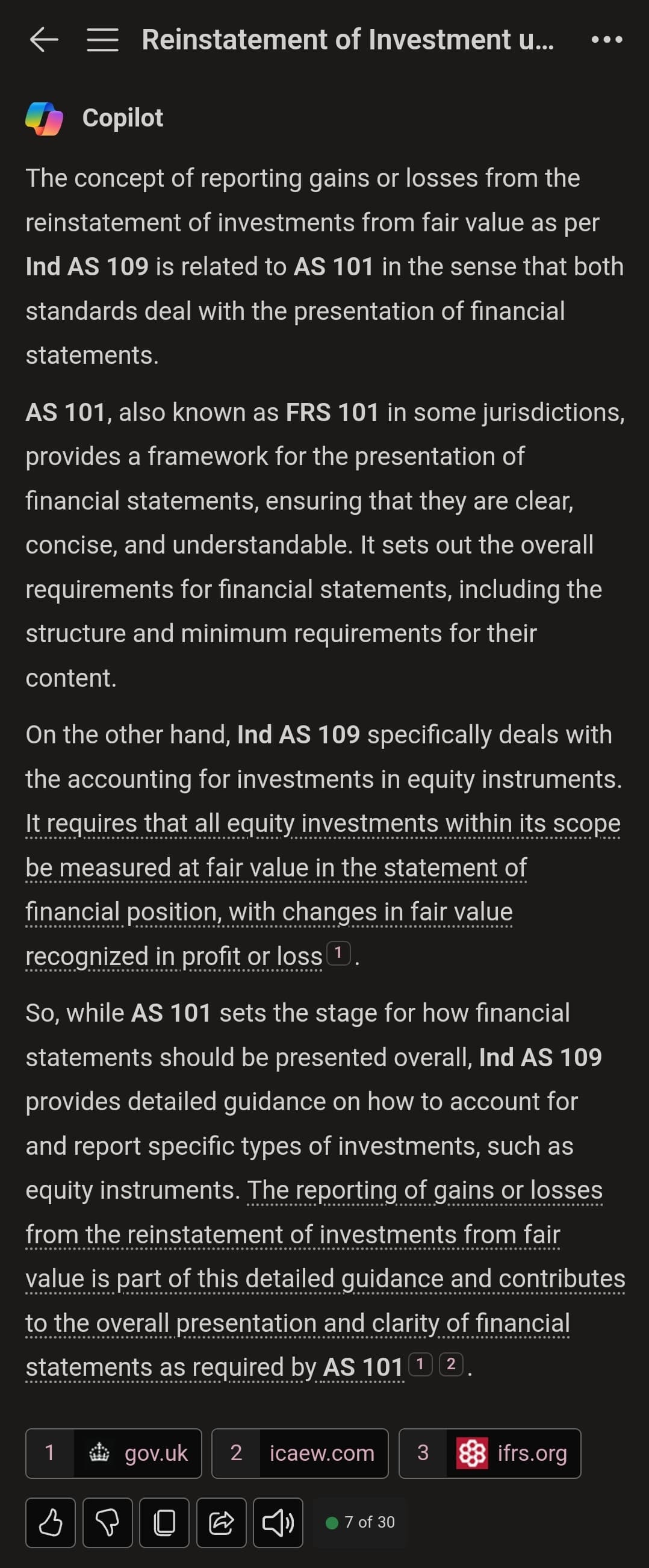

@Ashar_Mann could you please explain the same to me in the context of the AS 109 and 101 as I have almost zero knowledge in that area? However, will now try to check the accounting standards.

Copilot to the rescue. Simply amazing that I can’t resist sharing. Probed MS copilot like a 10 year old with a barrage of questions regarding AS 109 and 101 and presented the case of the above treatment of the Invits and the entire topic was explained absolutely clearly.

So,

As per 101 - When you first adopt Ind As there’s inconsistency in recognising revenue, cost, even leases, financial assets, etc

When you first move from AS to Ind As you have to make sure to give the restrospective changes as on the due date as the same is change in accounting policy.

Co. Had some understatement of 16 crores of PBT due to recognition differnece which they had booked last time the same is missing this time.

As per Ind As 109 FV gain on equity instrument is not opted for one time choice to route through OCI should be routed through PL

FVTPL makes this compulsion.

Hence, if you see the changes and take out the above effect,

Effectively the co. Has grown it’s bottom line by 20.833%

AVG enters into 6 year long contract with Indian railways.

"Through this Contract, while departure of the train from Agartala to Ludhiana the company will serve the industries in the field of Tea, Bamboo, Plastic granules, Mosquito repellent, FMCG, Hair oil etc. and departure of the train from Ludhiana-Delhi-Guwahati- Agartala which is the toughest location of northeast due to its geographical location and seasonal disturbances which affects regular road closures, land sliding etc. and this new train will help in serving the industries in the field of FMCG, Cycle, Hosiery, Electronics, White Goods, shoes, consumable items, Raw Material, Sanitary etc. We believe that this strategic move and committed services will have a positive impact on our operational efficiency, service reliability, and overall business growth. "

Recent acquisition of a warehouse for 32 cr shows the promoters ambition to expand .

Preferential issue at rs 222 .60 for close to 19 cr to promoters and close to 15 cr to non promoters.

nikhil Vora invested about 2 cr at 228

It specializes in road and rail transportation, cold chain logistics, warehousing, and value-added services like customs clearance and e-commerce fulfillment. With over 700 owned vehicles, 3,000+ associated vehicles, and 835,000+ sq. ft. of warehousing space, it serves major clients like Nestlé and ITC, indicating a strong B2B focus.

Mega-Trend Alignment: E-Commerce & Quick Commerce

A. Direct Link to E-Commerce Growth

Last-Mile Infrastructure: With 3,000+ vehicles and automated hubs, AVG supports e-commerce giants in Tier 2/3 cities, where demand is surging at 22.3% CAGR7.

Warehousing for E-Tail: Its 835,000+ sq. ft. network serves as fulfillment centers, critical for same/next-day delivery models.

B. Indirect Role in Quick Commerce

Cold Chain Readiness: 380+ reefer trucks and plans for 100 annual additions position AVG to handle perishables (groceries, dairy) for quick-commerce players like Blinkit or Zepto.

Scalable Last-Mile: Partnerships with India Post and UPSRTC (9,000 buses)5 enhance rural/urban reach, aligning with quick commerce’s expansion.

A pending ₹500 crore government tender (technical evaluation ongoing, price bids expected by March 10, 2025) could further boost revenue, with management expecting at least 20% revenue growth excluding this contract.