The current store count as per wiki & DMart is 177, I take it as typo on “About us” page. Dmart being mostly focussed on offline sales (I am aware of Dmart ready http://dmart.in), its acceptable also.

Few boarders had raised concerns on trusting wiki being crowd source data, which has the correct info in this case.

The thrust on exact store count at end of FY is important for investors to calculate growth & expected targets for investing decisions.

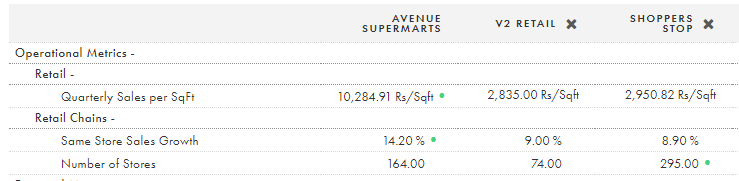

I find very interesting “Quarterly Sales per Sqft” numbers from tijori, which shows drastic change of almost 8% in hardly one month(its quite possible that they updated at end of quarter or FY). Still If it turns out to be true (at present, I don’t have a way to cross check from other source & need to wait for dmart to share details) then its really a great sign for bright future.

New store opening growth of approx 15% on top of new stores having more area (sqft) & further improvement in sales per sqft. Let us cross fingers & wait for numbers in coming week.

It also shows that Shoppers Stop is aggressively expanding, which can put a check on Dmart plans in apparels