I find it useful to look at sales growth as = (sales growth from existing stores) + (sales growth from new stores) - (loss of sales from closure of stores).

So just new stores opening might not give the full picture IMO.

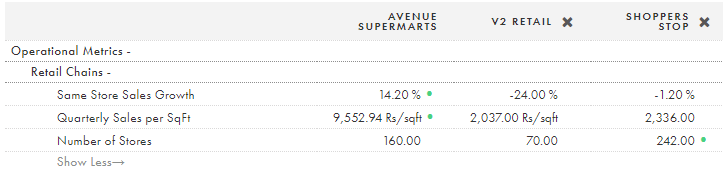

For sales from existing stores we can look at same-store-sales-growth which has been going down for Avenue.

Another metric for overall sales is sales per square feet which is going up. So IMO we need to get a wholistic picture by looking at all relevant metrics in addition to number of stores.

I noticed a change in the DMart store in my neighbourhood. It is a 2 storey store. Earlier the 2nd floor was for clothing, footwear, crockery, appliances, home furnishings (curtains, pillows, bedsheets) etc. The space was roughly equally divided for all these sections.

For the past few months the clothing section has started dominating the 2nd floor, with about 60% of the space. Home furnishings (~15%), home appliances & crockery (~20%) and the balance with footwear.

Did any one else notice this for other stores? What could be the implications of such a change on the revenue and margins?

It’s the same noticed in my neighbourhood DMART store as well (Pune) and is pretty much in line with the management commentary perhaps a year back. Almost half of second floor now contains menswear, womenswear and kidswear. Given the same product quality, the price point seems apt when compared to Reliance Trend, which helps attract large crowd. Would assume margins to better in apparel compared to groceries - VMART that seems close to this line of business depicts 8-11% OPM over the last decade.

Same has happened at Sanpada store in Navi Mumbai. Also the floor space is better utilised now , the billing section has more counters with more space for queue . I have experienced drastic change in the waiting time for billing even in peak hours.

The focus looks more on reducing the billing time by re - organising the whole store and also towards selling more of high margin products like clothing and footwear.

Also I have noticed , they have launched many self promoted brands like Royal Toast , which has more shelf space as compared to say Britannia and Parle rusk.

Maybe these small steps will help to increase the margins , keep an eye towards the margin this quarter.

Avenues Supermarket am not big fan of retail However if one has production of scale to be low cost producers of the Goods and is front runner amount=g the pears than we can think about investing in that scenario in any retail company .

How fast the inventory getting turnover and what is the cash Conversion cycle .Every retailer has dream to get the cash fast and want to pay to it’s supplier as slow as possible .So to have some homework You may need to find these CCC / Inventory Turnover

Cash from Financing Activity Proceeds from Shares in 2017 ->1840.62 Which very Huge apart from No History of dividend payout is negative for me .Low entry .Retails always have very Narrow Moats if at all exists .

Last 4 years Inventory Turnover with in range 15-16 Which is Good .

Generally retailers works on very thin margins .

so my quest if any with investing will remain same will this for next 10 years

Company has history of Issuance of Commercial papers which is an unsecured, short-term loan used by The company . Company does not provide any reasons for that but i guess it may be for financing accounts receivable and inventories. It is double edged

In every business especially in Retail Consumer is the Key I found a couple of complaints

Whish is not encouraging in long run so have so much exposure may prove to be fatal

Disc : I am not invested and not any sebi approved analyst

Regards

I have different take on DMART. Consumption is a very large percentage of our GDP and grocery+fmcg+apparel all together are very big part of this consumption. Now how many prominent players are their in this market not more than 6-7. DMART understands market I see a lot of footfall in their stores which shows they know how to serve this market. Another point is Promoter has to sell his stakes which i believe will not let the price fall in a short period.

If we don’t think for long period ( more than 1-2 years) this could be still a good bet. At least we can see this company competitiveness beyond financial statements.

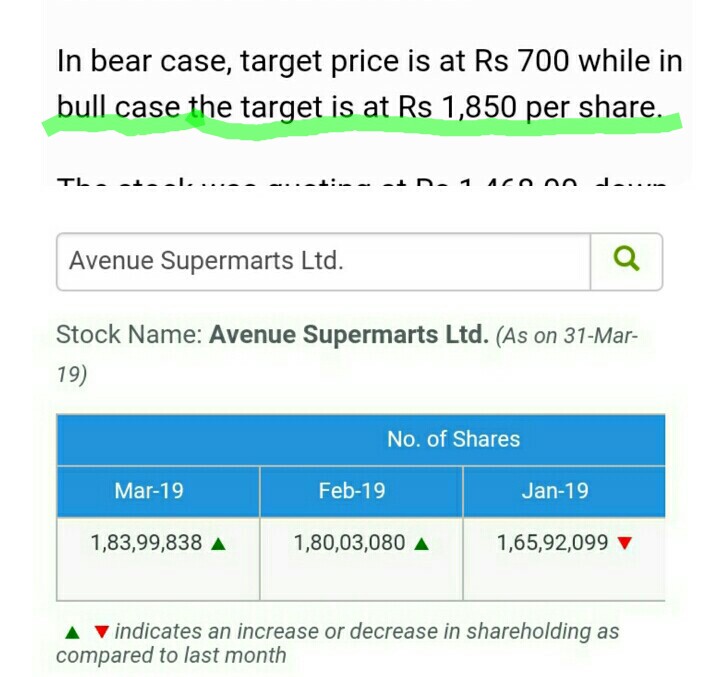

we should take this MS or any brokerage reports with pinch of salt…see similar report came out for RBL and yesbank on Oct 22 2018…RBL closed 469 that day and today almost after 6 months it closed at 671 that is cool 44% return for 6 months and yesbank from 211 to 255 that is 20% too

In this same brokerage report they have mentioned the bull case scenario too

I am attaching the last two months MF activity on this stock to understand MF house sentiment.

not pinch of salt, but completely ignore all of these…infact i dont even bother to read them as they all have either some motive or the analysts are immature to analyse the business.

I am keenly awaiting for the Q4 results which will give the direction. Last 2 quarters have been volatile for Dmart and thus market is providing negative sentiment.

SRS retail recently shut down its retail operations due to inability to manage rental exp and debt. Dmart is well covered on both fronts. Its further addition of stores in the high per capita zones of Maharashtra and telangana also provides further stability to its growth plans. The scale at which it is now operating makes it difficult for any retail operation to breach it even for reliance retail which is India’s largest retail chain in terms of sales.

In a nutshell, its difficult to compete against Dmart and emerge profitable. Valuation has been well discussed with people holding strong views on both sides. For valuations to go south there needs to be some trigger internally or externally in the business. So far, I can see none.

I know DMart valuations are very high. But it is the efficiency and planning and the strategy which makes me positive about this company. The opportunity size is huge and it is up to the retailers to go ahead and open the markets for themselves and away from the local kirana stores.

Now this is a tough job. Any new player who goes to a previously town not been served by the big retailers will need to spend money upfront to win over customers. From my observations DMart does not do this dirty job. This job of opening up the market and making new customers is undertaken by the older players.

I have some anecdotal examples. About 10 years back In my locality we used to have Big Bazaar. We all used to shop from there. But for some reasons Big Bazaar started doing poorly. Their merchandise became thinner. We used to get only 60% of all things we needed. One reason was a new DMart came in a neighboring locality. So slowly we started moving towards DMart. We used to drive 6 Km to go to DMart to shop. Then after a couple of years Dmart came to our locality and in a very short period of time the Big Bazaar closed down.

My wife is from Bhopal. They used to shop from the nearby Reliance and so they did for a few years. Now that Dmart has come they stopped going to Reliance. I know one swallow or even two does not a summer make. But my observation is other retailers go to places to open up the markets and DMart comes along with their much superior supply chain, pricing and other efficiencies to take away market share.

There are about 500+ Reliance stores selling groceries and vegetables. To grow at 20% they need to open roughly 100 stores a year or more. Maybe 75 and other 25% of the 20% growth comes from same store growth. DMart just needs 25 stores to grow 20-25%. I am not counting the Reliance stores which sell clothes and other households. So it is much easier for DMart to encroach on Reliance territory than the other way round.

This is where I feel DMart has an advantage along with the efficiency of their operations. It could happen that Reliance may throw infinite amount of money to capture market share/destroy competitors but since they have so many other businesses capital allocation to retail alone won’t be good enough for Reliance.

@sincyvarghese Great observervation and fully agree with the following [quote=“sincyvarghese, post:1083, topic:9270”]

So it is much easier for DMart to encroach on Reliance territory than the other way round.

[/quote]

I’m a long time Dmart customer myself and I’m unable to break the habit. Even when I go to my hometown in Karnataka, I keep asking if there’s a Dmart.

Off and on I’m able to find better bargains at the local kirana (especially sugar) but on the whole DMart offers me a far better deal in terms of wide variety of choices at different price points, superior quality, their private label Premia also comes to mind here.

Dmart atleast at my Pune location has been able offer a superior deal in comparison to Amazon Pantry, consistently, and as a result is better than Big Basket and their ilk for pantry items.

Right now, the only possible issue w.r.t Dmart is that I need to go to the store physically and get my shopping done. Because of the cost and quality advantages, this makes sense.

I guess the last piece of this story to look out for is when DMart Online happens. The holy grail will be if Dmart is able to offer all this superior value proposition even when I’m able to order stuff online at a cost of operation that makes sense in terms of competitiveness and profitability, including in tier two towns/cities. Since rival Reliance Retail is already offering this choice in terms of convenience, Dmart cannot afford to get this wrong.

And and and

It’s eyeing to overtake all the likes of Amazon’s and Walmarts , it’s Target is not D Mart.

But there will surely be short term disruption which will be opportunity to enter D Mart cheaper rate.

The article says now fashion segment forms 37% of the total revenues of BigBazaar. Fashion is the fastest growing segment for BigBazaar and Reliance. I think we will see this trend playing out for DMart as well. Myself and other members have pointed out how the store layouts have changed and how more space is being dedicated to apparels at Dmart stores now.

Enjoyable ( & also food for thought) article outlining a thought experiment pertaining to Walmart valuations that puts things in perspective (regardless of your views). Do go through the 1974 Walmart AR - link is given in the article - and some good similarities with the present day Dmart in terms of size of stores, no of stores opened and rent to sales percent of ~1.8%. R

absolute classy article.Thanks for sharing.

In todays noise, people dont have patience even for a quarter.Everyone wants a linear, non-volatile graph for the stock.

Lets hope market teaches some valuable lesson once again.

The store count is at 176 as I get from D Mart site itself. Which means FY19 store opening count is 21-22 which is very less than management guideline of 30 store per year. We have to see how this will impact the revenue.

Since they have opened 22 store so the Store growth is 14% and considering SSG growth at 14-16% the total revenue growth should come at 28-30%.

Although last time I have heard that new store area is larger than it’s old ones. So my assumption might differ on that but unfortunately I do not have any data on this.

Also since there will be no more decline in other income like the last quarter so we can expect a good bottom-line growth as well.