Great results. Unreal execution skills.

Please refer to the previous discussions - The QoQ revenue and profit figures historically has not been linearly progressive (possibly due to festive season and other seasonality in buying decisions I guess).

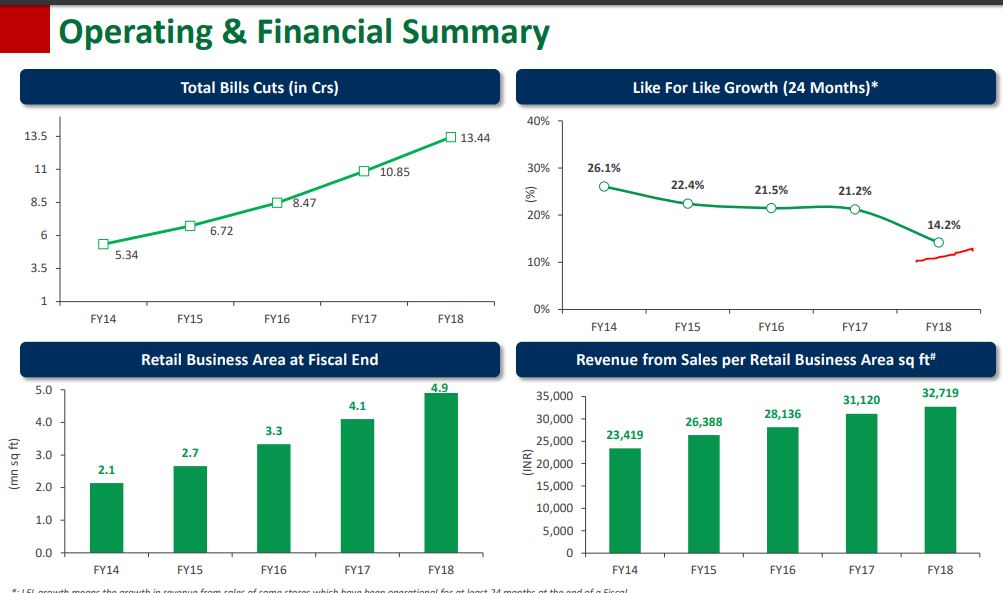

Obviously the performance didnt meet the expectations of some analysts - how ever, let us not disregard the superlative performance YOY basis and new store opening.

3 Likes

No so great results… expectation was about 200 cr PAT.

Also, I just come across this news yesterday about Weights And Measures Department Raids On DMart and around 6 cases logged against DMart, sheikpet branch. Also seized all the weighing scales and took them along with them.

A huge reputation damage in telugu states. This team has also logged criminal cases against More Super Markets (Aditya Birla Group).

2 Likes

Management already clarified it due to ‘Deflation in staples,tax rates not being comparable,store addition not in line with expectation & base effect of demonetization has made March 2018 revenue a little tepid’.It is still more higher than nominal GDP

Was there a concall for these results? If not, any idea when is it? I could not find details of this on the investor relations page of dmart’s website.

Dont think DMart arrange an investor concall.presentation and result and auditor report can be found on bse.Hardly 3-4 page presentation.Share price is doing wonder to them already no need for concall or massive ppt to influence investor from mgt side.

I have a different view on the purpose of concalls. Concalls are not to influence investors. Every management has the responsibility to answer their investor’s questions. After all the investors have provided capital to grow the company, don’t they deserve to ask the management a few questions? Why do you think Warren Buffet hosts a very public AGM for Berkshire Hathway?

There are many other stocks which have provided very good returns to shareholders consistently - Eicher motors, Bajaj Finance etc. They all have concalls after every quarterly result. It is their responsibility towards investors, they are not doing it out of their goodwill.

3 Likes

http://www.bsaravanan.co.in/entries/stocks/buy-from-dmart-but-not-the-stock

My analysis on DMart.

2 Likes

Sir,

This is a very interesting and knowledgable analysis. Highly appreciate. My views none the less as a learner:

-

Comparing Infosys with Dmart may not be exactly right as target markets and segments and timings are quite different.

-

Since 4-5 years back, friends have been talking of similar issues and repeated posts about Page Industries and Gruh Finance on this forum. Both these have given decent returns in the last 4 years.

-

You are right that there will be huge competition, but in imho, not from Grofers and Future group but from Flipkart/Wallmart and Amazon. Comparative valuations of Flipkart and Amazon India are nothing to right about.

I am beginner in investing in the sense of learning. So kindly do not take my views as opposite to what you said. Highly appreciate your post.

Dear Reader

Thanks for your valuable comments.

As a value investor, I would give a huge weightage to margin of safety under all market conditions. Infosys was mentioned to show the impact of paying a huge premium for any stock. If you are holding a stock for a long time, a good entry point is needed. Instead, if we pay a huge premium, our stock might underperform or might be impacted negatively upon any negative news.

We would be interested to know how these stocks deliver earnings during a bear market. Keeping these points in mind, an investor will turn the odds in his favour by paying a lesser price for quality stocks.

2 Likes

Hello Everyone

What is the threshold limit a promoter can hold in a given publicly listed company. Currently Mr Damani is holding 82.2 % and is planning to sell 1% in the open market to comply with the govt. rule. After this sale he will still be holding 81.2. The stock currently is taking a beating, I am wondering what if sell’s again. Does anyone help me with this - How much will Mr Damani have to reduce stake in order to comply with govt. norms.

Also i belive the stake sale would be in a staggered manner over a period of say 2 or 3 years.

Thank you

I am not sure , but I think its 75 %. Promoter should not hold more than 75% (I may be wrong also)

That’s about 850 Cr based on current valuation and I don’t think the market has enough liquidity to absorb that in that period of time. If its 5% down even before the sale has happened and considering there could be a lot more to go, the valuations are soon going to become quite reasonable. I had speculated this scenario. Now its more a Supply/Demand game.

Another thing is that now we are over a year since listing and considering the stock is trading above Jan 31st highs, the temptation to book LTCG could be high as well. Let’s see.

3 Likes

Hi

Currently the promoters hold 51,30,20,000 shares at 82.2% shareholding. A drop to 75% is roughly 4,49,56,636 shares and at current market cap its approx 6,721 crores. Selling 62 lakh shares ( 927 crores) currently is only 14% of the total shares promoter is selling. I guess there could be some ease of valuation coming up.

As per business channels 1600 crores buying is expected as per analysts. That still leaves approx 4,200 crores worth of market cap.

Rgds

Deepak

1 Like

Is this Supply Demand Game Applicable for GRUH Finance also? I am waiting to enter in GRUH from 2011, not entered that time due to High Valuation(10+PB) and same logic of low supply stock . In the mean time It have given bonuses 2 times (10:2 in 2012 and 1:1 in 2014)which provided enough liquidity but stock is up 10 times despite of staying overvalued (10+ PB) . Are we missing something for this type of companies which can’t be captured in Excel?

1 Like

Yes you are bang on the issue. Now for 1% selling the reaction has been pretty strong. If the promoters have to reach 75% level-wondering what will happen? Guess it will be 60-70 PE stock. What is the time limit they have to get to 75%?

The timeline seems to be 21st August based on recent Sebi guidelines. Though I don’t know if there would be a waiver for recently listed firms.

The timeline is mar 2020 till then I don’t see any reason to get into this stock as there will be continuous supply of shares and when supply of this size come in open market …everyone will tender their shares and wants to get out.

Why isn’t Mr Damani selling to some Institutional Investor?

The only reason he would sell in the open market is if there is not enough demand for the shares among institutions. But that seems weird given the huge target prices they are quoting in their research reports.

Any thoughts?

1 Like