EBITDA margin they will cap at around 10%, gross margins are roughly 15%. As the sales is increased, operating leverage will play and EBITDA margins will increase, these margins will pass on to consumer to cap profitability at around 10%. I am saying all this on the basis of old statements of management. This is part of everyday low price. This will help to deepen the moat. If someone is able to execute/replicate the same business model, he has to get the same volume of sales to offer at the price of Dmart which is not easy.

Now they are building large stores to accomodate more items of consumer durables, consumer goods other than grocery. Consumer durables I am not sure but goods other than grocery have higher margins, increase in sales of this stuff will surely play a big role on operating leverage. Let us see how it plays.

Above news, further increases my convection toward dmat now. BB is one of the best, widely used e-commerce still making loss and not sure what will be thier strategy to turn profit. The only option is see pricing war which they are already into…what next will be something interesting to see in coming days.

I enjoyed reading your personal experiences and analysis on their private label business,it is good. Tired of reading valuation discussions and personal opinions. Just check whether posting your blog content violating this forum guidelines or not,if yes paste it directly in this forum.

And is their any way to get their private label business numbers?

Nice write up, as always your write up triggers thoughts and that’s good. Few points -

- Same private label trend for Star Bazaar since much longer time. They even have benefit of Tata product. They have also created many good private label brands like - Klia, Fabsta - all a Tata product, with Fabsta Tea/coffee being sourced from none other than Tata consumer products (I last checked this few years back when it was Tata global beverages).

So, Dmart is simply following a well trodden path from likes of Walmart & even Tatas…good to know that they are doing it good as well as few years back when I visited their store, I did not like quality & packaging of their private label products and saw huge scope of improvement compared to Tatas

- Now coming to point of Private labels spelling trouble for leading consumer brands…when a Walmart could not meaningfully dent a P&G, Unilever or Colgate in US where they do not even have the massive web of local Kiranas…I doubt that the most of leading consumer brands can face serious trouble by any retailer…

Why? - One small example which comes to mind from a recent update…take example of Himalayan range of preserves recently launched by Tata Consumer - that’s the result of product innovation & strategy at its best…a retailer cannot afford to have the same innovation engine and high margin product launches to target cream of the consumers…sooner or later they need to stick to their core competency and see their Private Label as just a means to increase their revenues & margins and get hold of some loyal consumer base, but the moment they think of it as a means to topple or dent any leading consumer brand - their focus would diverge and their competitors would take advantage of that…

Would be good to know your & others thoughts as well…

Disc. Invested in Dmart, Trent, Tata Consumer hence biased. Each has its own core competence and focussed management. Post only for academic purpose and no buy/sell recommendation. Not eligible for any advice

Not denying that leading FMCG brands will stand the test of time. But at the margin they are likely to get hurt with the rise of both private label and modern retailers like DMART providing quick and easy distribution access to brands like Wipro Consumer or a D2C type new comer. There is a reason why a Unilever or its peers in developed markets have grown much slower than private label sales of retailers of Walmart and Costco (brand Kirkland). Also, developed market FMCG operate at lower margins and a positive working capital cycle unlike Indian FMCG which has a negative working capital as they get distributors to buy in upfront cash. A good way to check this is compare the ROCE of HUL with Unilever. So, leading FMCG will remain forces and brands to reckon with but at the margin their best in class economics do worsen and their growth is kept in check with some share shift to private label and upstarts given a leash by the rise of modern trade and e-commerce (new age channels).

We are a large country, and not all branded retailers exist in Tier 3 towns and villages, even for the ones that exist in towns, sales and profitability are questions. Also, considering that small packets have bigger margins, there exist crores of small home-run kiosk type setups, where there is no sign of private labels. So to compete with the mind share through A&P, the distribution strength, the taste shift when it comes to F&B of big FMCG companies is very difficult.

So branded retailers may push private labels aggressively for their own good, but I guess that would be restricted to metros and Tier 2 cities, and not to Tier 3 towns and villages. And I think sales from metros and Tier 2 are less than the sales from Tier 3 towns and villages, considering 65% or so population still live here.

So I don’t see an immediate threat to the big FMCG brands unless there is a considerable loss in sales, more A&P spend, diluting margins etc.

Just my thoughts and, I have a position in Dmart.

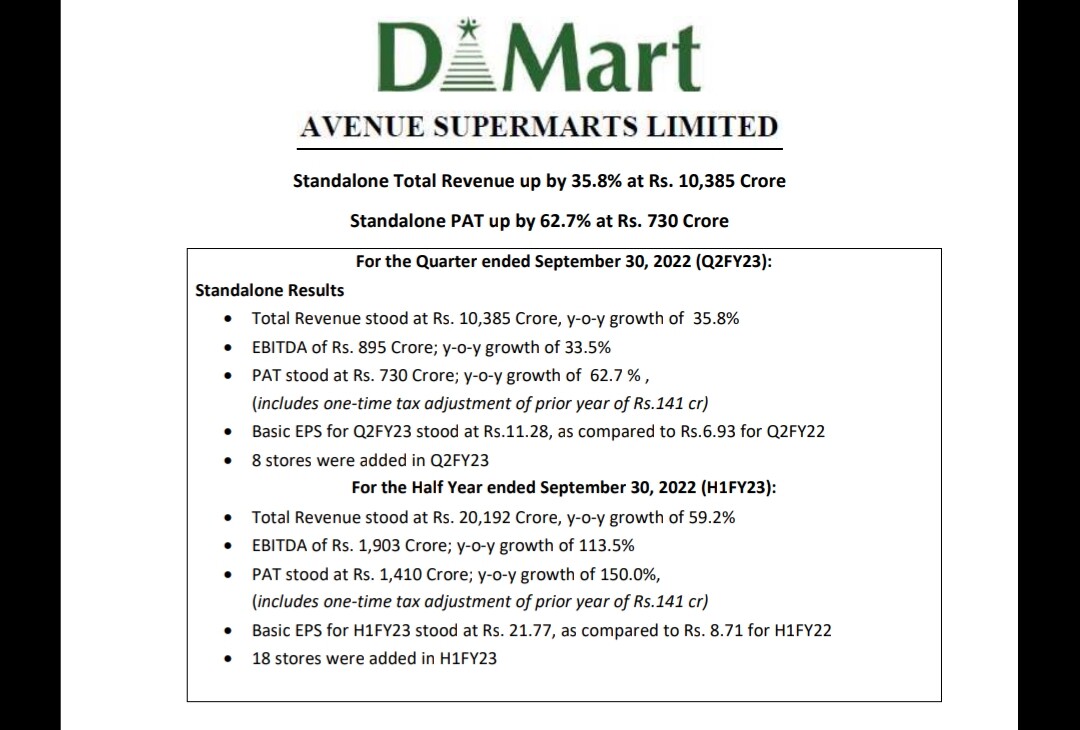

Standalone Revenue from operations for the quarter ended (QE) September 30, 2022 stood at INR 10,384.66 crores.

35.7% YoY growth

The total number of stores as of September 30, 2022 stood at 302.

Let’s see if they can maintain NP margin of 6.4 likewise Q1

September quarter NPM is usually less than June quarter (from 4 to 5%).

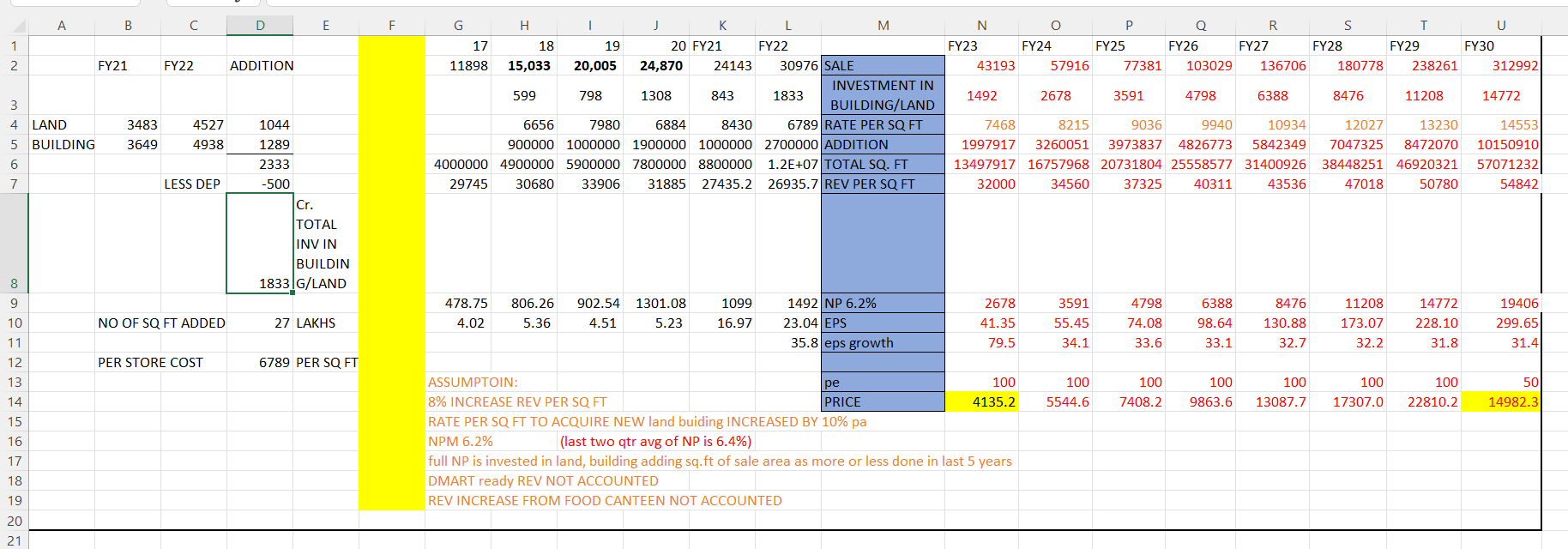

In last 5 year Dmart has invested apprx 5400 cr in land and building against 5 years of NP of 5600. based on this facts and following assumptions , have tried to forecast future expansion and turnover, NP etc.

assumptions

- 8% INCREASE REV PER SQ FT

2.RATE PER SQ FT TO ACQUIRE NEW land buidling INCREASED BY 10% pa

3.NPM 6.2% (avg NP of last two qtrs)

4.full NP is invested in land, building adding sq.ft of sale area as more or less done in last 5 years

5.DMART ready REV/Loss NOT ACCOUNTED

6.REV INCREASE FROM FOOD CANTEEN NOT ACCOUNTED

D mart.xlsx (13.4 KB)

views n comments highly appriciated

Your PE assumption till FY29 seems too aggressive , I would start with 75 PE on FY24 and reduce 10% consecutively and settle for 35PE.

Pre-covid PE has been lesser than 80 couple of times.

Hyderabad Dmart ready online shopping experience:

Dmart Ready is now delivering online orders on the same day. If we order in the morning, the items are being delivered between 12 pm to 5 pm. If we order in the evening, delivery will be on the next day morning. Earlier they used to take 2-3 days for delivery, so I only used to order once a month. Most of the items are cheaper at Dmart and the selection is much better compared to Flipkart or Amazon. Flipkart grocery delivery is the next day even if we order in the morning.

Packaging-wise, they will bring the items in a box directly and leave them at the door. No extra packaging for the items or carry bags. I like this approach personally as it’s good for the environment. It’s also cost-effective for the company. With good EV auto options becoming available hopefully, they will switch to EV autos for delivery.

A couple of cents For folks who are trying to model the earnings:

-

Dmart has a very special currency to spend for its growth, Its equity.

They are smart enough to utilize this in 2020 by raising 4kcr via QIP, by diluting just around 3% equity they have increased the Networth by 60%.

Please note that their networth is hardly 15k cr today, terminal potential could be in lakhs of crs. -

Dmart has a history[even before IPO] of funneling 1.5-2x of yearly free cashflows into store expansion, the additional cash requirement is funded with debt & when the time it right- they go for equity dilution.

-

Their inventory turnover ratio has been sliding downward from 14.5 to 12.5 levels, despite them still being the best- terminal inventory turnover numbers could be far lower- Which means more money requirement for incremental growth.

So, I’d suggest modeling that number to trend downward and settling at 8-9x on a terminal number while computing the free cashflow number. -

Simply putting the terminal P/E at 50x doesn’t make much sense, it all depends on the growth & longevity of growth. - In 10 years a lot can change for instance, a coupe of years back Quickcommerce didn’t even, exist now people are projecting it to be 5bill$ by 2025.

Putting more reasonable estimates in line with Walmarts of the world removes any element of surprise.

Disclosure: No holdings.

Quarterly results much below expectations. Although income grew 26% YoY, profit only grew 7% YoY. Tomorrow can be brutal for the stock

I am not completely convinced that the results were bad. There were no significant store additions in the last 9months which might have resulted in lower revenue growth but that is expected to be compensated by adding stores in Q4. Also the profitability front, lower margins are a result of lower discretionary spending by families. FMCG sales which are a low margin business is doing great. We just saw the festive season and the demand has normalized. We can see the Discretionary Business gaining traction going ahead. Also with increasing stores and sustainable revenue per sq between 35000-40000rs, we can see good growth in the topline and if they can maintain these margins, the bottom line will grow too.

Coming to the valuation front, it is now trading at 56 times EV/EBITDA of FY24 estimates. So yes, we can see some brutal downward momentum from the stock next week, but that will only give a good opportunity to buy the stock at good levels. Looking at the charts, the 200 Week EMA is at 3200. so there is a good chance the stock will see those levels in coming weeks.

I can be wrong, so don’t take this post as an investment advice.

Invested in this stock.

Avenue Supermart took great strides when it was ruling the retail market. Now that it is facing tough competition, it may not do so well. Perhaps R K Damani may take over Spencer’s. As of December 2022, Avenue Supermart has 306 stores across 14 states in India. If it adds the Spencer’s, as per the information I could access, 128 stores will be added to it.

On the other hand, Reliance Retail has 15,196 stores across 7,000+ cities with a retail area of over 41.6 million sft.

Avenue Supermart is definitely facing tough competition.