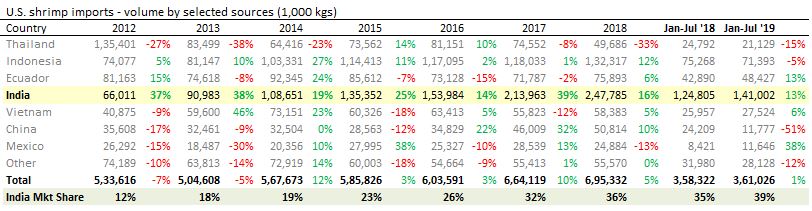

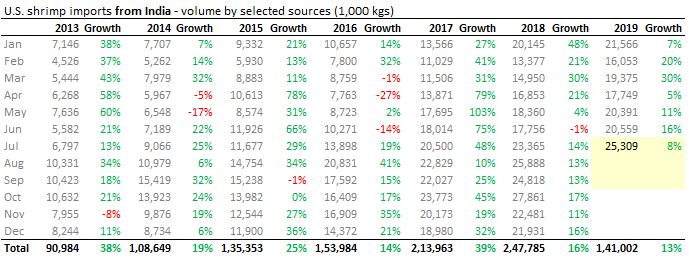

Some data to chew. Shrimp export to USA has been green. India is still gaining market share. Strong is getting stronger.

Have greyed out high margin Fy18 quarters (aberration) in the chart below. This is to cut noise. Avanti now has normalized margin in base data. In fact, Q2Fy19 seems below normal; depressed from top-line and bottom-line perspective. Historically Q1 and Q2 Fy are Avanti’s best quarters (seasonal). Q2Fy20 will have benefit of relatively low base for YoY comparison. Going forward Avanti’s financial performance will be largely dependent on its volume growth - as long as there is no sharp RM/shrimp price movement volatility hereafter.

Avanti continues to be high quality cash generating machine. Co has grown without debt and continue to do so. Co has a problem - problem of where to deploy cash - a good problem to have! Co continues to gain market share in feeds; no sign of tiredness. Farmers continue to trust and prefer co’s feed for better Feed Conversion Ratio (FCR) and Average Daily Growth measurable benefits.

Mix of remunerative farm gate prices and no deficient rainfall this year should bring back farmers. Better days ahead. Seems stock price is not factoring positives currently.

Enough pessimism. Go Avanti!

Disc: Re-entered recently