They are included as well. People will put their towel down during down markets. Keep watching!

And always about HDFC Bank, Kotak Mahindra…

By the way, yet to see a company go down in a 3 year period if eps is growing at 20%+ and revenue at 10%plus; irrespective of valuations. Any examples, dear Sir?

I believe every stock- low PE or high PE will be battered during a bear market. High PE stocks experience market capitalisation erosion not necessarily because of their elevated valuations, it could possibly be because of the pessimism that envelopes the market.

So, instead of expecting erosion for high PE stocks we should expect it for all stocks- irrespective of valuations.

And hence,when we invest in the market we should be prepared to see significant reduction in the value of our investments.

3 Likes

Many people have similar views and then there are others that keep saying that they will buy after x% correction. Just makes my conviction stronger. Not planning to sell till DMART covers all the remaining states in India and may not even sell then.

Disc - Invested since lower levels and adding on corrections.

Some businesses are such great operations that no one shorts them. In such a scenario the momentum play is massively profitable.

Hence a Netflix or Dmart can even sell for 200X and still they won’t be shorted.

These will only time correct .even if there is a bear market people know they can just hold on

This is what differentiates men from the boys. Truly great companies understand what matters in the long run in the retail business selling items of daily needs which creates a positive feedback loop. What surprises me is both Raghuleela and Inorbit are at a stone’s throw away distance opposite Vashi station and with the hypercity acquisition by KB, opening BB will only cannibalise sales of hyper city and vice versa. I know someone who works v closely with KB and the more I hear about KB from him, the more I get convinced that the lack of focus of this group will limit its scale. When the going gets tough, FR will face the heat.

1 Like

I am a shareholder in DMart. Those of us who are shareholders need not be cocky about our good decision in owning DMart because the markets can make monkeys out the best and brightest any time. Even Jim Rogers and Marc faber have been proven wrong for a decade about their call about gold.

Having said that I feel it is better to hold a higher valued company which is among the very best in the industry than in owning undervalued companies which are not focussed on operational excellence. Again my opinion only.

8 Likes

7 Likes

Hi

With Jeff Bezos shareholder letter out an important point to note other than Amazon having 100 million prime customers is that he calls out India as a recent milestone. 40 million local products are sold by 3rd party sellers and more importantly India has the fastest uptake in the first year of prime in any geography. It’s also the most visited website and downloaded app in India in 2017 apart from the being the fastest growing marketplace. Also do read the Whole Foods part. Interesting.

In it for the long haul.

Amazon_Shareholder_Letter.pdf (125.6 KB)

Regards

Deepak

Disclosures

Invested in dmart from low levels.

I work for Amazon so views might be biased.

10 Likes

An excellent read. Thanks for sharing. Buffet says ‘When a management with a reputation for brilliance tackles a business with a reputation for bad economics, it is the reputation of the business that remains intact’.

Another version of this will be ’ ‘When a management with a reputation for brilliance (high standards) tackles a business with a reputation for great customer loyalty and economics, the end result is AMAZON’.

4 Likes

Amit Mantri’s tweet today

D-Mart valuations now imply 25%+ EPS growth for the next 20 years. No Indian company has been able to ever achieve this from a 100 mn $+ profit base.

Understanding base rates very important. Don’t bet on what’s possible but on what’s probable. https://t.co/Ht4tUayR4d

2 Likes

Too much gyaan on overvaluation.Quoting certain individuals is of no use. The more value investors scream-Dmart makes new highs.Taking a shot at 25 years is a bit of a joke.

1 Like

What does these people know?

- Not even seen 2009.

- Love DMart so much so that they regularly keep on tweeting about it.

- Funds being run are less than 2 year old.

- Fund’s performance in FY 2018 ( first full year) needs to be checked against Midcap, multicap, small-cap indices and not merely Nifty 50.

- Reporting of performance not in CAGR but overall for 20 months may mis-lead.

- If people have guts, let them short heavily than “selflessly educating foolish investors” on Social Media.

Advice - Do not fall for those who are running PMS and giving Gyan to get some Clients.

2 Likes

Amit Mantri suggests to read the base rate book by Michael mauboussin.

With a company like Dmart, selling at 120 pe, it is not enough to disclose that you are invested, but also disclose how much of your networth is involved in the bet, and at what price you purchased it, instead of enticing others, for the sake of selling to them, like a pyramid scheme.

Guys, very disheartening to say but I feel this is the poorest quality of discussion we can have on such a great forum which has given n giving us so much knowledge . What may not be relevant to us does not mean is not relevant to world and vice versa. Above all, rather than getting into commenting more on others views, let us stick to logical analysis of stock.

Forget about learning stocks and investments, I think the 1st thing we could learn from people like @desaidhwanil Bhai @hitesh2710 jee and @Donald is how to lead discussions when there are counter arguments in a healthy manner rather than calling this is waste, that is waste. Sorry but deeply sadened by poor display of debate.

37 Likes

Did my own ground testing of prices at dmart and bb on same day, bb current campaign/claim of EDLP and a brokerage rpt showing bb price now cheaper then dmart is a sham… imho

3 Likes

“Psychologically, I don’t mind holding a company I like and admire and I trust and know that it will be stronger than now after many years. And if the valuation gets a little silly, I just ignore it. So, I own assets that I would never buy at their current prices but I am quite comfortable holding them.

Well, I am almost constitutionally. . . I have a defect. And I just won’t pay 30 times earnings… I have never done that but I have one or two now which are now worth 8 or 10 times what I paid for them and they are still marvellous businesses and are still growing and I just hold them. Many investors I know are like me. I cannot defend it in terms of logic. I don’t defend this logic. I just say this is the way I do it and it keeps me more comfortable to do it this way. And I am entitled to this, it’s my own money and I am entitled to do it my own way. A lot of people are just like me. Li Lu is just like me. He will hold things that he bought a long time ago at tiny prices in what are still great companies but he won’t buy more.” — Charlie Munger

6 Likes

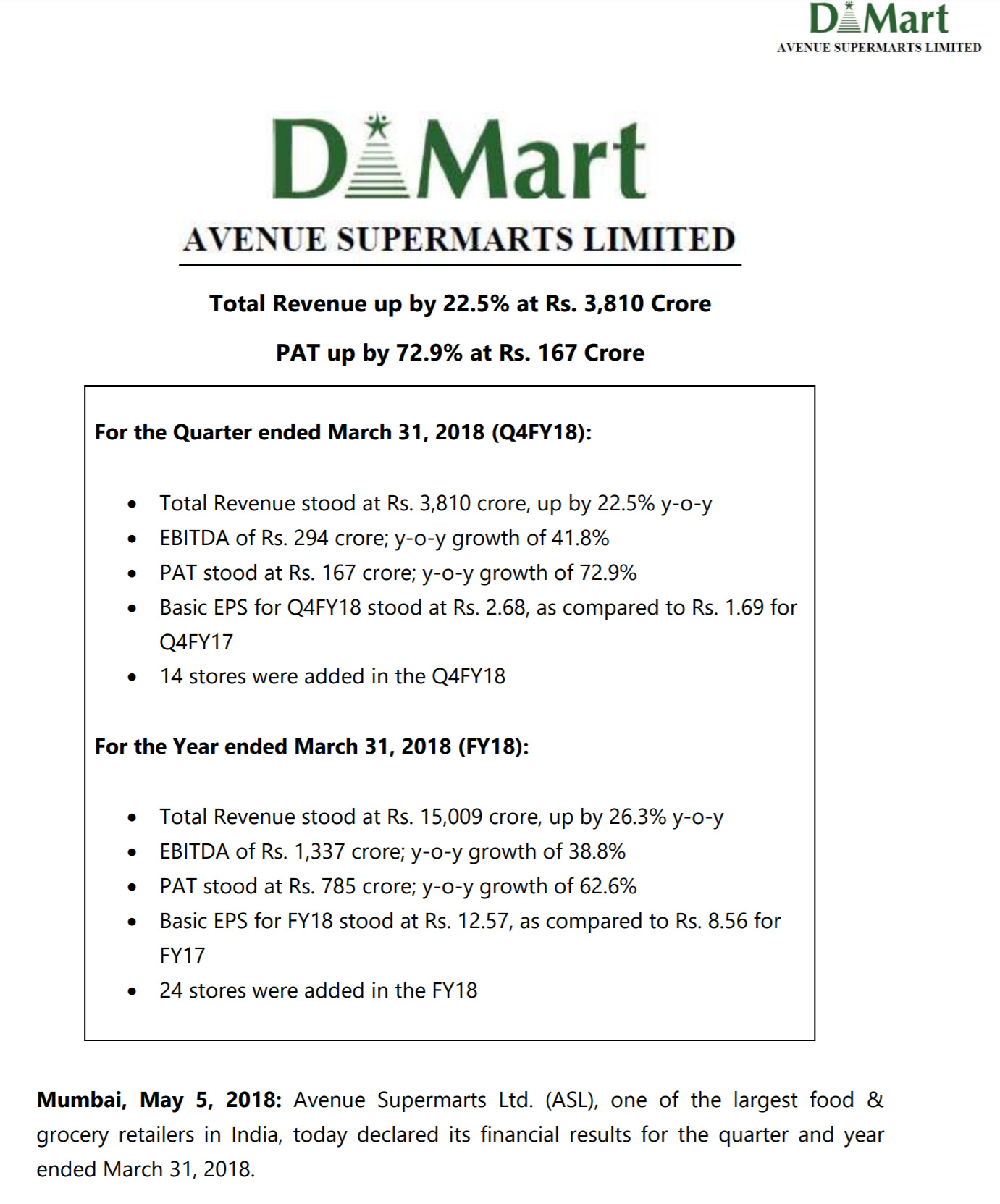

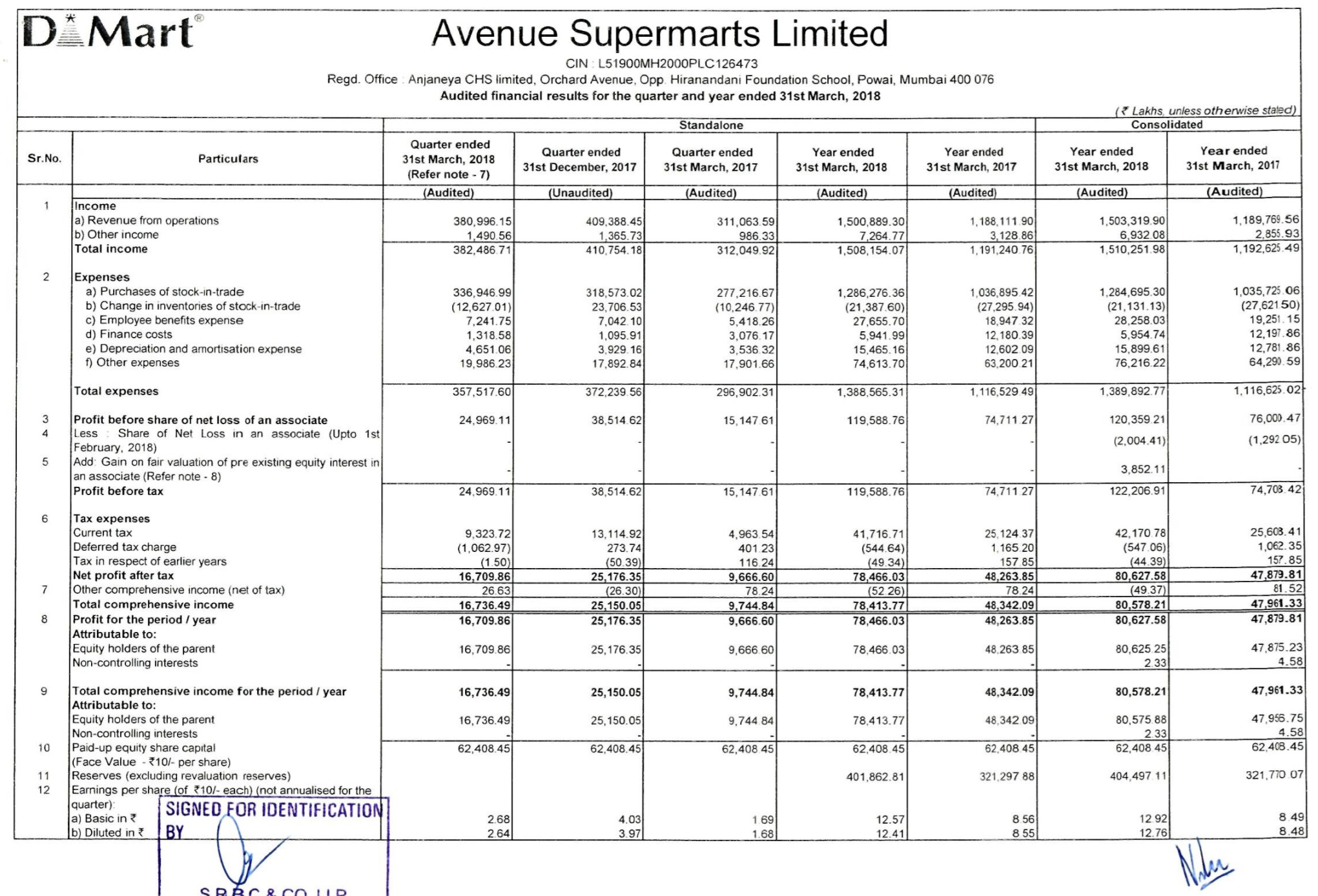

Results are goodY-o-Y, but disappointing Q-o-Q considering street was expecting Net Profit over 200cr atleast considering the valuations it is trading at ! Few such quarters of average results and this stock should trade near 1000 bucks !