Have received few messages from members asking for my views on Avanti and underlying business/recent decline in stock price. Hence, I am writing a common message in this thread. These are my personal views based on various news articles and press reports I came across. I may be wrong in my assessment and this is not a stock recommendation. Pls do your own due diligence before making any buy/sell decision.

Shrimp prices are going down and raw material prices for shrimp feed are going up- I read some where that shrimp prices are coming down owing to extreme weather conditions in US. Now, as per various news reports, all the companies have reduced shrimp procurement prices from farmers and increased shrimp feed prices. This in my opinion would partly mitigate the drop in profit margins. Here is where, in my opinion, market leaders like Avanti will score over other smaller and unorganised players in feed business. In such extreme business operating conditions, farmers would generally look for lower operating costs and ways to arrest drop in yields on their investments. Avanti, in a way is able to fulfill this need with a higher FCR. During my interaction with farmers last year, i realised some of them are well prepared for these adverse business operating conditions. They have a medium to long term view of making good returns on their investments and they very well account for these off periods (great learning for me personally after that interaction, to have a firm view on investments over a 3-5 year period and not get perturbed with short term price movements). They were very clear that, shrimp business has provided them with good returns over many years and they are not going to stop shrimp farming owing to one off bad season!

In my opinion, Growth vectors for Avanti over next 3-5 years are as follows:

a) expansion of US market and in turn higher consumption of shrimp across globe. In the last AGM of Avanti, Mr Inder Kumar did mention that Indian market shrimp consumption is at nascent stage currently and may provide an opportunity in future.

b) rise in Chinese imports and entering new markets like Japan

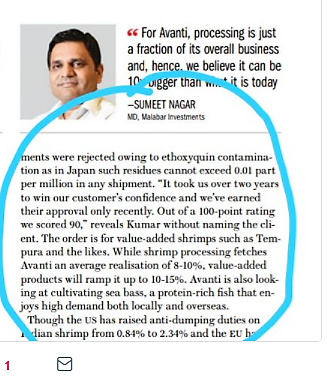

c) rise in domestic market share in feed category and increase in contribution from processed shrimp.

d) recent outlook article spells out few details on how Avanti is trying to entrench its position in some of the key markets like US by vertical integration with companies like Chicken of Sea (Thai Union group company) etc

Above all, I am very confident about Mr Inder Kumar and his astute capital allocation skills. He remains very closely connected to the customer to understand their needs and in turn create a win-win situation for all the stakeholders.

Few risks (which may not be all inclusive) like adverse climatic conditions, continuous rise in raw material prices and low demand for shrimp /low price etc may bring down the margins from 15% (as per Q3 18). In the current scenario, I presume margins would be lower in Q4 18/ subsequent quarters (till raw material prices cool down a bit) and may be market is factoring in the same to bring down the stock price of late. I personally do not have any views/opinion on short term price movement in future. But, as per my estimates, Avanti would provide good returns to investors in next 3-5 years.

We should also bear in mind that, such adverse operating conditions were prevalent in 2012/13, 2008/09, but Avanti continued to deliver strong operating performance year on year.

Will try and do some scuttlebutt to assess the actual situation on the ground and provide feedback to the forum in the coming weeks.