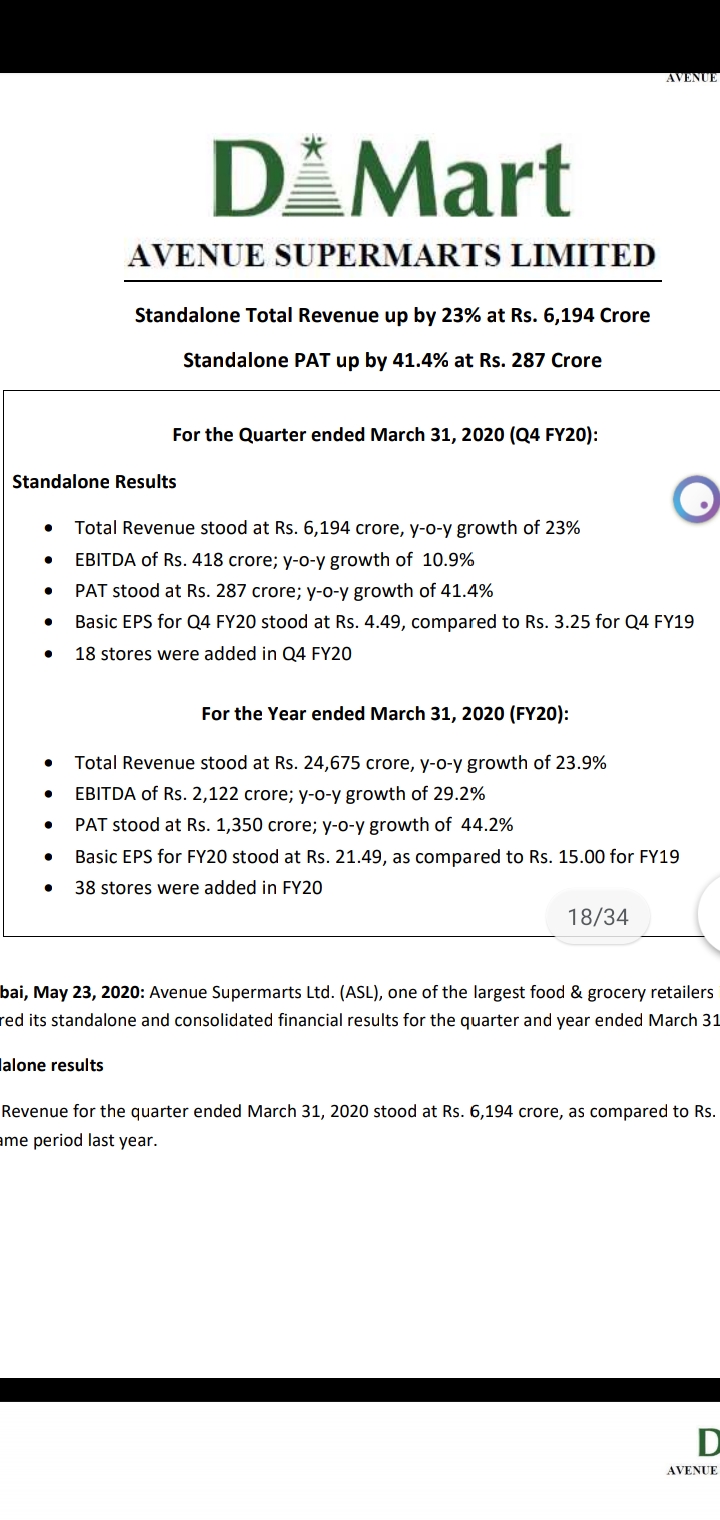

detailed result

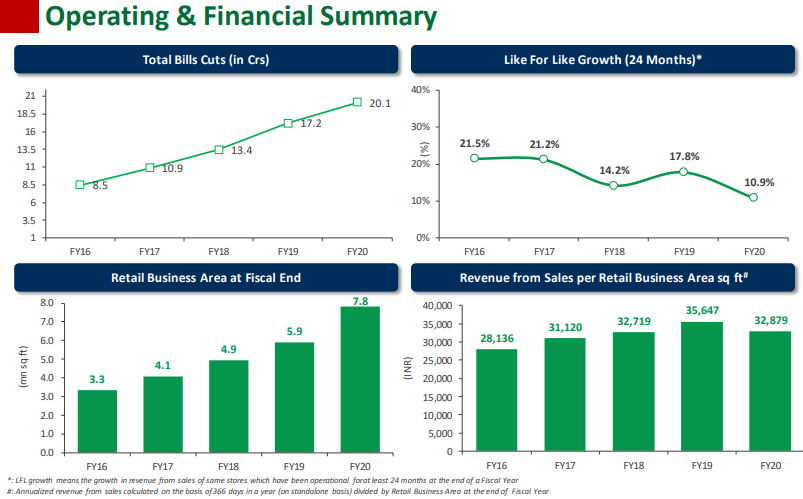

Above slide seems to highlight most of the concerns for Dmart

Growth in total bills cut have slowed down - It had increased by 28.35% in previous year and growth in current year is 16.86%

LFL (2 Yrs) is lowest since inception & approaching single digit

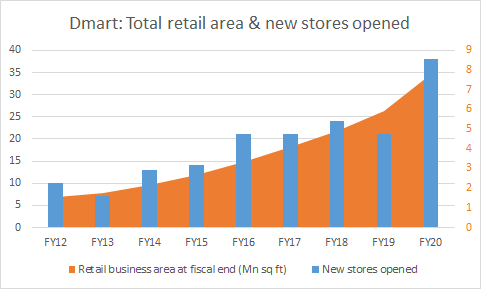

Revenue generated per sq ft area has also seen de-growth for he first time (even though if we discount it for disruption of 9 days in march’20)

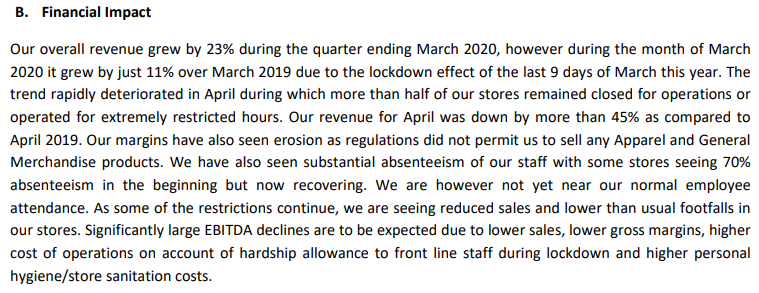

few key points

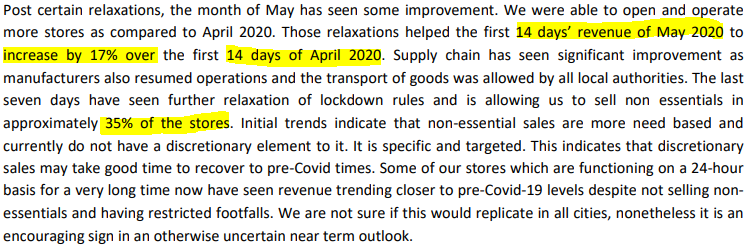

My rough calculation says that net revenue in 2 months (Apr’20 + May’20) of current quarter (Q1) will be approx 2000 Cr … it indicates that Q1 revenue will be around 50% of Q4

Revenue has gone down from 6809 cr (Q3) to 6290 cr (Q4) - we must note that the covid impact in Q4 was 8-10 days only… in normal circumstances they should have improved the numbers.

YoY - it may look better due to good performance in first 3 quarters but that is already priced in

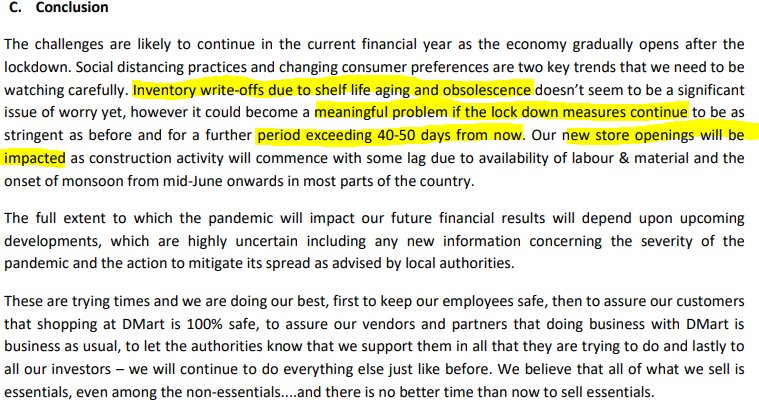

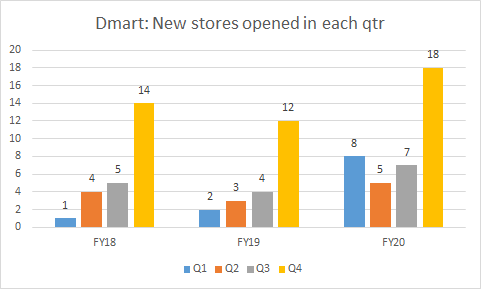

Total store addition is encouraging as its highest no in any quarter - 18 stores in Q4 alone (they will start contributing along with covid relaxations)

Earnings before Interest, Tax, Depreciation and Amortization (EBITDA) in Q4 FY20 stood at Rs. 417 crore, as compared to Rs. 372 crore in the corresponding quarter of last year. EBITDA margin is at 6.7% in Q4 FY 20 as compared to 7.4% in Q4 FY 19.

Net Profit is at Rs. 271 crore for Q4 FY20, as compared to Rs. 192 crore in the corresponding quarter of last year.

PAT margin improved from 3.8% in Q4 FY19 to 4.3% in Q4 FY20.

Basic Earnings per share (EPS) for Q4 FY20 stood at Rs. 4.25, as compared with Rs. 3.07 for Q4 FY19.

Total Revenue for FY20 stood at Rs. 24,870 crore, as compared to Rs. 20,005 crore in FY 19.

Earnings before Interest, Tax, Depreciation and Amortization (EBITDA) in FY20 stood at Rs. 2,128 crore, as compared to Rs. 1,633 crore during FY19.

EBITDA margin improved from 8.2% in FY19 to 8.6% in FY20.

Net Profit of Rs. 1,301 crore for FY20, as compared to Rs. 902 crore in FY19. PAT margin improved from 4.5% in FY19 to 5.2% in FY20.

Basic Earnings per share (EPS) for FY20 stood at Rs. 20.71, as compared with Rs. 14.46 for FY19.

Mr. Neville Noronha’s comments:

Overall, FY 2020 saw a healthy 24% revenue growth while PAT margins were in line with expectations. Our LFL growth for FY2020 was 10.9%. Two reasons for this. One is that stores that are more than 5 years old grew at a rate lower than the previous year and most of the stores that are younger are peaking faster, even before they qualify for the 24 months LFL measurement. We opened a record 38 new stores, 6-8 of those stores should have actually opened last year.