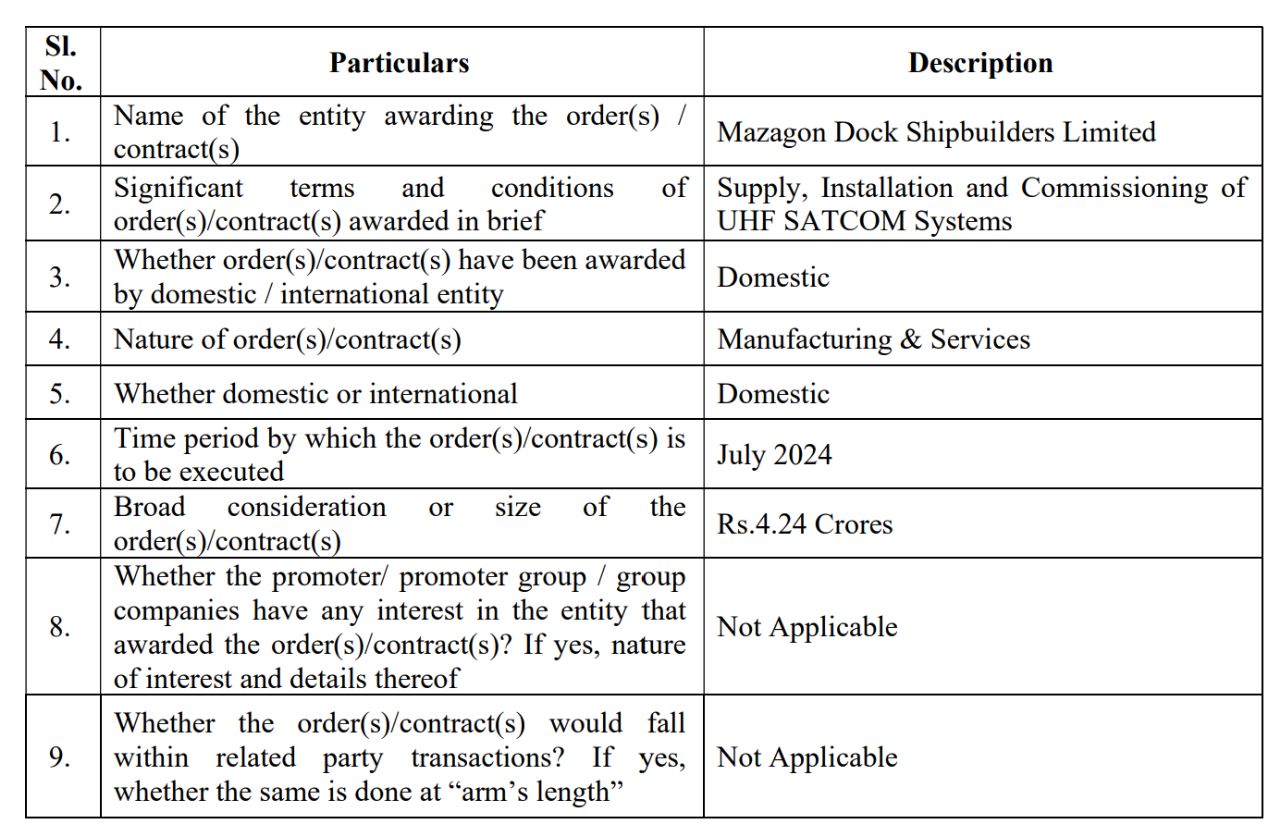

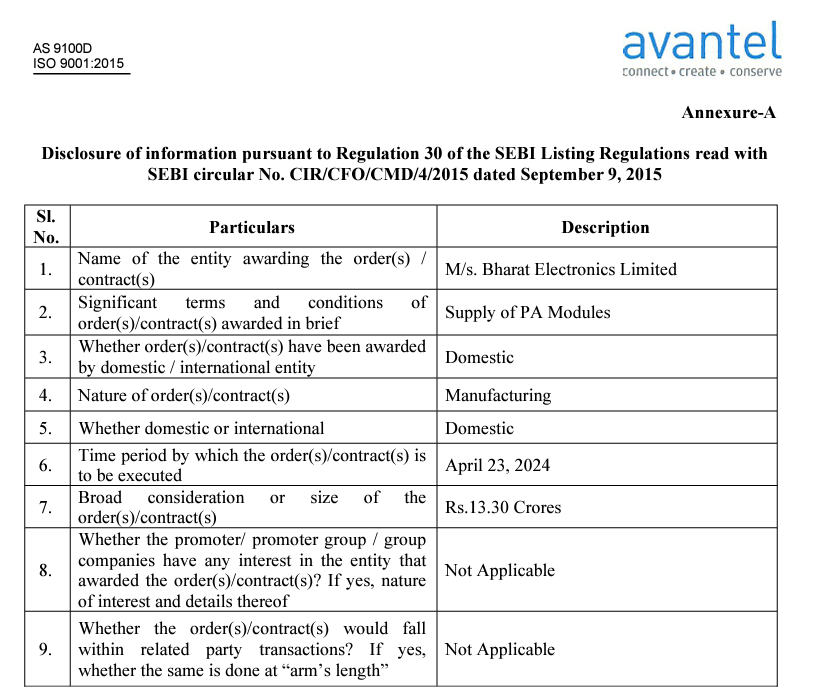

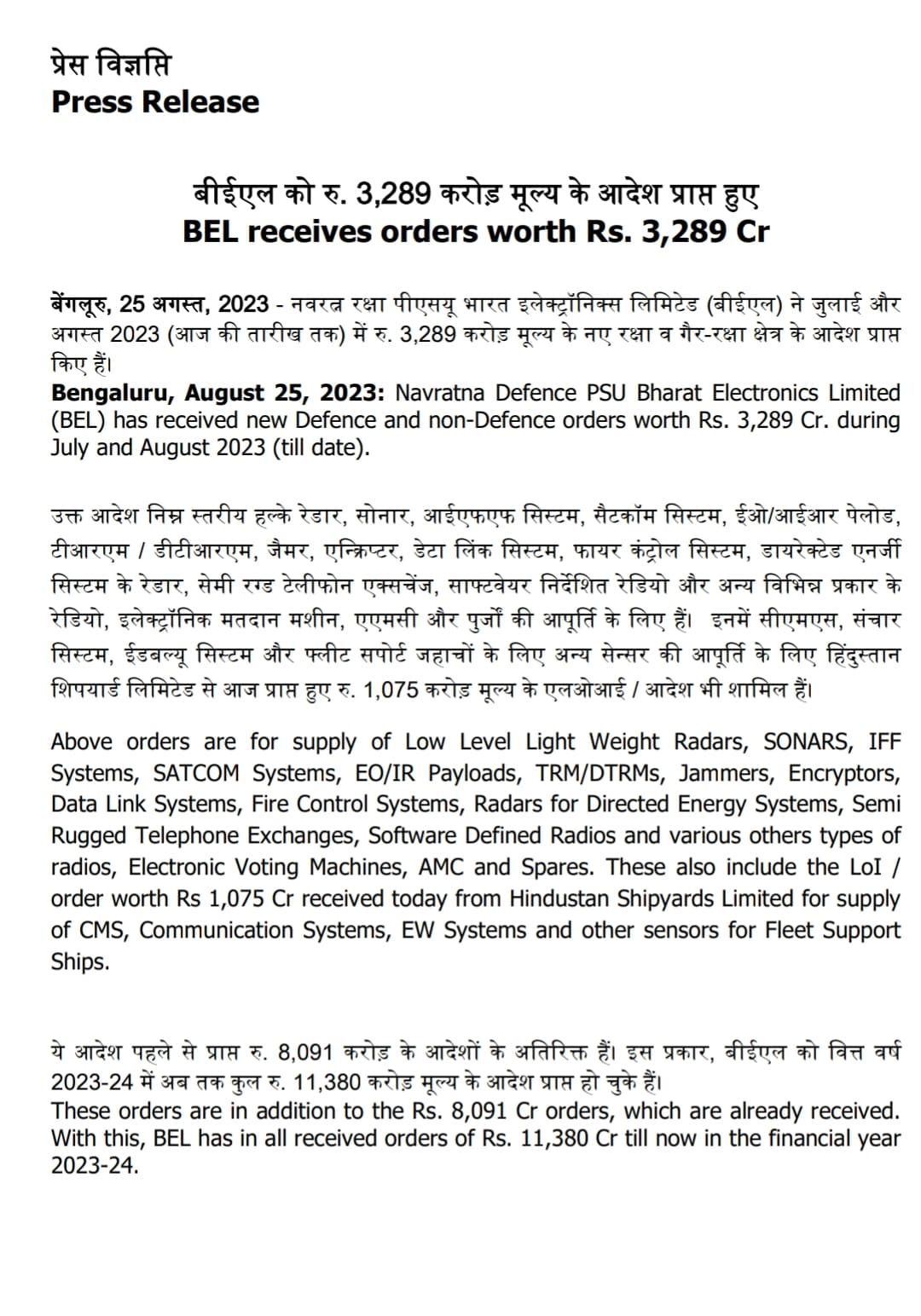

Some part of this order for radio communication is likely to flow to Avantel.

5 Likes

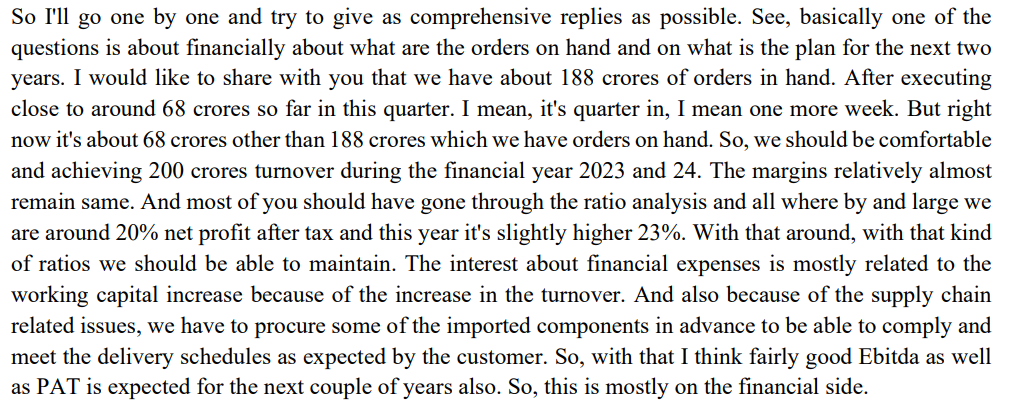

AGM transcript is out

11 Likes

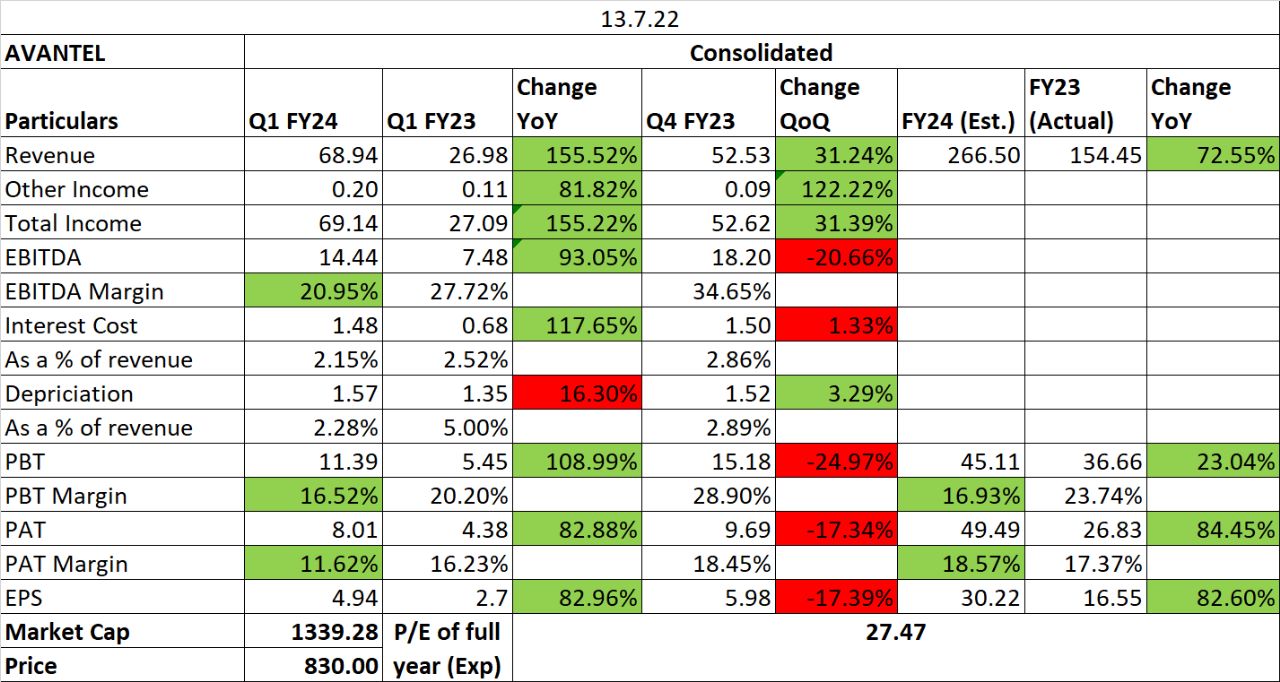

Results for June Quater:

July 13 - Avantel Ltd AVAN.BO :

-

JUNE-QUARTER CONSOL NET PROFIT 80.1 MILLION RUPEES VERSUS

43.8

MILLION RUPEES -

JUNE-QUARTER CONSOL REVENUE FROM OPERATIONS 689.5 MILLION

RUPEES

VERSUS 269.9 MILLION RUPEES

1 Like

1 Like

Q1 24 nos are inline with mgmt commentary in AGM of Order book 68cr rev in Q1 and 188 cr for rest of year.

Q1 nos - Gross margins have been maintained . EBDITA margins should be seen with respect to inventory built up(15.5 cr reported in Q1) , this is likely for two contracts delivery - Lockheed and L&T (Railways) - both of them are getting completed in Q2. This inventory should ideally get consumed in Q2.

Per above H1 itself is 130 cr revenue, last whole year was 155 cr ), which brings to the question that what happens in h2 which traditionally has been more stronger for Avantel/peer groups.

With current runrate and solid Q1 start, a high probability that mgmt does deliver 250 cr+ revenue and NPM at 20% i.e. 50 cr. Future order book build up stays a key watch out (post Q1 mgmt has 188 cr but mkt wd like to see some wins in near future inline with most peers reporting), its a in favor sector and Avantel has lot of room to grow given its tiny size currently(supported by capability)

note above assumptions could be off and actuals may go in either direction. Kindly apply your own discretion.

D - Invested

17 Likes

I would add here that with future plans of defence mfg in India all Satcom orders of Navy are most likely going to go to Avantel. The recent run up in ship building stocks is a sign of awaiting orders.

7 Likes

I have assumed the same YOY growth rate for all quarter. I checked my formulas and no.s but not sure why is it like that. Well, its just an estimate. I can be completely wrong.

Avantel core business has found robust footing. I hope to see sales improving in the near future.

I would be more interested in Imeds global picking pace. A new high growth segment turning profitable should be good news for shareholders.

2 Likes

I wouldn’t count too much on it. There seems to be a lot of competition in this area. I also suspect that it takes time to bring in acceptability for the products. But it is definitely an area that suits the capability available at Avantel.

Can someone help me understand this? While large no of orders and executions gets talked about, the ticket size for each unit appears very low considering 154 cr topline for FY23. Will the growth be driven by volumes in this case? If that is the case, it means they need to invest more and more in R&D to increase the application of their offerings?

MOA with department of meteorology

1 Like

Sept 13 - Avantel Ltd AVAN.BO :

- COMPANY HAS RECEIVED A SUPPLY ORDER WORTH 70.3 MILLION

RUPEES

The EPFO payroll data shows decent jump in employees since Jun 2023.

Payment Details Avantel.xlsx (15.3 KB)

Source- EPFO website

3 Likes

Bhai - how do we get these details from epfo site?

4 Likes

@vivek_17 - Thank You. Very useful