@rajpanda.Search for shrimp feed word in AR gives below lines from latest AR

Page 9 , under Summary of Operations & State of Company’s affairs

For the fifth consecutive year there was overall increase in the shrimp culture both in terms of water spread

area and stocking density, mainly because of success of Vannamei shrimp culture. Your directors are glad to

inform that your Company’s Shrimp Feed sales grew by 56% in quantitative terms. Your Company’s high

quality of shrimp feed and technical support to the farmers by educating them with best culture practices has

made our feed one of the most preferred feed by the farmers. The year 2014-15 ended with shrimp feed sales at 2,33,489 MT, an increase of 83,598 MT as compared to previous financial year .

Page 18,PRINCIPAL BUSINESS ACTIVITIES OF THE COMPANY

S.No. Name and Descrption of main Products/Services NIC Code of the % of total turnover

Product/Service of the Company

- Shrimp Feed 15339 84.83

- Processed Shrimp 15129 15.03

III PARTICULARS

Page 64, Plant locations:

Shrimp Feed Plant – I, III & Wheat Flour Plant

D. No.15-11-24, Kovvur – 534 350.

West Godavari District. Andhra Pradesh

Shrimp Feed Plant – II

Vemuluru, Kovvur – 534 350.

West Godavari District, Andhra Pradesh.

Shrimp Feed Plant

Block No.498/1 & 501, Pardi-Nashik Road, Balda Village

Pardi Taluk, Valsad Dist. Gujarat – 396 125. India

Page 76, Under Strengths

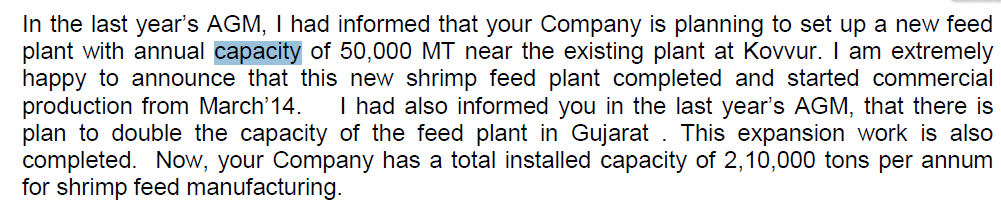

Presently company’s shrimp feed plants are operating at 100% capacity utilization. In view of future increase

in growth of shrimp culture, it is planned to set up shrimp feed manufacturing plant with 1,10,000 MT per

annum capacity in Andhra Pradesh. Company is searching for suitable land for the purpose

When and how much new capacity gets added and utilized? will reveal the future unfolding of Avanti story atleast for there ~85% of core business currently.

Also, refer to earlier point put-up by Hitesh in June,2015 regarding 2,85,000 MT current capacity