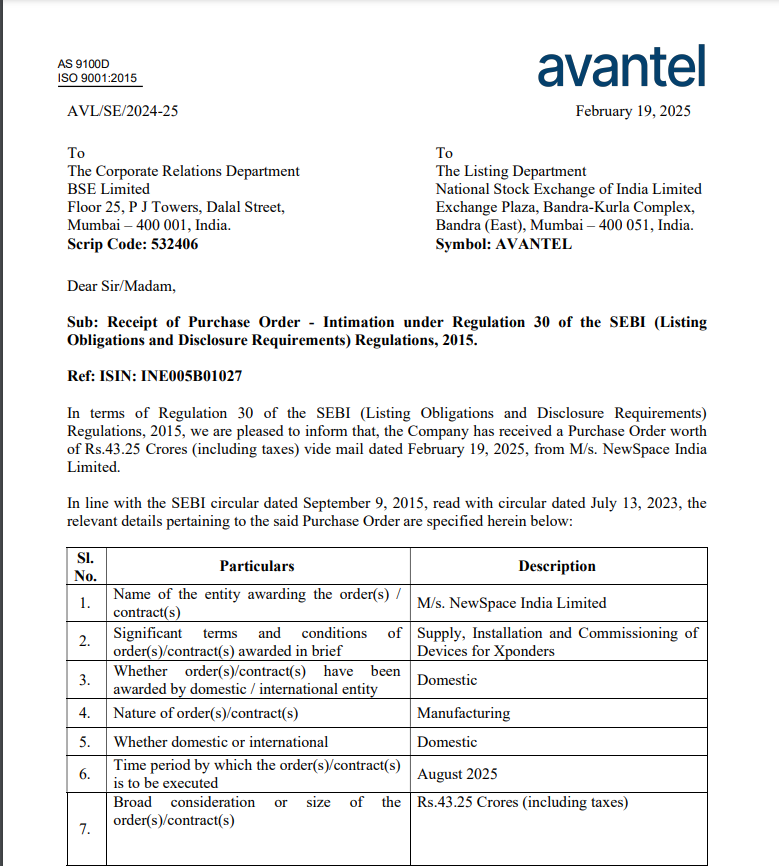

Company has received a purchase order worth of Rs.43.25 Crores from M/s. NewSpace India Limited For Supply, Installation and Commissioning of Devices for Xponders

1 Like

Avantel announced a strategic partnership with Safran aerospace to design, manufacture, and integrate multi-band antennas in India, delivering high-performance, sovereign solutions to support the growing demands of space communications across the region.

5 Likes

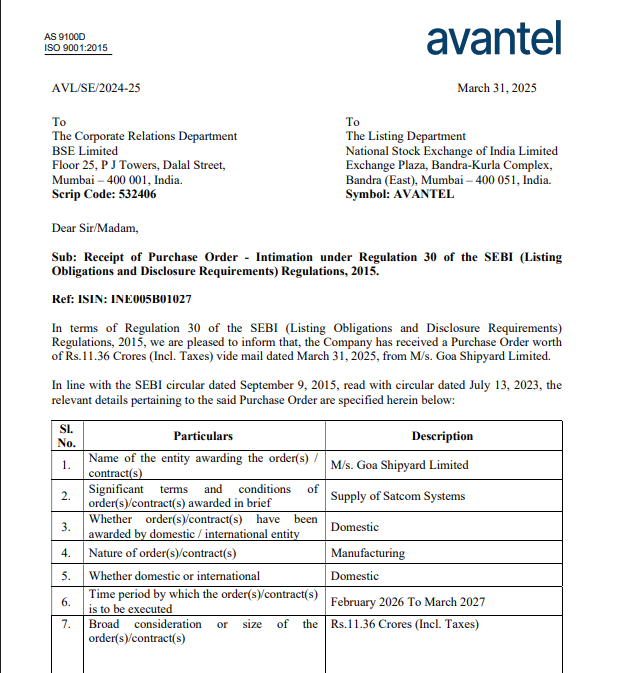

Avantel has received a Purchase Order worth

of Rs.11.36 Crores (Incl. Taxes) from Goa Shipyard Limited for Supply of Satcom Systems

3 Likes

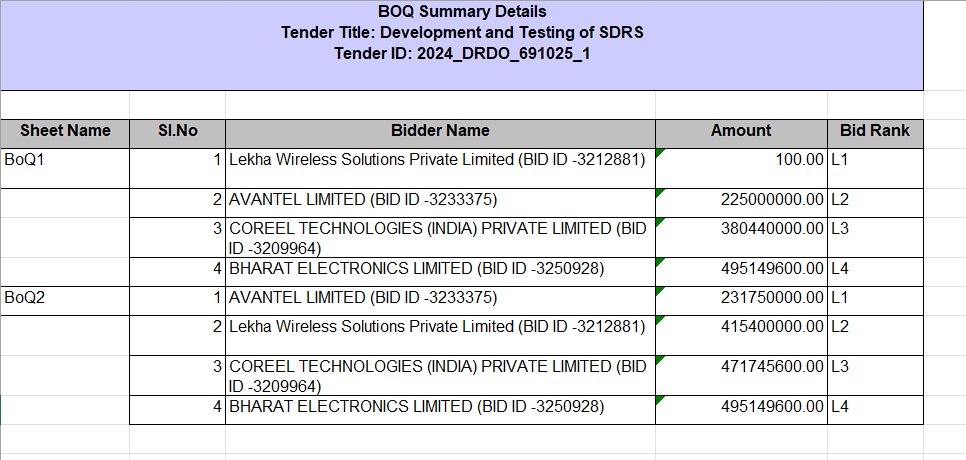

They are likely to win this tender of about 30-50cr form my guess

This is from DRDO for development and testing of SDR

plz note this has been sourced form publicly available info and I can be wrong

Disc- not invested, evaluating

8 Likes

Promoters sold 1,317,013 shares on May 6, 2025. Assuming this is sold at ₹110 per share, total value is around ₹14.5 crores.

This is one day before the rights issue record date, that is, 7 May 2025. What can we infer from this?

1 Like

Can it be said that they raised money for subscriptions of right issue ?

That is a possibility. But why would they do it on the day before record date? That would mean they lose Rights Entitlements (about 10,884 REs).

If they sold it on or after the record date, they would have retained REs and raised money for applying for rights at the same time.

Maybe, this is simply due to market uncertainty as the result of the tension between India and Pakistan.

Not sure yet. It will be interesting to know the change in the shareholding after rights issue.

2 Likes

Is there any news of Avantel getting any new orders after the recent conflict and new defense based orders/procurement kicking in?

@abhinav_sinha so the above SDR order which I posted avantel had the lowest bid of 22cr but some company came at put a bid of 100rs I don’t know why they did that and what would happen to this tender now

second they won a tender from Mazagon Dock Shipbuilders Ltd of about 10.85cr

another 15-20cr of tender for Dual band full motion antenna they have participated of about 10-15cr but lot of competition here almost btw 10-12 vendors

Also their Imeds is doing decent recently they got approval form CDSCO for thier oxygen concentrator. Earlier it was only for the staple

Also I was trying to map their order book but kind of failed

this is based on what number they announce per AGM around 30th of may then add the new orders won and subtract the orders executed so as per that it should be around 200-250cr but lets see

plz note all the info above is public ally available may be exchange notification will come in some time

disc - evaluation

13 Likes

In DRDO design and development contracts, some companies quote as low as Rs 1 (essentially zero) to win the tender if they feel that:

- The product/technology has a large market

- The company will gain immense knowledge while co-developing the product with DRDO

- The company has the resources and willingness to invest its own capital to develop the product

So in this case it seems that Lekha Wireless is the lowest bidder and that they will win the tender.

6 Likes

Can you please guide me to the resource from which you availed this, since I know a friend and he did say that low bidding is allowed in DRDO ?

But wouldn’t such a low bid normally fail the “smell test”, as in, seem too good to be true?

1 Like

It was a two BOQ bid where Lekha Wireless bid 100 Rs strategically for BOQ 1 and overloaded on BOQ 2.

It’s mentioned in BOQ 1 that “Kindly fill details in BoQ2 form only.”

There’s ambiguity here. If rates were to be filled in BOQ 2 only then Avantel stands L1 i guess. Otherwise lekha wireless is L1 and difference between L1 and L2 for BOQ1+BOQ2 is 4.135 Cr

4 Likes

1.Key Growth Drivers

Execution of Large Projects:

Indian Navy: 1 KW & 5 KW HF projects (high power radio communication).

Indian Railways: RTIS (Real Time Train Information Systems) – 6300+ units supplied for locomotive tracking.

Multi Utility Helicopters (Lockheed Martin, USA): MSS (Mobile Satellite Services) for helicopter platforms.

Expansion of Customer Base & High-value Orders:

New Space India Limited (NSIL)/ISRO: Orders for 30,000 MSS terminals.

Defence, Railways, Shipyards, Atomic Energy—frequent new orders.

Turnover & Profit Growth:

Crossed ₹100 crore (FY22), ₹150 crore (FY23), ₹223 crore turnover (FY24: highest since inception).

Profit before tax up 68.9% YoY in FY23.

2. New Revenue Streams

Medical Devices Subsidiary:

Formation of wholly-owned subsidiary Imeds Global Private Limited (FY22).

New manufacturing facility in Andhra Pradesh MedTech Zone (APMTZ), Visakhapatnam.

Products: Surgical staplers/removers, non-invasive ventilator, patient monitor, syringe pump, CPAP, BiPAP, oxygen concentrators (development/commercialization from FY24+).

Targeting indigenous, cost-effective healthcare equipment for growing Indian demand post-pandemic.

Space Technology and Services (Emerging):

Ground Station as a Service (GSAAS) proposal.

SATCOM (Satellite Communication) as a Service using a dedicated satellite—initiative with ISRO/IN-Space.

Investment in a ~70,000 sq ft facility for space technology R&D and manufacturing (Hyderabad, operational in FY25).

- New Products & Innovations

Defence & Strategic Electronics:

1 KW HF Software Defined Radios (SDR), SCA 4.1 architecture (custom for Indian Air Force).

5 KW HF Transmitter—import substitute for Indian Navy.

MSS M-II (Mobile Satellite Services) using Digital Beam Forming, LDPC coding: more reliable high-speed comms for helicopters.

RTIS Terminals for real-time locomotive tracking and automated charting (Indian Railways).

Initiatives in airborne, marine, and multi-band SCA compliant SDRs, Ku-band and new frequency terminals.

Indigenous air defence radar development (for Indian Army, in progress).

Innovation Highlights:

Persistent in-house R&D (recognized by DSIR, Govt. of India).

Technology absorption for wireless, signal processing, embedded systems, and software integration.

Import substitution through indigenous design and manufacturing (DAP 2020 compliance for defence orders).

Advanced wind profiler radar, environmental radiation monitoring, and electronic beamforming for SATCOM.

4. Unique Selling Proposition (USP):

Indigenous, Customized Solutions: Deep focus on “Make in India” and “Atmanirbharta.” Fully in-house conceptualization, design, and manufacturing—catering to highly specialized requirements of Defence and other strategic domains.

Cutting-edge R&D: Recognized in-house R&D lab; ability to swiftly move from concept to execution and respond to customer-specific needs.

Trust & Relationships: Established, deep-rooted ties with Indian Defence, Railways, ISRO, and government bodies—positioned as a trusted partner for sensitive and strategic projects.

- Business Model:

Core Model: Design, manufacture, and supply of wireless/satellite communication equipment, embedded systems, radars, and customized solutions for defence, space, and government.

Revenue from project-based execution and supply contracts.

Focus on sectors with high entry barriers and repeat business.

Service & Support: Includes after-sales, upgrades, and customer support for mission-critical solutions.

Diversification:

Medical devices (via subsidiary)—leveraging electronics and manufacturing expertise in new verticals.

Space/ground station services—potential for recurring service-based revenues.

R&D-Driven Value Addition: In-house development allows rapid innovation, proprietary product development, and sustained competitive advantage.

Summary of Major Initiatives and Transitions:

From FY22 to FY24, Avantel has robustly expanded within its defence/strategic core, broadened into medical devices, and proactively positioned for emerging opportunities in Indian space privatization and service-based models.

New revenue streams and innovation are visible in medical devices (Imeds Global), high-value defence projects, and space technology services.

The USP remains indigenous, high-tech, and customer-specific solutions for strategic sectors, fuelled by R&D and robust government/defence relationships.

The business model is evolving from hardware supply to augmented, service-based, and multi-vertical operations rooted in technology innovation and reliability.

Orderbook growth and orderbook quality remains the key monitorable here to guage growth in the next 2-3 years.

AVANTEL R&D FOCUS AND INNOVATIONS.pdf (114.2 KB)

AVANTEL AGM SUMMARIES.pdf (106.8 KB)

6 Likes

Annual Report for FY25 is out.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/f66c951e-985d-4fc5-a260-b35fea769431.pdf

can anyone study and explain the ESOP accounting of Avantel. They have accounted Rs 14.56 Crs in P&L but just cant understand whether its 100% of value of ESOP expensed in the FY or this is the value of ESOP attributed for this FY.

2 Likes

Here’s a detailed summary of Avantel Ltd.'s growth plans, key opportunity areas, R&D investment, and management’s guidance for FY25 and beyond, based on its FY2025 annual report (dated 31 March 2025):

Growth Plans & Key Growth Products

- Software Defined Radios (SDRs) for Airborne Applications

• Company Statement: “Avantel is confident of developing Software Defined Radios for airborne applications during the current financial year 2025-26 and will be one of the top five companies in the county in the area of Software Defined Radios.”

• Avantel has already developed advanced SDR solutions in HF and UHF bands and is now focused on airborne platforms, targeting major defence communication upgrades. - Ku-Band Electronic Steerable Phased Array Antenna (ESA) for COTM

• A strategic product for ‘Communication On The Move’ (COTM) satellite applications—central for continuous battlefield and mission connectivity.

• The company is investing in R&D for these high-tech phased array antennas. - Wind Profiler Radar

• Used for meteorological and environmental monitoring, especially for satellite launch support.

• Quote: “Our advanced Wind Profiler Radar systems are designed to enhance meteorological assessments and environmental monitoring before launching a satellite.”

• Uses proprietary phased array technology for precise atmospheric profiling. - GSaaS (Ground Station as a Service), VSAT & Satellite AIT Services

• Avantel received authorization from IN-SPACe to establish a commercial satellite ground station service, operational from a new 70,000 sq ft Hyderabad facility (ready by June 2025).

• The company has also received a VSAT license for KU-band voice and data services. - New Manufacturing Facility for Antennas & MIL Standard Connectors

• Setting up a new facility (80,000 sq ft on 9.1 acres in Andhra Pradesh) dedicated to electronics manufacturing for both commercial and defence/aerospace markets.

• Will include capacity for Satellite Earth Station Antenna, high-power HF antennas, and connectors, supported by new SMT lines. - Medical Devices via Subsidiary Imeds Global Private Ltd.

• Focus on indigenously-developed products in surgical and respiratory domains.

• Established a 25,000 sq ft facility at AMTZ, Visakhapatnam, with cleanroom and assembly/testing capabilities.

Opportunity Size

• Defence Budget Tailwinds: India’s 2025 Union Budget allocates ₹6,81,210 Cr (≈$78.6B) to defence, up 9.5% YoY; 75% (~₹1,35,000 Cr or ~$15.6B) earmarked for the domestic industry, boosting opportunities for indigenous players like Avantel.

• R&D Budget: The R&D allocation for defence is ₹26,816.82 Cr with ₹3,730 Cr or $430M reserved for private industry/startups/academia.

• Government Vision: Increased spending and policies (Atmanirbhar Bharat, iDEX/ADITI schemes) to promote domestic defence manufacturing and technological innovation.

• Order Successes: Avantel has secured projects under iDEX (e.g., Ku band portable/airborne terminals, Satphones) and executed major contracts for Indian Railways, ISRO, and defence shipyards, reflecting healthy demand visibility.

• Diversification: The push into medical devices also leverages increased demand for domestic innovation in critical healthcare products.

R&D Investment & Capability

• Current R&D Spend: ₹366.5 lakhs in FY25 (2.63% of turnover, excluding product-specific development).

• Philosophy: All major products are developed in-house; the R&D center is recognized by the Department of Scientific and Industrial Research.

• Focus: Persistent innovation in core domains (SDRs, phased array antennas, radar, satellite comms), along with diversification into medtech.

• Facilities: Major new capex, with state-of-the-art R&D/manufacturing hubs in Hyderabad and Andhra Pradesh.

• Quote: “The Company invests its time and resources to constantly scale & upgrade in emerging technologies as per the needs of its customers.”

Management’s Guidance & Statements

• “Avantel has achieved a turnover of Rs. 248.67 Crores for the financial year 2024-25 which is the highest turnover since inception.”

• “We are confident of developing Software Defined Radios for airborne applications during the current financial year 2025-26 and will be one of the top five companies in the area.”

• “No major threats are envisaged, and company has visibility for the next three years.”

• “Innovation in design as well as operations is helping Avantel stay ahead.”

• “All the product offerings of the Company have been developed indigenously in house by Avantel R & D wing and truly qualify the ‘Make in India’ requirements being prophesied by the Government.”

• “Your company… obtained authorisation from IN-SPACe for setting up GSaaS (Ground Station as a Service)… operational by 15th June 2025.”

In Summary

Avantel’s growth plan rests on deep R&D, large-scale manufacturing expansion, new product rollouts (especially in SDRs, phased array antennas, and radar), and government-driven industry tailwinds. Strategic investments in innovation and facilities, along with venture into the medtech sector, place the company at the center of a multi-billion dollar, multi-year domestic opportunity across defence, space, and healthcare.

18 Likes

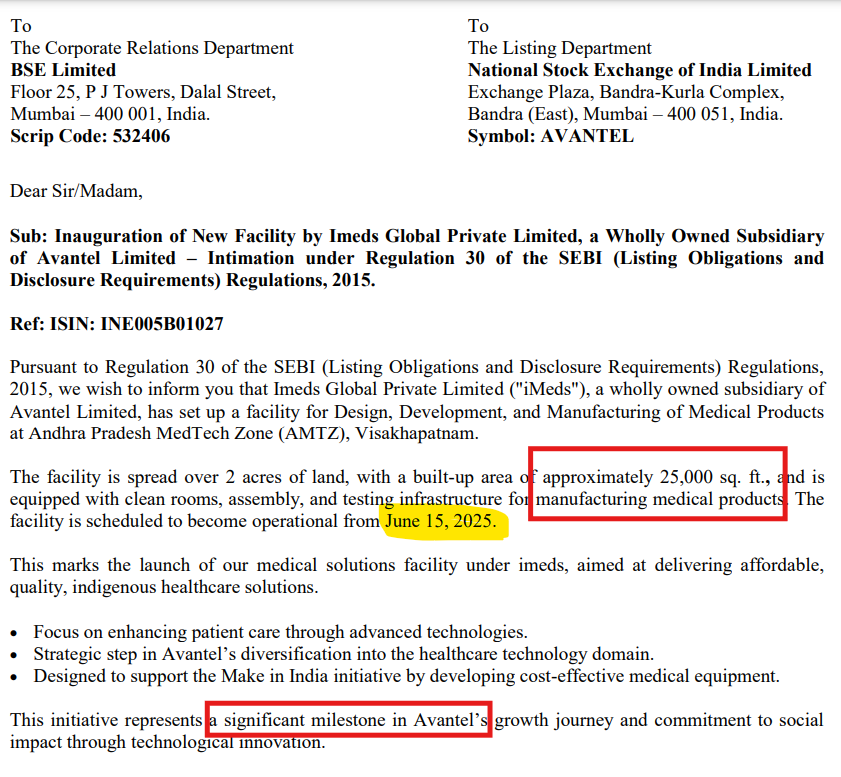

Inauguration of New Facility by Imeds Global Private Limited, a Wholly Owned Subsidiary

of Avantel Limited –

5 Likes

Did some attend agm and what are the points discussed by the company ?

3 Likes

AVANTEL AGM SUMMARY JUNE 2025.pdf (3.8 MB)

18 Likes