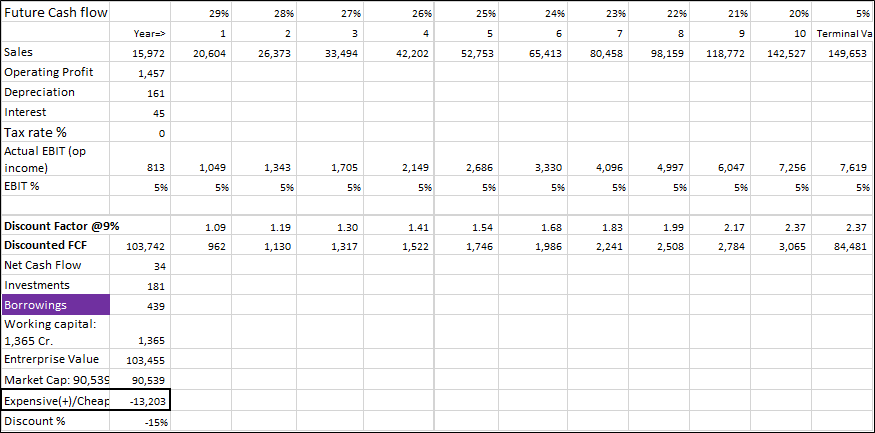

The YoY Revenue growth has been steadily coming down from 50% for FY13 to 30% for FY18 (perfectly logical as you cannot grow by 40-50% YoY once you attain a certain size). So, a somewhat optimistic estimate of Revenue CAGR over the next 5 years would be about 25%.

Next, lets come to Net Profit. The NPM has been steadily increasing, from 2.8% for FY13 to about 4.8% for FY18, resulting in Profit Growth being higher than the Revenue Growth during this period. This is also logical, as increase in operations create certain operational synergies resulting in increase in margins up to a point. However, margin increase has it’s limits, and beyond a point it becomes stagnant or might even decline as increased size of operations tend to create certain operational inefficiencies.

So, a safe assumption would be that NPM cannot increase significantly beyond the current levels. Hence, the Net Profit CAGR over the next 5 years would be similar to the Revenue growth, i.e., about 25%.

Next, lets come to valuations. As the expected growth beyond 5 years is unlikely to be more than 20%, the market is unlikely to assign a P/E of more than 30 at the end of 5 years. So the combined result of tripling of EPS (25% CAGR) and P/E falling to one-third of the current levels (of 100+) will result in the Share Price 5 yrs down the line being the same as it is today !

Disclosure: No Investment - Unlikely to invest even if it falls by 50% tomorrow