I am sorry but I could not find any avantel reference in the article.

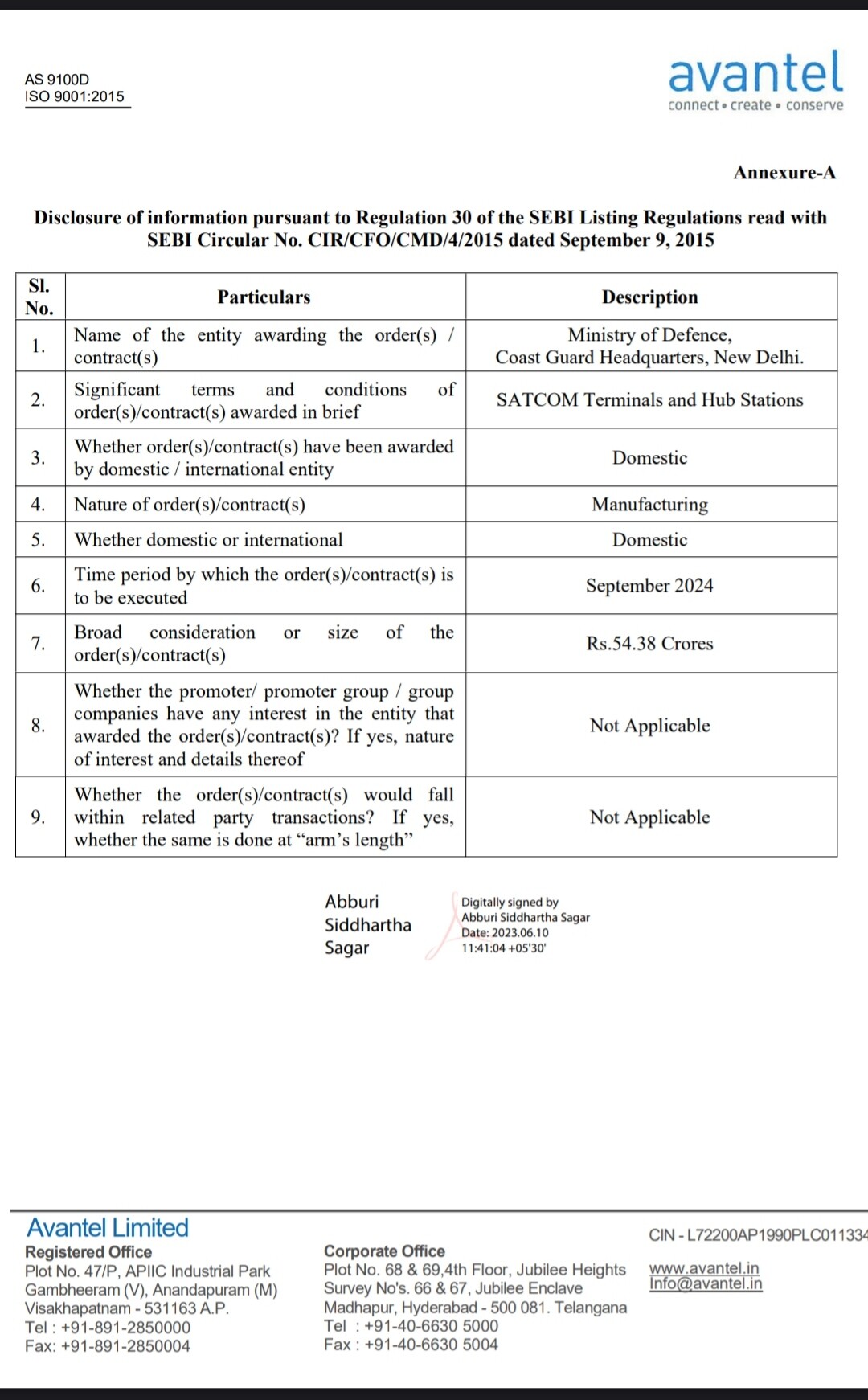

There is no AVANTEL reference, i was correlating on how AVANTEL has disclosed its entry into medical devices market but MOTHERSON is doing it under the hood

Profit growth, sales growth, RoE etc are all looking great. What would be the right PE benchmark for Avantel? Its median PE is too low and it deserved some PE re-rating but the Industry PE being shown on Screener is 47.5 and on Kite it is 25. Similarly for P/B or Price to Sales. What could give a sense of reversion-to-mean vs continued bull run?

1 Like

Hi All,

Since Avantel operates in a very niche area with limited set of customers (GoI, Defence organizations, etc), how would the company grow further? Any insights?

Disclosure: Have a tracking position

It could get acquired by companies operating on that front.

1 Like

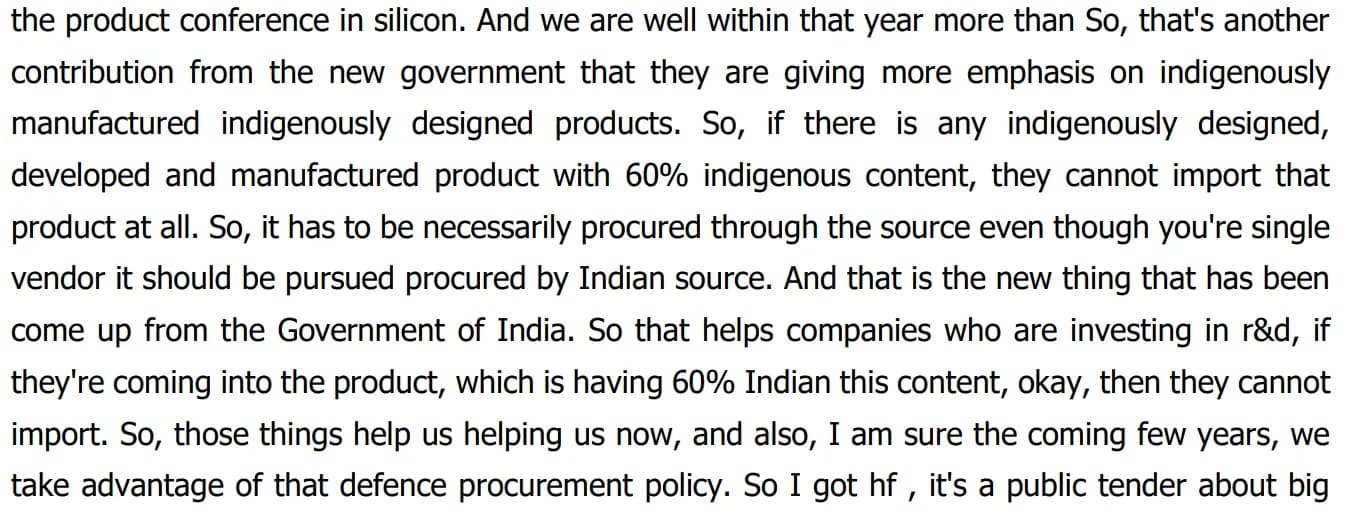

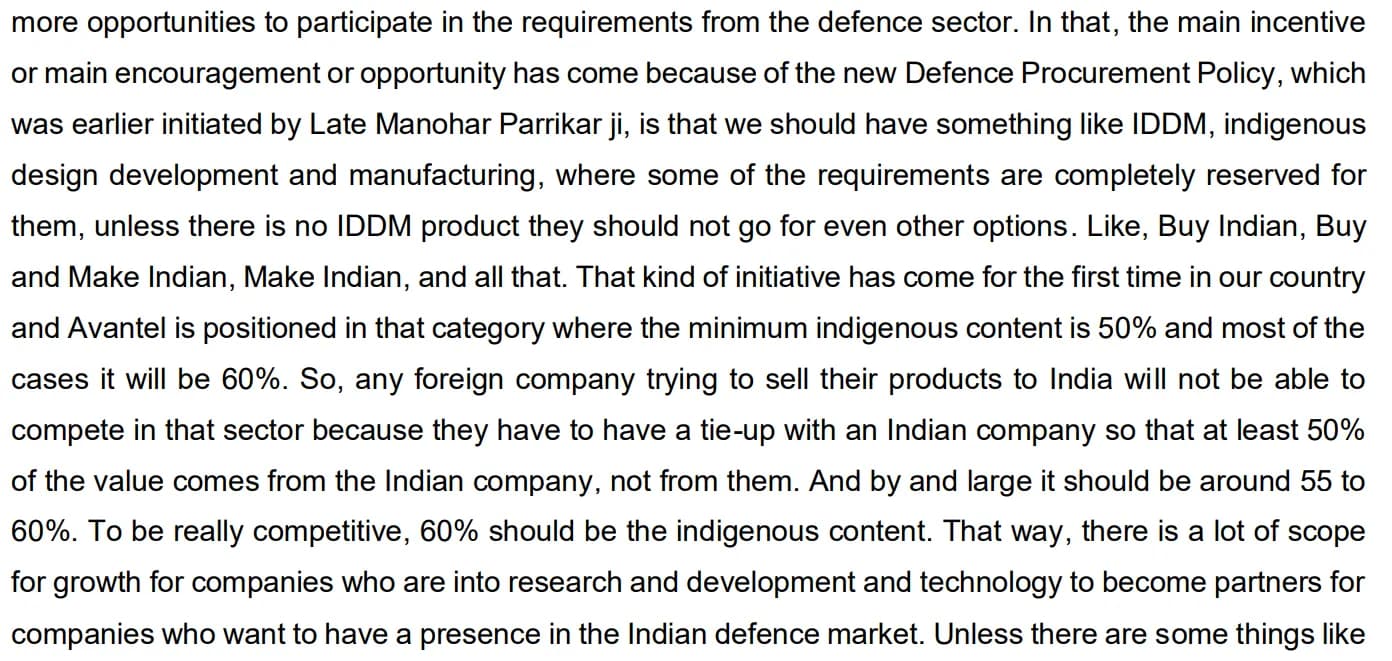

Given that there is lot of “Made in India” focus in Defence industry which will lead to huge business opportunities for the company in future, isn’t it prudent for them to aggressively expand in their core defence business and expand capacities? rather than venturing into an unrelated field - medical devices?

It has niche and unique defence tech which it can utilise to become a major player. Need to understand how aggressive and growth oriented the promoters are?

4 Likes

The company is into electronic communication and satellite communication business mostly for defence sector.

Electronic communication for the military is replaced as per technology advancements.

Software Defined Radios being the latest has already been developed by Avantel. RFP as floated by MoD can be accessed here. Not sure as to whether Avantel will apply directly or through BEL.

Redirect Notice of now

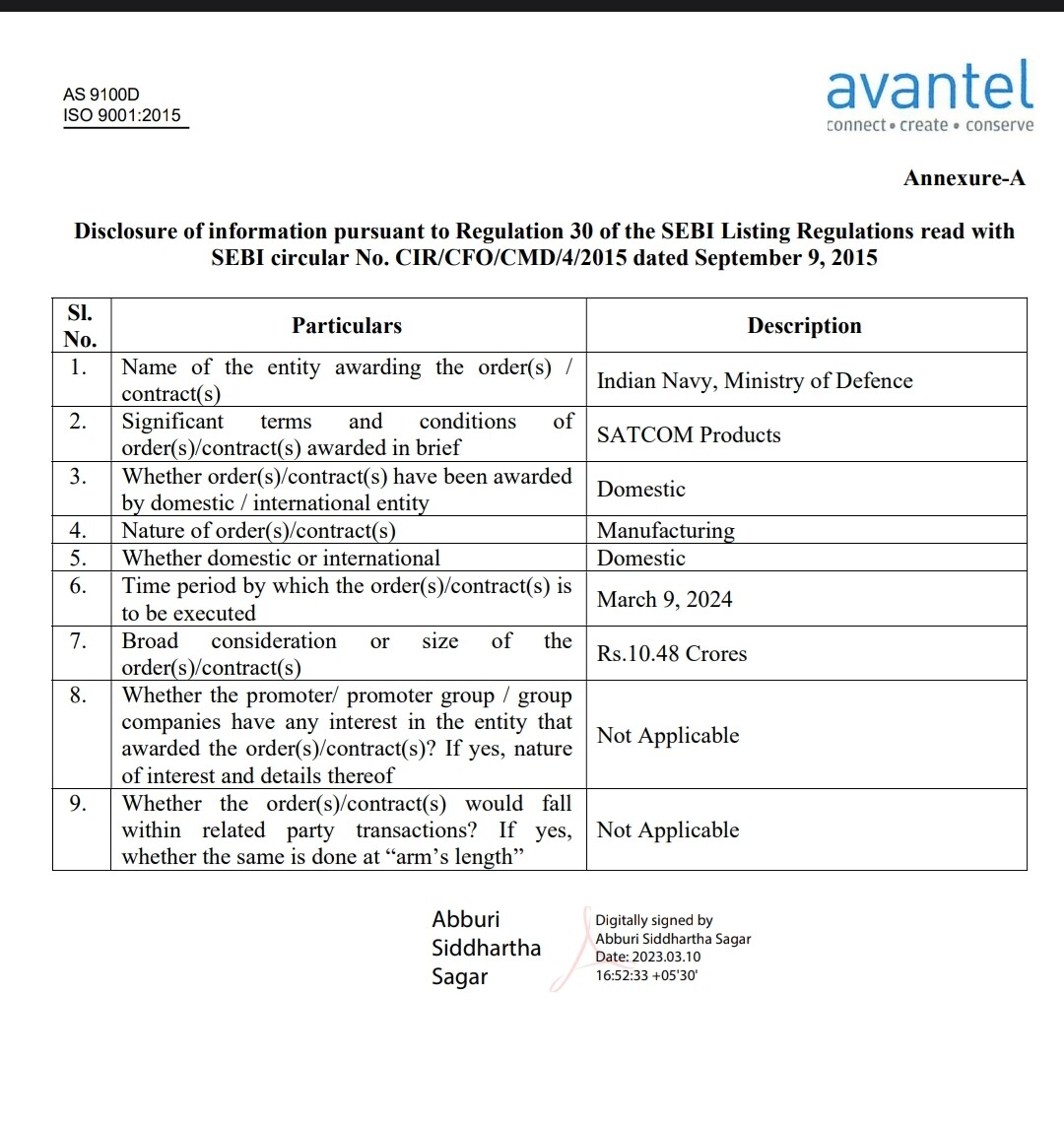

It recently received an order for satcom products.

The fact that the company is trusted by someone like Lockheed Martin speaks volumes of its quality and execution.

Defence manufacturing for use by Indian forces as well as push for the defence exports and curbs on imports puts the company in a sweet spot.

Satcom is likely to be a high growth and niche field.

The global satellite communication market reached a value of nearly $53,083.8 million in 2022, having grown at a compound annual growth rate (CAGR) of 6.5% since 2017. The market is expected to grow from $53,083.8 million in 2022 to $83,680.3 million in 2027 at a rate of 9.5%. The market is then expected to grow at a CAGR of 11.4% from 2027 and reach $143,872.3 million in 2032. (Source- https://www.globenewswire.com/news-release/2023/04/03/2639364/28124/en/Satellite-Communication-Global-Market-Report-2023-Increasing-Investment-in-Low-Earth-Orbit-Satellites-Robust-Government-Support-Growing-Demand-for-Telecommunication-Drives-Growth.html)

Clarity on details of satcom policy are still awaited. FDI announcement is likely.

Disclaimer - Invested

10 Likes

while company has delivered a fantastic Q4 and FY 23 - story might be just starting

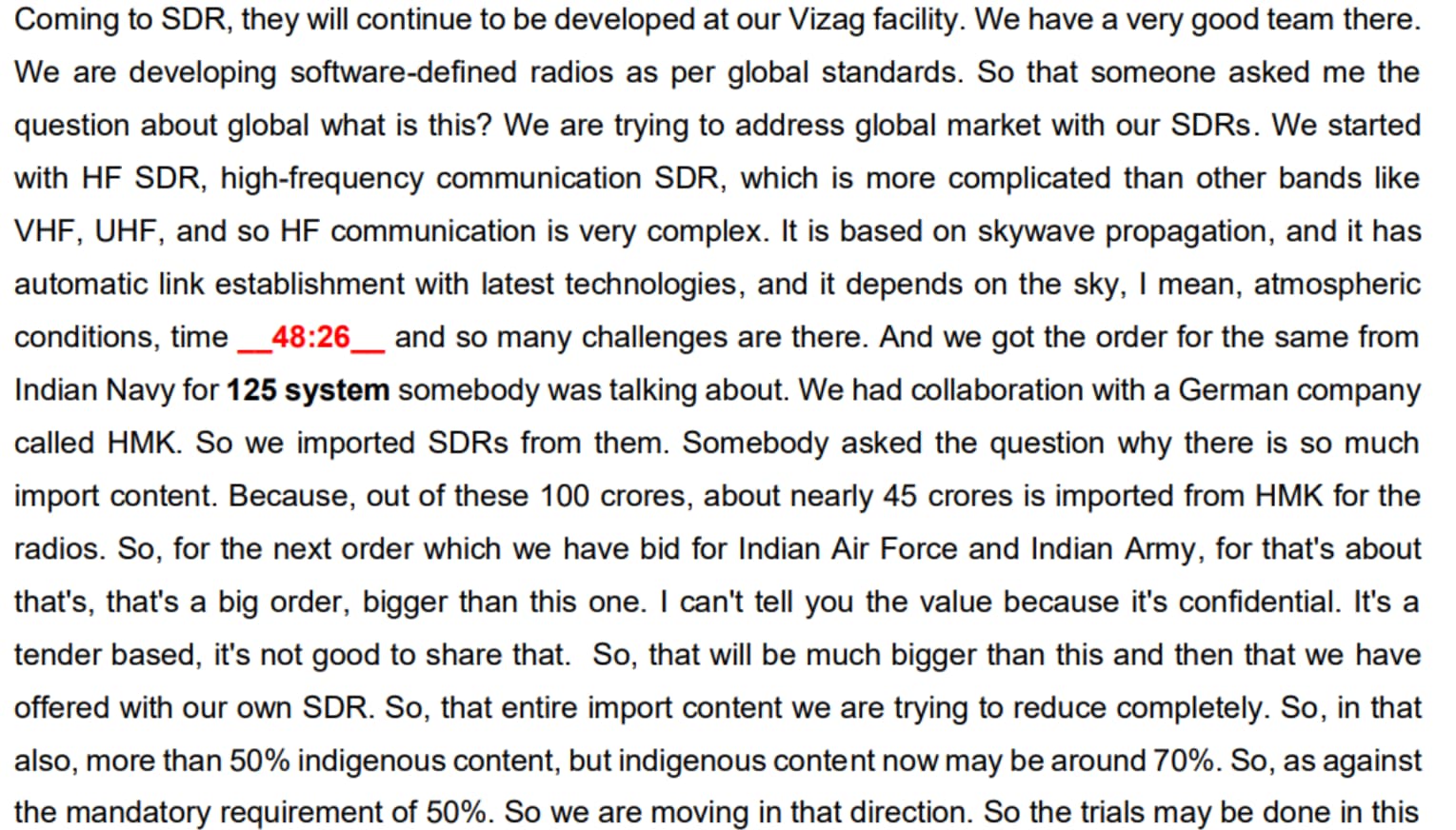

Here is the relevant snippet from last AGM on SDR capability and pricing (that time they had partner and had to import) -

Order size as posted in rfp link by vivek is 7X+ from the last order size - possibly this could be the large bid that Mr Abburi has mentioned in AGM per above screenshot -

FY 24 could have lot of additional triggers for company in terms of recently announced large capex( accruals based), mega orders like above if won(given mandated local content reqmt in tender Avantel will likely have a lion share) and can take co to different orbit, medical equipment subsidiary ramp up etc.

comments from folks tracking co and those who attended AGM can throw further insights

Edit - We can reverse engineer potential Bid size from here ![]() as EMD is disclosed in tender - here

as EMD is disclosed in tender - here

would be great if anyone tracking or good at finding tender status - share with all

D : Invested

18 Likes

Eagerly waiting for their Annual report and the AGM that would provide more insights about the future prospects of the company.

Disc - Invested

1 Like

Sharing some work I have done on Avantel.

Avantel Ltd is into design, development and manufacturing of satellite communication, radar systems and electronics for defense and aerospace industries.

One of their key offerings is high frequency (HF) software defined radio (SDR), for which they have a collaboration with Hagenuk Marinekommunication (HMK).

Their key clients include Boeing, Lockheed Martin, Indian Navy, Bharat Electronics etc.

Avantel was founded in the early 1990s by Dr A Vidyasagar (present chairman & managing director), who, along with his family members, holds a 40% stake in the company.

A discussion of Avantel is incomplete without a discussion of their R&D prowess. As the chairman has explained in past annual meetings-

It takes about three to four years of advanced planning and development…so we invest in R&D, and then come up with a product. And that will be an entry barrier, because we are three to four years ahead of them [competitors] if they want to get into that by the time you have already captured it. So that’s how we survived all these years…whatever we invested three, four years back…have given results today…we should understand that you invested earlier and the returns are coming this year.

Importantly, for most years in the last decade, consistently over 90% of the total R&D spend has been debited to the P&L instead of being capitalised, an indication of conservative accounting.

In the past, during the period from FY14 to FY17, R&D expense as a % of revenue jumped substantially from their standard high-single-digit range to an average of 16% from FY15 to FY17 (excluding the abnormal 45% in FY14). This was primarily directed towards- a) real time train tracking systems (in collaboration with Highness Microelectronics) and b) 1 KW HF power amplifier and antenna tuning unit. As a result, operating margins contracted by 700-800 bps and return on capital employed plummeted.

Sure enough, Avantel received an order worth INR 1.25 billion for train tracking and wrote in its FY21 annual report - “this year, the company has also signed a highest value contract till date with Indian Navy for supply of 125 No’s 1 KW HF Transceivers.”

A demonstration of their R&D is their ability to indigenously develop import substitute products, often in record time periods (e.g., their antenna tuning unit).

The outcome of such R&D is that Avantel is a single source vendor for many of their offerings (90% of revenue comes from unique, differentiated products where they have no competitors).

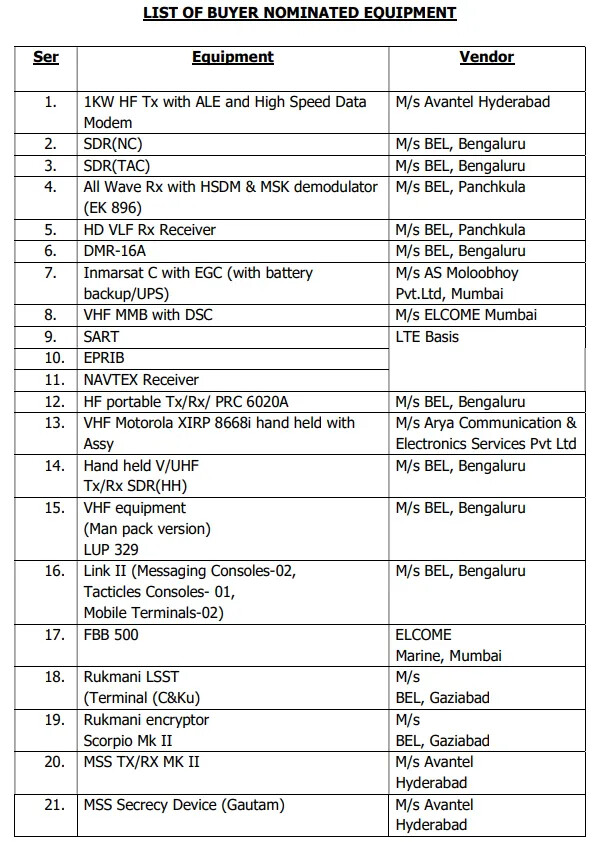

To corroborate this, one can find Avantel mentioned as the sole approved vendor in an RFI by the Indian Navy (see serial numbers 1, 20 and 21 below).

Their R&D capabilities are also validated by the numerous awards they have won. Avantel was named among the top 25 most innovative companies; won 1st prize for excellence in R&D in the MSME category etc. (the list goes on). Regarding attracting talent right out of college, Avantel has tied up with an engineering college (VNRVJIET) and is also one of the bigger recruiters at ANITS.

The Indian government has been proactively working on being self-sufficient and independent in defense, providing strong tailwinds for the sector.

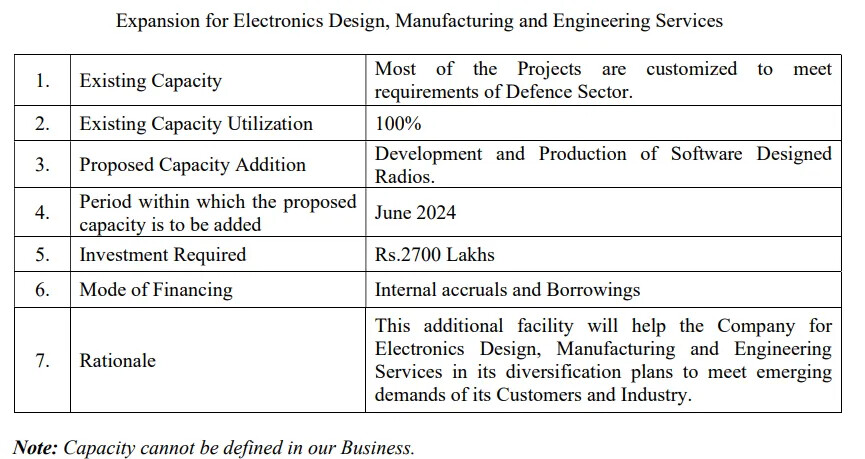

Avantel has also announced capex of INR 27 Crores (INR 270 million), in line with the capex guidance given during the FY22 AGM.

Capex outlook given in FY22 AGM

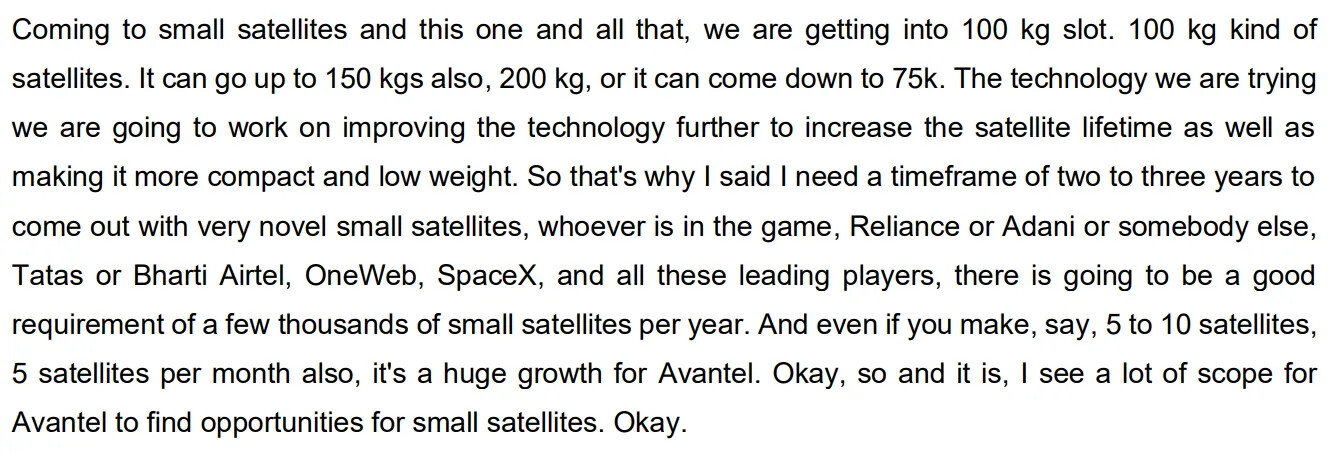

Management commentary on the small satellites opportunity

Here is an excerpt from Ashlee Vance’s biography of Elon Musk, to connect the dots on small satellites-

Some members of the military had already been promoting the idea of giving the armed forces more aggressive space capabilities, or what they called “responsive space.” If a conflict broke out, the military wanted the ability to respond with purpose-built satellites for that mission. This would mean moving away from a model where it takes ten years to build and deploy a satellite for a specific job. Instead, the military desired cheaper, smaller satellites that could be reconfigured through software and sent up on short notice, almost like disposable satellites. “If we could pull that off, it would be really game-changing, ” said Pete Worden, a retired air force general … “It could make our response in space similar to what we do on land, sea and in the air.” [emphasis added]

[image]

Growth opportunity in small satellites

Going forward, Avantel’s growth is expected to be propelled by the aforementioned expansion plans and sector tailwinds as well as plans to venture into new yet adjacent products and segments. Regarding the latter, management has explained that they will “leverage the existing strengths and…find new markets and new applications for the existing products and technologies.” As for specific verticals, management has spoken about plans of entering medical electronics, IoT, cloud computing and nanosatellites.

One of the key monitorables remains the execution and capital allocation on projects outside their core competence, such as medical devices. Their foray into medical devices appears to be a case of unwarranted diversification; management has elaborated that they want to participate in affordable healthcare. They are collaborating with ISRO for ventilators and are in talks with global majors for potential contract manufacturing opportunities. Performance in the medical devices segment has been subpar so far, but management has clarified that they are working on product development and certifications which will take time. On the positive side, the capital deployed in this segment is only INR 2 Crores (INR 20 million), well under 5% of total capital employed. Furthermore, their facility is being set up at the Andhra Pradesh Medtech Zone (AMTZ), a medical technology park with common manufacturing and scientific facilities. Management has commented “they [AMTZ] invested more than 100 crores [INR 1 billion] on test facilities which are made available to the companies there…it is an ideal place to do something in medical electronics.”

Another negative is that receivable days are high at >100 days; though, this is a general trend across all Indian defense companies (an explanation by management is below).

In FY22, the % of total R&D spend recognised as capital expenditure spiked to 34% (a previously unseen level, see below). This is a major question that requires explanation.

Moreover, in the absence of conference calls or investor presentations, tracking progress is possible only through quarterly results, exchange announcements and the annual shareholder meeting.

Currently trying to map out their reported orders to gain better visibility and for tracking. Would be happy to collaborate if anyone is interested.

Disc- invested. No transactions in last few months

16 Likes

| Date of Announcement | Product | Client | Order Size (INR Cr) | Time Frame (To Be Executed By) |

|---|---|---|---|---|

| 10-Mar-23 | Satcom | Indian Navy | 10.48 | 09-Mar-24 |

| 24-Aug-22 | Satcom | Indian Navy | 11.28 | NA |

| 21-Mar-22 | Satcom | Lockheed Martin | Approx 11.1 | NA |

| 14-Mar-22 | RTIS (Locomotive Tracking) Phase 2 | Indian Railways | 125.68 | NA |

| 18-Nov-21 | Satcom | Bharat Electronics | 9 | NA |

Disc- invested

9 Likes

New Medical Device Policy cleared from Cabinet…There is also a mention of the PLI scheme and setting up of manufacturing parks

Will this help Imeds? (Subsidiary of Avantel). Has management guided anything on expansion plans for this in the recent past?

2 Likes

one can check here on approved names as of date

more tracking here

https://pharmaceuticals.gov.in/schemes

Avantel-inmeds doesn’t seem to be in approved candidates yet, though they are likely benefitting in state level scheme (as part of med park) - last AGM notes has some details, though we need to get roadmap clarity

Avantel 2023 AGM announcement is due anytime going by last year trends

5 Likes

AVANTEL AR 2022-23 Notes

Consolidated Net worth of the Company for the Financial Year ended March 31, 2023 is Rs.10748.17 Lakhs as compared to Rs.8142.08 Lakhs for the previous Financial year ended March 31, 2022.

Your Company has successfully completed all the deliveries of the 1 KW HF project of Indian Navy and the installations of HF Radio sets are currently under progress. The RTIS project with Indian Railways is currently under execution and shall be completed by October 2023. We have also designed, developed and supplied 5 Kw HF Transmitter systems which will be an import substitute for Indian Navy requirements. Your Company has successfully completed development of SATCOM System for Multi Utility Helicopters of Lockheed Martin being supplied to Indian Navy.

Future Prospects:

- Keeping in mind the future business prospects, this year your Company has also embarked on development of HF Software Defined Radios (SDRs) with 2G/3G ALE & ECCM Capability and different variants of MSS for submarines.

- Imeds Global Private Limited, subsidiary of Avantel Limited offering innovative medical solutions has commenced its operations from AMTZ, Vizag and the license for manufacture of Surgical Staplers and Removers has been granted. Imeds has also embarked on development of a non-invasive ventilator which is at an advanced stage and developing a patient monitor & syringe pump through Technology Transfer.

- Union Budget also outlays around Rs. 5.93 lakh crores which is 13.18% of the total Budget of 2023-24. Its 13% increase from 2022-23. Modernisation and infrastructural development has been increased by 6.7%. The sustained increase of the capital outlays in the defence budget indicates positive outlook from customer side for new inductions / new purchases by the Defence Forces and offers sufficient market space for your company to forge ahead and expand its footprint in the strategic sector.

- The recent announcement of Union Cabinet approval of the “Indian Space Policy 2023” is a great step in the direction and your Company expects to utilize the emerging opportunities to enhance its SATCOM and Space Technology portfolio. In F.Y. 2023-24, your Company focus would be around development of HF / VHF /UHF SDRs for ship borne as well as land-based platforms and design & development of Air Defence Radar systems for Indian Army.

7 Likes

Can anyone who attended the AGM please share the insights?

While co might give transcript like last year , some key take aways from Avantel AGM - 23rd June

- Order book healthy 188 cr June end( excluding 60 cr+ for current qtr) - Q1 is leanest usually and this might set a good tone for start of year

- SDR is a key opportunity with $300M per year type spends - from 100% import to 35% import(rest indigenous now) for Avantel, expect FY 25 to be step up on offering breadth(band range of SDR) hence ability for higher/all of tender participation - as of now selective players in this space and Avantel feels we are way ahead - SCA complaint SDR, already developed HF

- One large tender(SDR) trials in august for Indian army/airforce - seemed good probability candidate

- Margins 20%+ (NPM) doable and guided for 25% type rev growth CAGR for coming few years(though might do a notch better per past trend and tailwinds, interestingly in opening speech Mr Abburi indicated similar growth like last 2 year to continue)

- med equipment - Inmeds break even in FY 25, some products commercialized (stapler etc) and some in testing

- Capex excluding building 15 cr for this and next year - all through internal accruals, have enough land for expansion

- Radar is space they want to focus more from FY 25 onwards (seems expecting demand side clarity via some tenders)

- Railways - L&T - RTIS - order to be completed by Oct 23, next set of 12K trains (current order was 6K type) could be out by Year end and Avantel stands a good chance

- Lockheed martin order also to be completed by Sept

- Share split announcement soon and NSE listing next year

All in all appears given small base/size and order book visibility + upcoming sizable tenders, they can continue to deliver on similar trajectory growth. Sector tailwinds help further.

D: Invested

20 Likes

Stock split announced. 1 share of FV 10 Rs to be split into 5 shares of FV 2Rs.

1 Like

Going by the tone of management in the latest AR, growth (at least ~25%+) in sales and profit seem certain for the next 2~3 years. Although a 10-bagger in the last 3 Yrs, decent ROE (~30%) and and bullish (ATH) chart make it look like a good investing candidate even now.

But, this represents a classic example where ‘Profit from operations’ is primarily tied up in the Working Capital (60%~70%). Rest of the operating cash flow has gone in to Capex and Taxes, leaving nothing for the shareholders.

Disc: No position.

1 Like

I don’t find AGM transcripts on screener yet. Does the management insinuating about this quarter revenue is going to be around 60 crore? Is that a fair understanding?