Good for bringing this to notice. Perhaps we can try studying some of these names and see how big they are and what kind of growth and margins do they enjoy.

As TUF has a 25% stake in Avanti and TUF being a world leader in RTE segment, I was feeling that it should be a win-win arrangement.

Driven by a historical shift in food production with farmed fish surpassing global beef production for the first time in modern history, Cargill announced it has formed a joint venture with Naturisa to build a USD $30 million shrimp feed facility near Guayaquil, Ecuador.The transaction involves the construction of a new world-class shrimp feed mill that will produce 130,000 metric tons annually and employ 260 people when the facility is fully operational in 2017.

This 130,000 tpa faciltiy will be operational in 2017. Avanti says its 110,000 tpa faciltiy will be operational in mid-2016. Both starting at the same time. What explains the difference?

ATTN: Those local to Andhra and having friends/relatives/family in Nellore, Ongole, Bhimavaram, Kovvur

As we understand Bhimavaram is the nerve centre of Shrimp Processing. We need contacts here asap, to understand the Processing Industry dynamics better - players, labour situation/availability, scale-up, antibiotics, and the like. We have some workable contacts in Nellore, Ongole.

Anyone having useful contacts in Kovvur, Nellore, Ongole also welcome to put in their wholehearted efforts. Please do your bit to set us up nicely - to extract the real insights into the business - so we can quiz the evolving situation properly

[Please feel free to butt in and correct if there are other locations/centres we should better be concentrating on]

Thanks to abundant availability of labor n owner / labour imlyying absence of labor exploitataion obusiness model India shud have an edge over SE Asian nations for Shrimp industry.

Andhra Pradesh’s shrimp farmers left in lurch by price slump, high mortalities

The battle between buyers and sellers is intensifying and the expected demand from US is not coming. Would be interesting to see the impact of lower prices on Avanti in next few quarters as now they are in a much stronger position (due to higher operating Cash flows) to face the slowdown (whenever it comes).

Some interesting insights from the report. The feed prices has increased by almost 36%(Rs 55 to Rs 75) while shrimp price has come down by almost 28% (from 510 to 370). So it would be interesting to see the volume growth incase of Avanti feeds in this and next quarter because even if they are able to grow at 20-25%,this would be much more significant than 35-40% growth last year as the industry is facing headwinds this year. This would also demonstrate Avanti’s ability to increase market share (and will through some light on potential market size) and even pricing power (in so called commodities business)

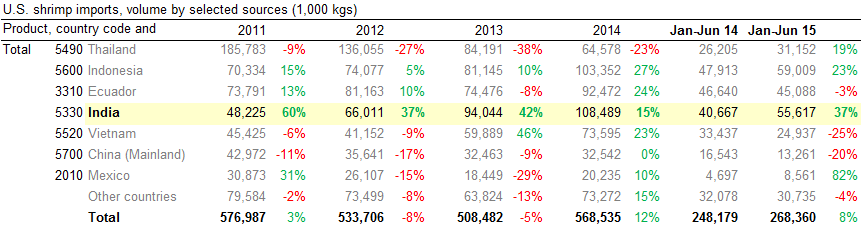

US volumes from India up 36% in volume terms but average price down by 21%

This information combined with the previous news of feed price increase by 36% could actually mean that way too optimistic prediction by management for sales/profit target for next 2 years may not be totally out of line

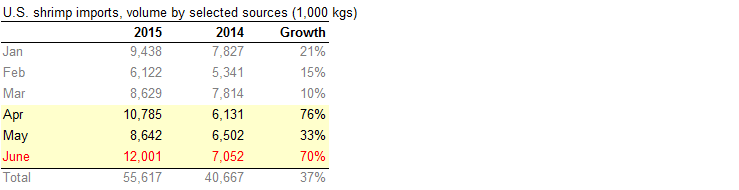

Shrimp import volumes into the United States are up 8% to 268,402 metric tons for the first half of the year, from 248,236t last year, National Marine Fisheries Service (NMFS) data show.

The value, meanwhile, went down by a considerable 14.7%, from $3.05 billion last year to $2.6 bn this year.This equates to an average price decrease of 21%, from $12.28/kilo last year to $9.68/kilo this year.

In June alone, volumes were 8,531t, down 6.8% from last year’s 9,118t. As for value, it was $59.5m, down 27% from last year’s $81.9m.

Those from India increased from 40,666t last year to 55,617t this year;

Also looks like Andhra govt has started seriously looking at solving the recent problems emerging in aquaculture in the state

There is vast potential to increase revenues, for which there is a need for all aqua farmers to fall in line and follow guidelines. From our side, we are focusing on addressing long-pending problems including the licensing system,” he added. He said he was personally interacting with farmers in coastal districts to garner information about ground realities.

“The government is ready to allocate funds to this sector. We are on the job of chalking out a comprehensive plan to make optimum use of the resources available,” he added. East Godavari District Collector H. Arun Kumar said there was huge potential for development of fisheries in the district, and that plans were afoot to simplify norms to accord permission for converting agriculture lands for aquaculture purposes.

This has already gone from 5% of my portfolio allocation to 8-9%.

Reminded of BM’s quote - “No position is too small for a stock that is going down and no position is too big for a stock that is going up”. Had no self-confidence to place a big bet due to borrowed conviction! sigh…

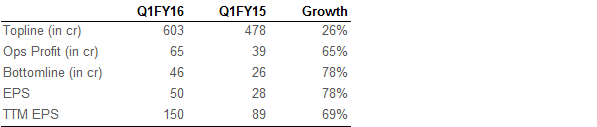

Results are very good…Revenues have gone up, however exports revenue has gone down. I will seek advise from others if this is something to worry about.Generally exports results in better margins - had exports been better, would the bottom line been more better?

Great results from avanti. I think the co is on track to achieve the guidance (or if not then reach very close to it) set by Indra Kumar.

It also goes to show that following unnecessary news headlines takes one nowhere.

Its a good idea to do scuttlebutt and keep abreast of all news but then one has to have the ability to analyse the news and make sense of what is important and what is not.

In the past couple of months I have seen a lot of hue and cry over the prices of shrimp, prospects of the industry being affected by a variety of factors and what not. While this could have been important it could have shaken the confidence of investors who might have invested on borrowed conviction and they might have sold out in a hurry to lock paper profits into actual profits.

This thread is a great learning on what to ignore and what not.

Not sure if this qualifies as skuttlebutt, but I did get a note from Vizak today:

"Yesterday I had a bunch of boys and girls who came in for dinner at 11pm.I just had a conversation with them. This is what I found out. They were from Araku a nearby hill station at vizag. They were all working for a prawn breeding factory at Vijayawada. They were total of 300 working there from Araku And their salary starts from 15000 to 20000.With accommodation and food provided by the management. They were more then happy to work there. "

Guys, stop following useless headlines and getting into the absolute minute details.

The facts are simple, Ocean produce is falling alarmingly and aquaculture is the FUTURE. Its a sunrise sector…obviously there will be ups and downs but the long term trend of shrimp demand and prices will be UP and UP and UP’er.

Cheers to fellow shareholders.

*Celebrating by eating some nice Rawa Prawns today and helping keep up the demand! lol.

This is how perception changes and max wealth is created.

Avanti has huge brands in its feed business,they are farmers no 1 choice,its working on negative working capital,has great distribution reach in every nook and corner and which is ever increasing to a newer areas.

To to pit opp size will remain huge for next several years and business is v scalable.

As they invest in business where institutions are going to invest not where they are already invested.Avanti will now become top choice in coming years of several FIIs/MFs/HNI

Note some like Malabar India Fund,a kotak group’s Pinebridge, Premier Investment funds,SLG International Opp ,Kothari Pioneer Motilal Oswal are already invested.More are going to come

Isnt its feed business akin to a FMCG business?if so what PE will you assign to it?