Yeah , but after that market gave it high PE of approx 30-35 also , currently PE is 18-20 , do you think it will assign the same PE , if we are not going to get that kind of growth (at least 30%). That’s the question I have ?

Here are some of my observations based on friends and relatives who are into shirmp farming in Andhra Pradesh:

- There is huge drop in shrimp prices this year, especially for the last 2-3 months. For the same count (ex: 30) the price is dropped by 40 to 50% which is very huge.

- With such huge and sudden price drop, most of the farmers may get losses even with good production on average.

- Farmers are protesting in Andhra Pradesh because of this huge and sudden price drop.

- Even though there is higher farming this year, the main reason for this price drop seems to be because of processing plants collusion. Its not solely because of higher supply.

While this may not impact the immediate profitability of Avanti feeds or Apex frozen foods, there will be definitely an impact later and growth may be subdued for next year.

9 Likes

9 Likes

We cannot predict the market. We can only control our risk. By not giving a higher P/E multiple…that is what the market is doing. Capital allocation is where the skill of the investor lies.

Shrimp costs should not determine the P/E to give for the company

3 Likes

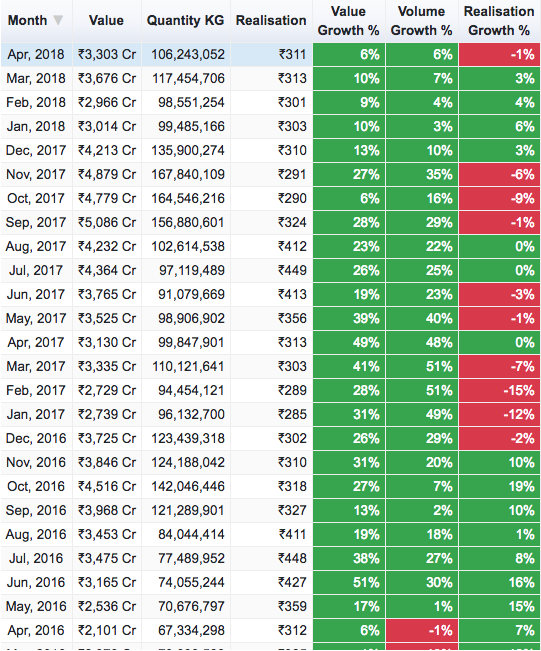

Hey, is it just me or the price is showing a trend.

It peaks in May,June,July,Aug & subdued in other months.

Also can you share source of this data?

Would you mind sharing your source. I am looking for old historical data. Will be very helpful.

Thanks.

2 Likes

Avanti Results announced.

IMHO results are ok-ish. Not so great not so bad.

Was worried after reading so much negative stuff on this thread.

My notes:

Q4:

Revenue Growth Q4FY18 Vs Q4FY17: 24%

PAT Growth Q4FY18 Vs Q4FY17: -3.2%

Full Year FY18:

Revenue Growth FY18 Vs FY17: 30%

PAT Growth FY18 Vs FY17: 105%

ROCE FY18: 72% {FY18 EBIT / (Avg. Net Worth + Avg. Non Curr Liabilities)}

ROE FY18: 50% {FY18 PAT / (Avg. Net Worth)}

P / E : 19

Earnings Yield: 9% {FY18 EBIT / (M Cap + Debt - Cash - Curr. Investment)

Disclosure: Invested and happily holding

6 Likes

Avanti results are out:

Highlights - 1) Anti-dumping duty is minuscule sum of 78.88 and not a deterrent as feared by many.

2) Volume seems to have increased (which brings out the point that shrimp production being at all time high so as the requirement for shrimp feeds)

3) Healthy Dividend Rs. 24 per share

Concern: Cost of raw material consumed is very high 80% of sales as against 68% for Q3 and Q4 of last year.

Can anyone explain:

The sharp increase in raw material price

huge fluctuation in change in inventories, what leads to such wild variations in inventories

Q4 - (-3543) Q3 - (-997) Last year Q4 - (+1885)

1 Like

Shrimp feed raw material price is linked to soybean price.since Jan 2018 to Mar 2018 soya price has increased more than 20%.hence this jump in cost of material consumed in Q4 Avanti result.

Dividend is Rs 6 per share which is 18 rupees not 24 rupees

Thanks @SMondal15

Thanks @soodhakar for correcting…I got confused between bonus issue of 1:2 and 2:1.

Can you explain the wild variations in inventory value in case of Avanti

Curious to understand why you think this industry is cyclical. Do you mean dependant on weather patterns or something else? Demand for shrimps is a function of structural shift towards premiumisation as incomes rise. While yes this demand is discretionary in nature, let’s not forget that so it is for the likes of Nestle etc

Your assertion of farmers quickly switching to other options also is difficult to understand as per my understanding shrimp farming is done on brackish areas where cultivation of other cash crops isnt easy.

Cyclicality in any industry is generally not caused by demand shifts, it is caused by increases in supply which are lumpy. In this context if you have 1-2 years of good prices leading to huge profits, aquaculture farmers shift wholesale to that product causing demand supply imbalance and a consequent price decline, which is what seems to be the case here.

Conversely unlike in say metals if you build a 3million MTA plant the market is stuck with it till demand rises to meet increased supply, in agri based products the supply is also flexible i.e the farmer moves from shrimp to something else (other seafood products) so the imbalance will correct faster.

In aquaculture I am expecting good demand growth with GDP increase as well as lifestyle factors but what one has to realize that while increase in volumes comes with an increase in costs, an increase in realizations goes straight to the bottomline. The reverse is also equally applicable on realization decline which will play on Avanti’s bottomline irrespective of healthy demand unless it is offset by volume growth and other factors to an equal extent (which is not impossible but challenging). It’s a good company with good long term potential but current pricing has limited margin of safety.

6 Likes

@learner619

Very good points

anyone when is the concall? and how to attend if they are published?

Sir,

A shrimp farmer unlike a Basmati one (or any other agricultural/horticulture crop) cannot shift to other crop, if a season is bad.

100m*100m ponds are dug out, and huge amount of earth is removed which has substantial costs. If a season or two goes bad, then also there is no going back.

What usually happens is farmers may go for lesser stocking density and possibly early harvesting in face of falling prices.

4 Likes

He cannot grow rice, there are other seafood products he can breed such as fish…either way if shrimp is not remunerative he will not breed it. Fact remains that because you have had 3-4 good years so everyone has jumped into shrimp, supply has gone up and prices are going down. One can debate specifics to any extent but aquaculture is not some IT/ FMCG industry to be immune to basic demand-supply mechanics…

Would again reiterate Avanti’s feed business is less susceptible to this than the shrimp export business.

1 Like

I am a relatively new investor in Avanti, around 600 range. What are the views of the seniors on Q4 results?

Overall looks like the stock is getting battered since the split announcement, but the fundamentals themselves of investing in the company and the promoter haven’t changed.

1 Like

Both earnings and profits dipped in Q4 even though revenue increased by 24%:

P.S: Not much information is available in the article

3 Likes