I started compiling these notes few weeks ago, when US tariffs were in force and only Q2 FY26 results were available. So I am posting them with timelines.

02/02/2026

1. Summary

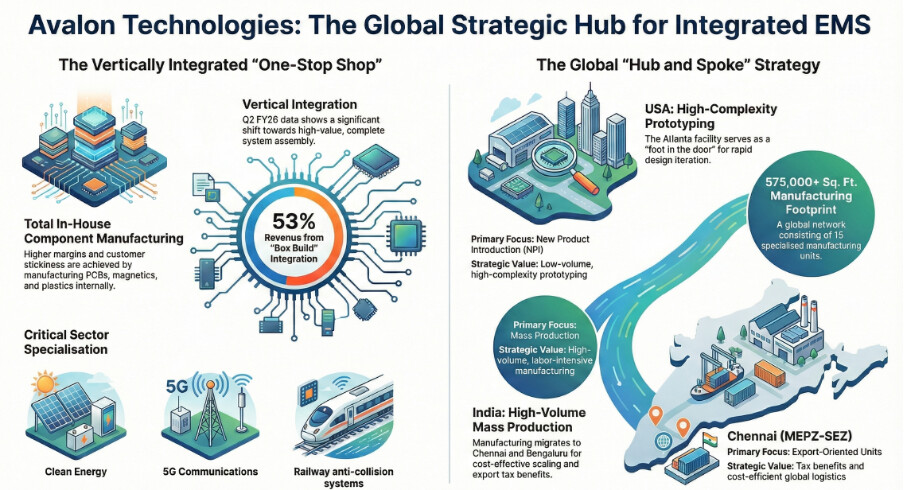

Avalon Technologies is one of India’s leading fully integrated Electronic Manufacturing Services (EMS) companies. Unlike mass-volume consumer electronics manufacturers (like those making mobile phones), Avalon specializes in high-mix, flexible-volume manufacturing for critical industries such as Aerospace, Railways, Clean Energy, and Industrials.

The company distinguishes itself through a “Dual-Shore” manufacturing model, operating high-tech facilities in the United States (Atlanta) and cost-efficient volume manufacturing in India (Chennai, Bengaluru). This unique structure allows Avalon to offer clients the best of both worlds: US-based prototyping and complex integration close to the end-market, and India-based low-cost volume production.

2. Company History & Evolution

Founded in 1999 by Kunhamed Bicha and Bhaskar Srinivasan, Avalon started as a pure-play Printed Circuit Board (PCB) assembler in Chennai. Over 25 years, it has evolved into a vertically integrated solutions provider.

-

1999: Incorporated as Avalon Technologies Pvt Ltd in Chennai.

-

2003: Earned first ISO 9001 certification.

-

2005-2008: Opened dedicated facilities for cables and PCB assembly.

-

2009: Strategic Acquisition: Acquired design capabilities to move up the value chain (ODM services).

-

2010-2011: Entered high-barrier sectors like Aerospace and Railways.

-

2016: Enhanced “Box Build” capabilities (assembling the full final product, not just components).

-

2023: Listed on NSE/BSE via IPO.

-

2024-25: Strategic entry into Semiconductor Equipment components and Clean Energy (Solar/Hydrogen).

-

2025: Commissioned a new export-focused facility in Chennai (MEPZ-SEZ).

3. Promoter Background & Remuneration

The company is led by technocrats with deep domain expertise in the US and Indian markets.

Key Personnel

-

Kunhamed Bicha (Chairman & Managing Director):

-

Background: Founder with over 2 decades of experience in the EMS sector. He drives the company’s strategic vision, particularly the cross-border India-US synergy.

-

Remuneration (FY25): Approximately ₹23.73 Million.

-

-

Bhaskar Srinivasan (Non-Executive Director):

-

Background: Co-founder, instrumental in setting up the operational framework and US client relationships.

-

Remuneration (FY25): Approximately ₹7.58 Million.

-

-

Suresh Veerappan (CFO): Leads financial strategy, capital allocation, and investor relations.

4. Products & Capabilities

Avalon is a “One-Stop Shop” for EMS. It does not just assemble parts; it manufactures the sub-components in-house, leading to higher margins and customer stickiness.

Core Capabilities

-

PCB Design & Assembly (PCBA): Complex multi-layer boards for critical applications (e.g., signaling systems, medical devices).

-

Cable & Wire Harness: Custom cable assemblies for power, RF, and data transmission.

-

Magnetics: Transformers, inductors, and coils manufactured in-house.

-

Sheet Metal & Machining: Precision metal fabrication for enclosures and chassis (critical for “Box Build”).

-

Injection Molded Plastics: High-precision plastic parts for casings and components.

-

Box Build (System Integration): assembling the final finished product. Box Build revenue contributed 53% of total revenue in Q2 FY26, indicating a shift towards higher value-add work.

Key Industries Served

-

Industrials: Power automation, heavy machinery control systems.

-

Mobility:

-

Railways: Braking systems, signaling, and the new Kavach anti-collision system.

-

Aerospace: Cabin subsystems, engine parts (AS9100D certified).

-

-

Clean Energy: Solar inverters, hydrogen fuel cell components, and EV charging infrastructure.

-

Communications: 5G infrastructure equipment and satellite systems.

5. Manufacturing Facilities

Avalon operates 15 manufacturing units globally, with a total manufacturing area of 575,000+ sq. ft..

-

India (Chennai & Bengaluru): Focus on high-volume, labor-intensive manufacturing. The Chennai units are located in the MEPZ-SEZ (Special Economic Zone), providing tax benefits for exports. A new export-oriented unit was recently commissioned in Chennai.

-

USA (Atlanta, Georgia): Focus on high-complexity, low-volume NPI (New Product Introduction) and prototyping. This facility allows US clients to iterate designs quickly before shifting mass production to India (“hub and spoke” model).

Strategic Advantage: The US facility acts as a “foot in the door” for clients who are wary of offshoring immediately. Once the prototype is perfected in Atlanta, Avalon migrates the bulk manufacturing to Chennai for cost savings.

6. Financial Analysis & Quality of Earnings

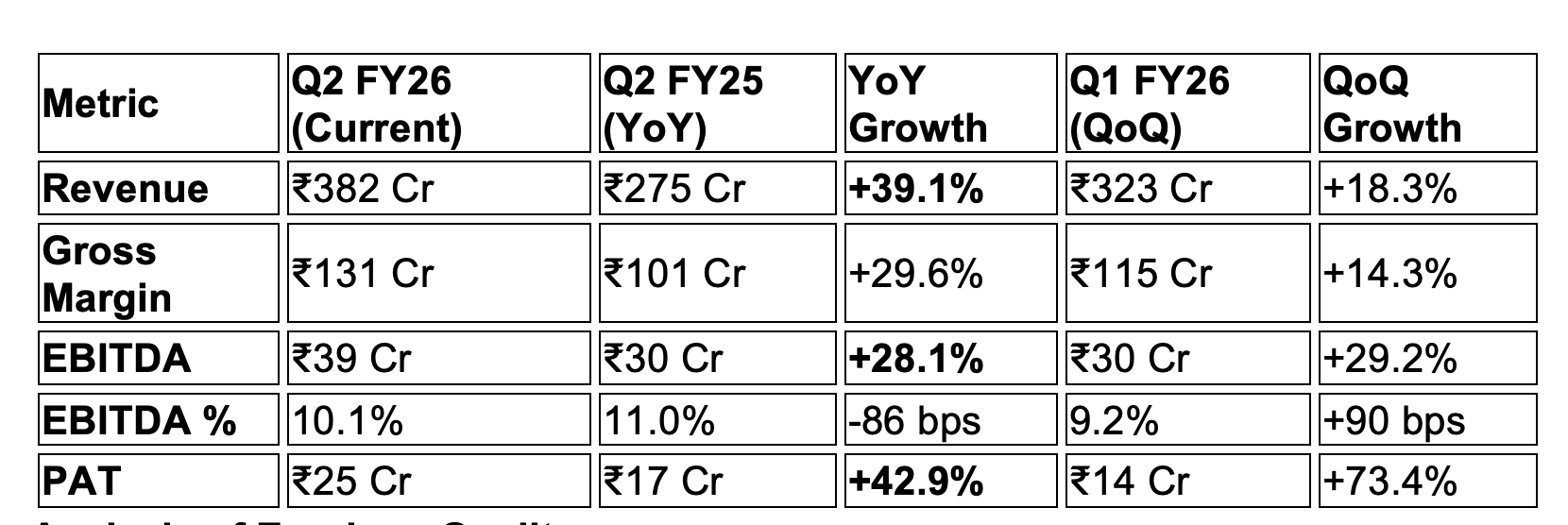

Latest Q2 FY26 Results vs. Previous Periods

Avalon demonstrated strong momentum in Q2 FY26, driven by a rebound in US demand and ramp-up of new Indian programs.

Analysis of Earnings Quality:

-

Revenue Growth: The 39% YoY growth is organic and volume-driven, validating the recovery in the US market and strong domestic order inflows.

-

Other Income Impact: In Q2 FY26, “Other Income” was ₹115.79 Million, which is substantial relative to the Profit Before Tax of ₹331.63 Million. Investors should note that a portion of the bottom line is supported by non-operating income (likely interest on cash reserves/IPO proceeds), meaning core operating profitability is slightly lower than headline PAT suggests.

-

Margin Pressure: Gross margins compressed by ~250 bps YoY (36.8% to 34.3%) due to a shift in product mix (more Indian customers, typically lower margin than US) and ramping up of new facilities which are not yet at full efficiency.

7. Working Capital & Cash Flows

For an EMS company, working capital management is the critical risk factor.

-

Net Working Capital (NWC) Days: Improved significantly to 129 days (H1 FY26) from peaks of >160 days in FY24. This shows better management of inventory and receivables.

-

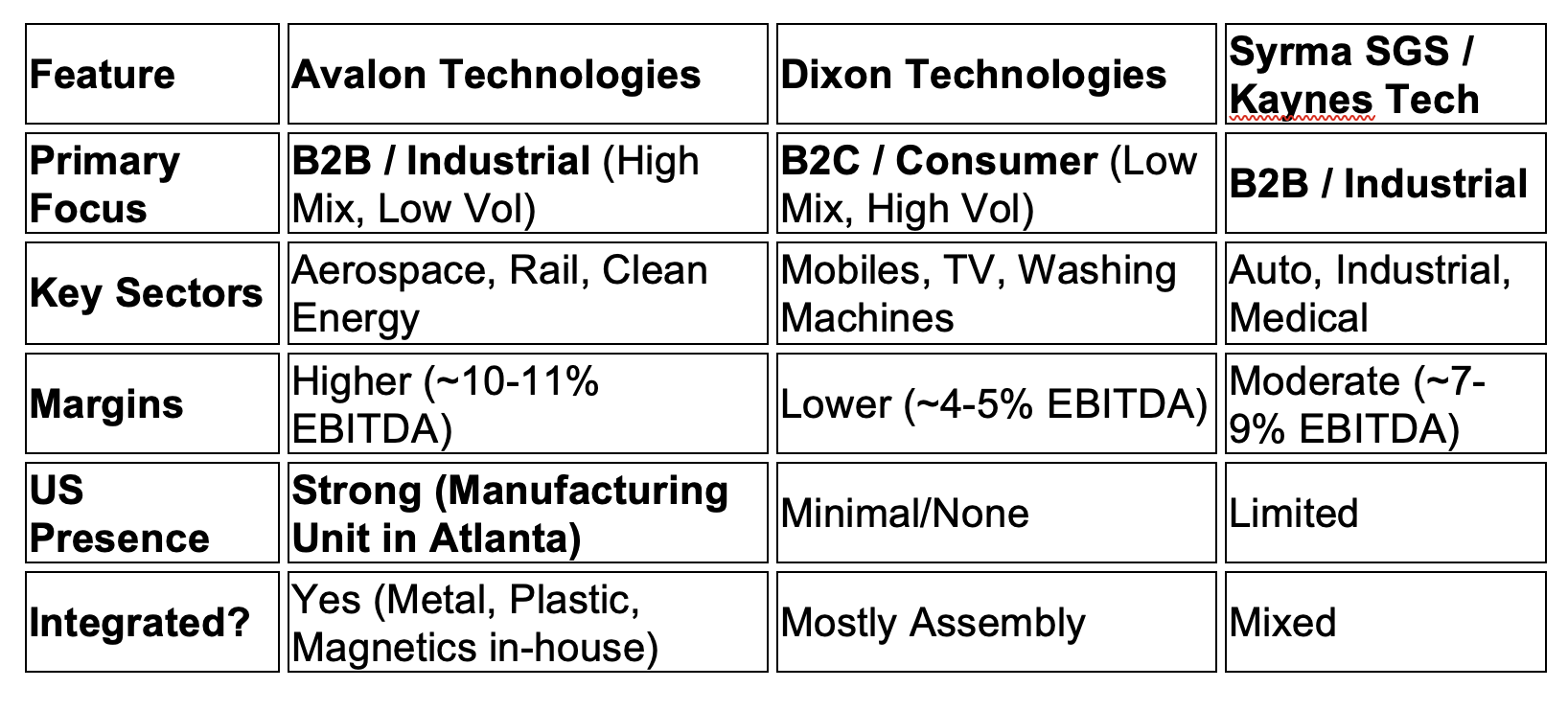

Inventory Management: Inventory days stand at 86 days. While improved, this is still relatively high compared to pure-play assembly peers (like Dixon), but typical for “High-Mix, Low-Volume” players who must stock varied components for diverse clients.

-

Cash Flow Concern:

-

Operating Cash Flow (OCF): For H1 FY26, OCF was negative ₹10 Cr.

-

Reason: The company is front-loading inventory to execute its large ₹1,863 Cr order book. While this indicates growth, it burns cash in the short term.

-

Free Cash Flow (FCF): Currently negative due to working capital build-up and ongoing Capex.

-

8. Capex, Timelines & Future Prospects

Capex Strategy

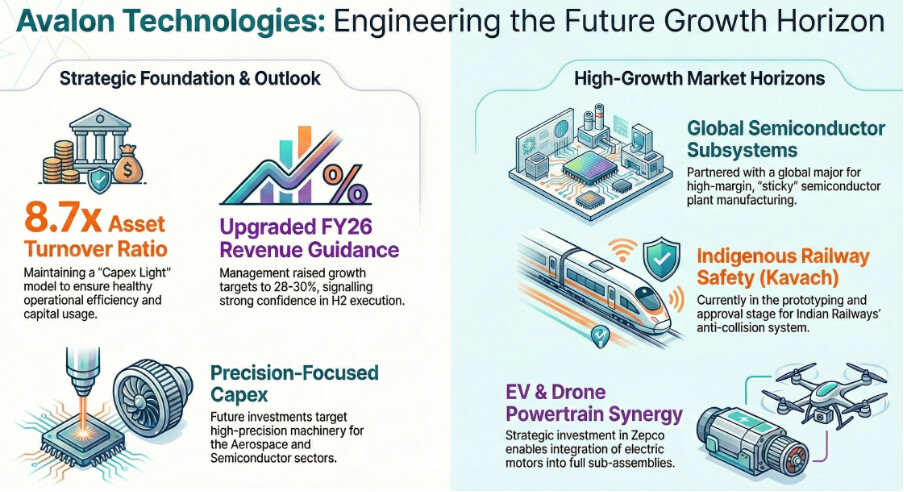

Avalon follows a “Capex Light” model. The asset turnover ratio is healthy at 8.7x.

-

Recent Capex: Investment in the new Chennai facility (Phase II brownfield expansion) to serve export demand.

-

Future Capex: Focused on upgrading machinery for high-precision sectors (Aerospace/Semicon) rather than just building massive sheds.

-

Future Opportunities

-

Semiconductor Equipment: Avalon has partnered with a global major to manufacture subsystems for semiconductor plants. This is a high-margin, “sticky” business with long qualification cycles.

-

Clean Energy: Producing components for hydrogen and solar sectors.

-

Kavach System: The Indian Railways’ indigenous anti-collision system offers a massive domestic opportunity. Avalon is in the prototyping/approval stage for this.

-

Guidance: Management raised FY26 revenue growth guidance to 28-30% (up from 23-25%), signaling strong confidence in H2 execution.

9. Acquisitions & Synergies

The user asked about acquisitions. Avalon generally prefers organic growth but makes strategic tech investments.

-

Zepco Technologies (Recent Strategic Investment): Avalon acquired a ~4.05% stake in Zepco.

- Synergy: Zepco specializes in electric motors, drives, and controllers. This allows Avalon to integrate these critical components into its offerings for the EV and Drone sectors, moving beyond just circuit boards to full powertrain sub-assemblies.

-

Past Acquisition (2009): Acquired a design firm to add “New Product Introduction” (NPI) capabilities, which today is the cornerstone of their high-margin US business.

10. Competition Analysis

vs. China

- The “China+1” Tail wind: Global OEMs are actively moving manufacturing out of China to de-risk supply chains. Avalon is a prime beneficiary because it offers a US-India hybrid option. Clients can keep IP-sensitive prototyping in the US (Atlanta) while moving volume production to India, completely bypassing China.

vs. Indian Peers

Avalon operates in a different niche than most Indian EMS players.

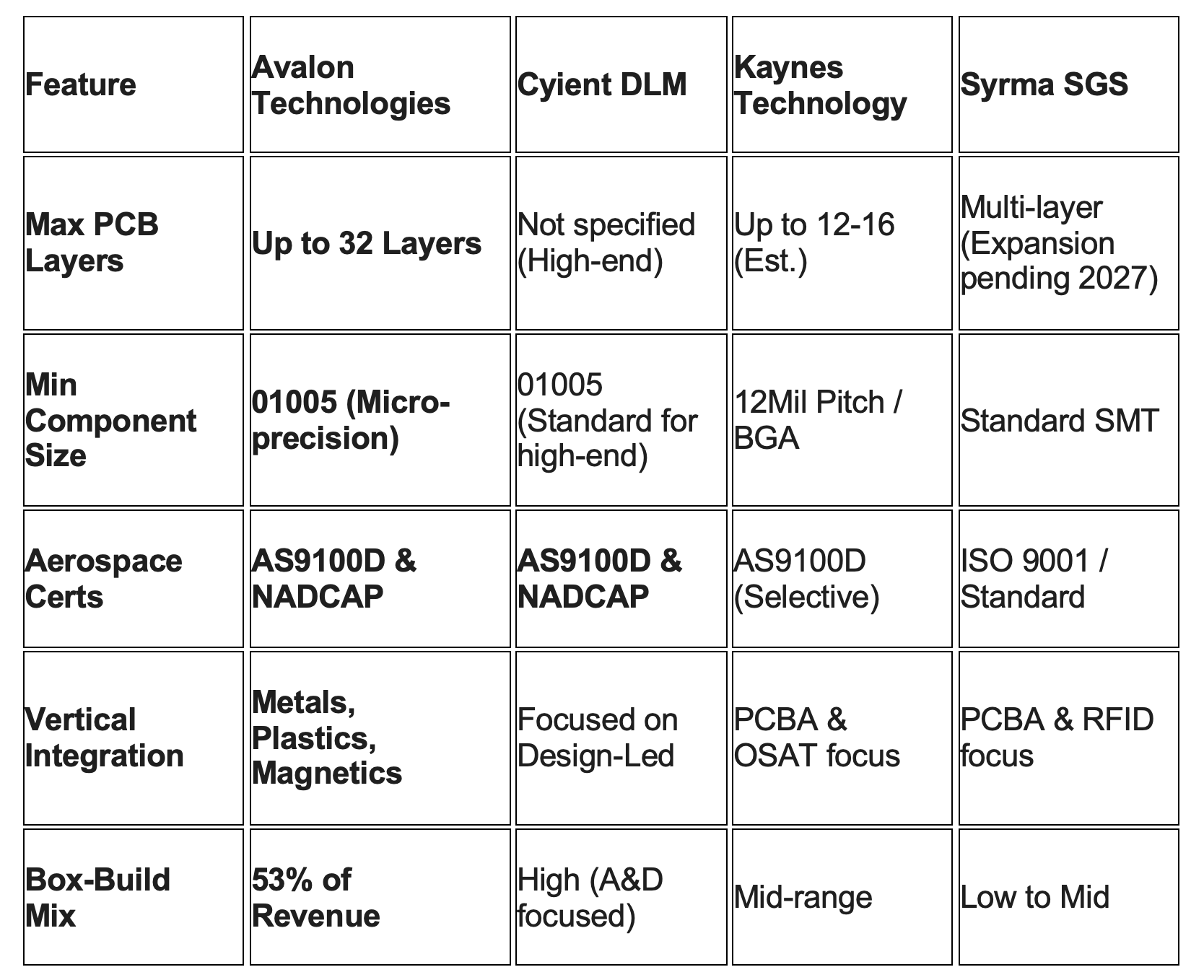

Avalon does not compete directly with Dixon (volume play). Its closest peers are Kaynes Technology and Cyient DLM, which also focus on high-value, low-volume industrial/aerospace electronics.

11. Red Flags, RPTs, & Contingent Liabilities

-

Contingent Liabilities: The company has reported contingent liabilities of approximately ₹2.76 Cr (related to tax disputes/claims not acknowledged as debt). This is low relative to their balance sheet size and not a major alarm.

-

Related Party Transactions (RPT): RPTs are generally at arm’s length. The rental of premises from promoters or related entities is common in mid-cap family-owned businesses but should be monitored. The AR states RPTs are in the ordinary course of business.

-

Customer Concentration Risk:

-

US Reliance: ~61% of revenue comes from the US. While this drives high margins, it exposes Avalon to US economic slowdowns or protectionist policies (tariffs). However, management states they recover 99% of tariffs from clients.

-

Top Clients: A significant portion of the order book is concentrated among a few top global OEMs. Loss of a key account (like Collins Aerospace or their major Rail client) would be material.

-

-

Cash Burn: The negative Operating Cash Flow in H1 is a “Yellow Flag”. While explicable by growth, continuous cash burn to fund inventory for new orders can strain the balance sheet if receivables are delayed.

12. Risk Factors

-

Working Capital Intensity: The business requires upfront investment in inventory. If clients delay payments (Receivables > 90 days), liquidity tightens.

-

Currency Fluctuation: With >60% revenue in USD and costs in INR/USD, volatility impacts margins. (Mitigated by natural hedging via US operations).

-

Execution Risk: Ramping up the new Chennai facility and semiconductor lines requires precise execution. Delays leads to margin drag (overhead absorption issues).

-

Geopolitical Risks: Changes in US import tariffs could theoretically hurt the “India to US” export model, though the “China+1” trend currently outweighs this.

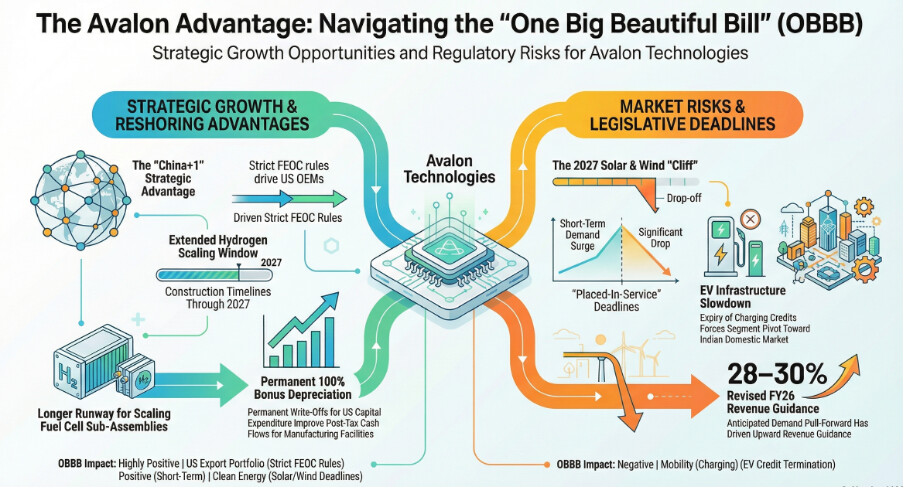

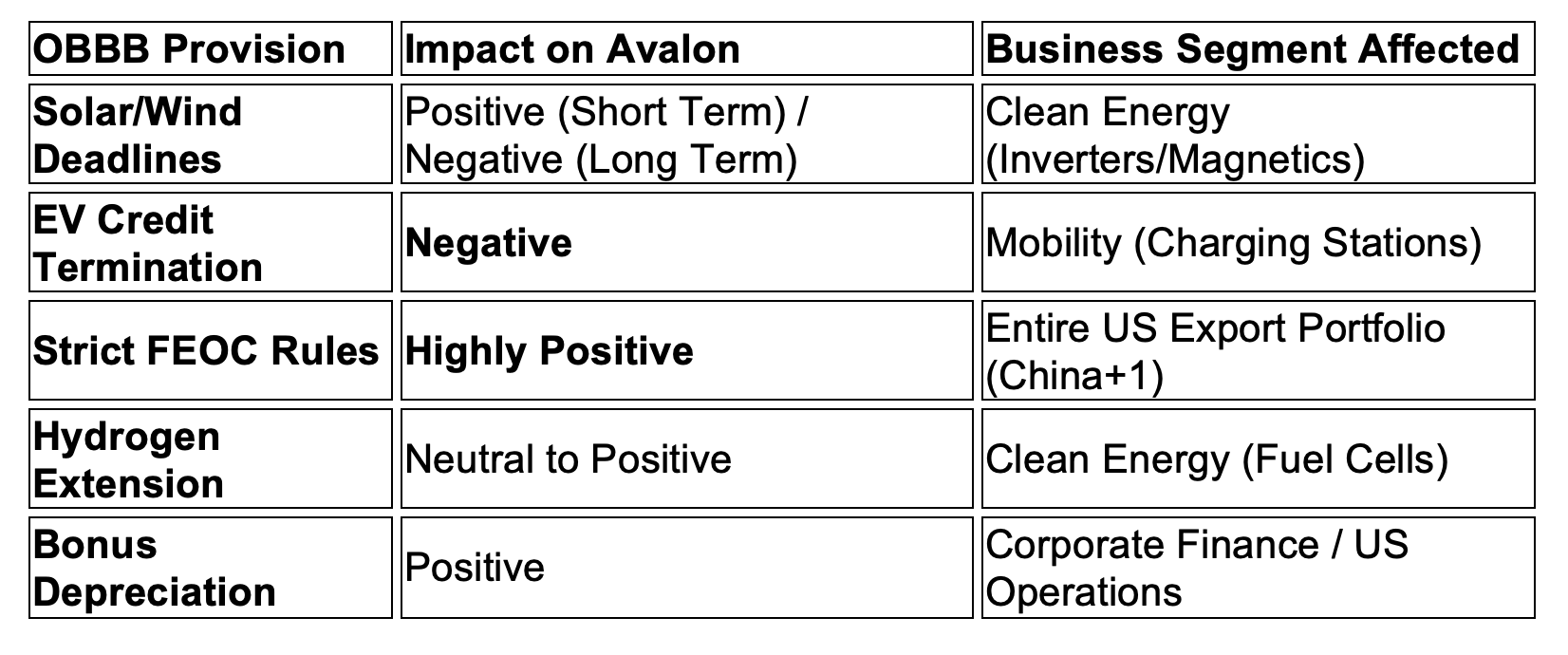

“One Big Beautiful Bill” (OBBB)

The “One Big Beautiful Bill” (OBBB), signed into law by President Trump on July 4, 2025, represents a significant policy shift that directly impacts Avalon Technologies, particularly its Clean Energy and EV segments.

Based on the recent legislative details and Avalon’s Q2 FY26 performance (reported in November 2025), here is how the OBBB affects the company:

1. Accelerated “Rush-to-Finish” for Solar & Wind

The OBBB imposes a strict “placed-in-service” deadline for wind and solar projects. To claim the remaining tax credits, projects must be completed by December 31, 2027, or have commenced construction by July 4, 2026.

-

Impact on Avalon: Avalon manufactures solar inverters and power conversion systems. In the short term (H2 FY26 and FY27), this creates a demand pull-forward. US developers are likely to accelerate orders to meet the 2027 deadline. This is reflected in Avalon’s revised upward revenue guidance (28–30%) for FY26.

-

The “Cliff” Risk: Post-2027, the demand for utility-scale solar components in the US may drop significantly as federal subsidies for these specific technologies phase out.

2. Elimination of EV and Charging Credits

The OBBB terminates the New Clean Vehicle Credit (30D) and Commercial Clean Vehicle Credit (45W) by September 30, 2025, and the charging station credit (30C) by June 30, 2026.

-

Impact on Avalon: Avalon’s exposure to the EV charging infrastructure market is at risk. With the expiration of the 30C credit, the rollout of US charging networks is expected to slow down. Management may need to pivot this segment toward the Indian domestic market or other geographies to offset the US slowdown.

3. Tightened FEOC (Foreign Entity of Concern) Rules

The OBBB introduces aggressive restrictions on “Prohibited Foreign Entities,” specifically targeting Chinese ownership and material sourcing in the clean energy supply chain.

-

Strategic Advantage for Avalon: This is perhaps the biggest positive for Avalon. Because the bill makes it nearly impossible for projects using Chinese-linked components to qualify for tax benefits, US OEMs are under immense pressure to decouple from China.

-

Avalon’s “Dual-Shore” model (Atlanta for NPI and India for volume) becomes the preferred “China+1” alternative. During the Q2 earnings call, management noted that the “India-US” synergy is a major factor in their order book growth (₹1,863 Cr).

4. Expansion of Hydrogen Timelines

Unlike solar and wind, the OBBB was slightly more lenient with Clean Hydrogen, allowing the Production Tax Credit (PTC) to continue for projects starting construction through 2027.

- Impact on Avalon: Avalon has recently entered the hydrogen fuel cell component space. The 2027 window provides a longer runway for Avalon to scale its hydrogen-related sub-assemblies compared to its solar business.

5. Corporate Tax Benefits (Bonus Depreciation)

The OBBB made 100% Bonus Depreciation permanent for business property acquired after January 19, 2025.

- Impact on Avalon: As a capital-intensive manufacturer, Avalon benefits from the ability to immediately write off its US-based Capex (like equipment for its Atlanta facility). This improves the company’s post-tax cash flows, partially offsetting the negative operating cash flow seen in H1 FY26 due to inventory build-up.

Summary

Investor Perspective: While the OBBB creates a challenging environment for US renewables, Avalon is uniquely positioned to capture the market share moving away from China. The company’s pivot toward high-mix sectors like Semiconductor Equipment and Railways (Kavach) acts as a hedge against the volatility in the US clean energy legislative landscape.

================================================================

Avalon Technologies is a high-quality, niche EMS player that is distinct from the mass-market assemblers. It is an “Industrial Proxy” rather than a “Consumption Proxy.”

-

Positives: Strong order book, high entry barriers (Aerospace/Rail certs), integrated manufacturing, and unique US footprint.

-

Negatives: High working capital needs and current negative cash flow from operations.

-

Outlook: With the raised guidance and entry into the semiconductor/clean energy space, the company is positioned for robust growth, provided it manages its cash conversion cycle effectively.

===============================================================

-

-

11/02/2026

Addendum: Q3 FY26 Performance & Strategic Updates

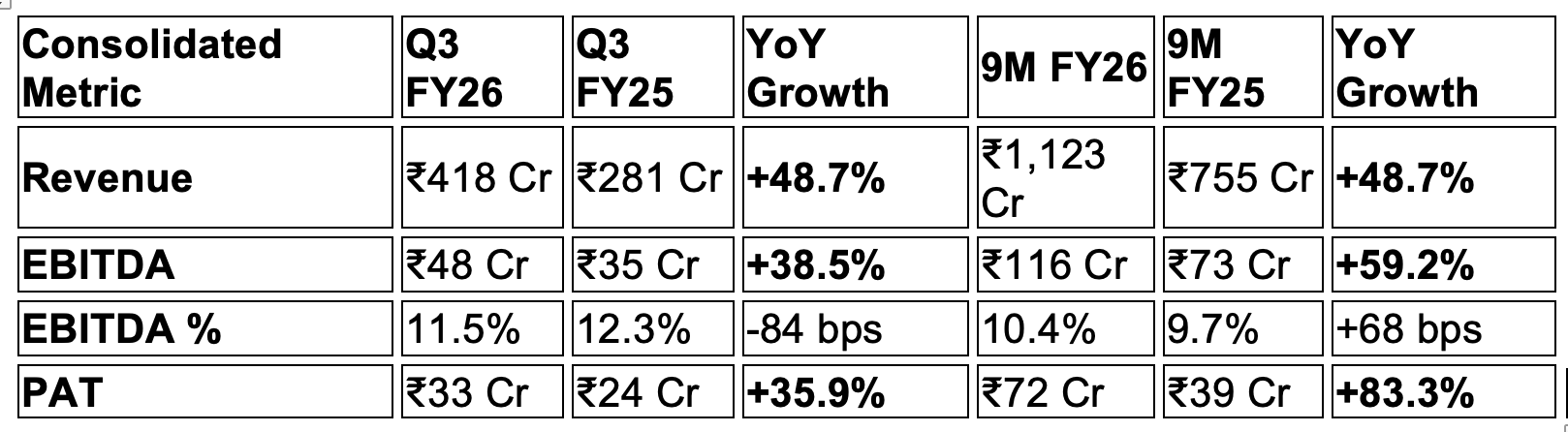

1. Latest Financial Performance (Q3 & 9M FY26)

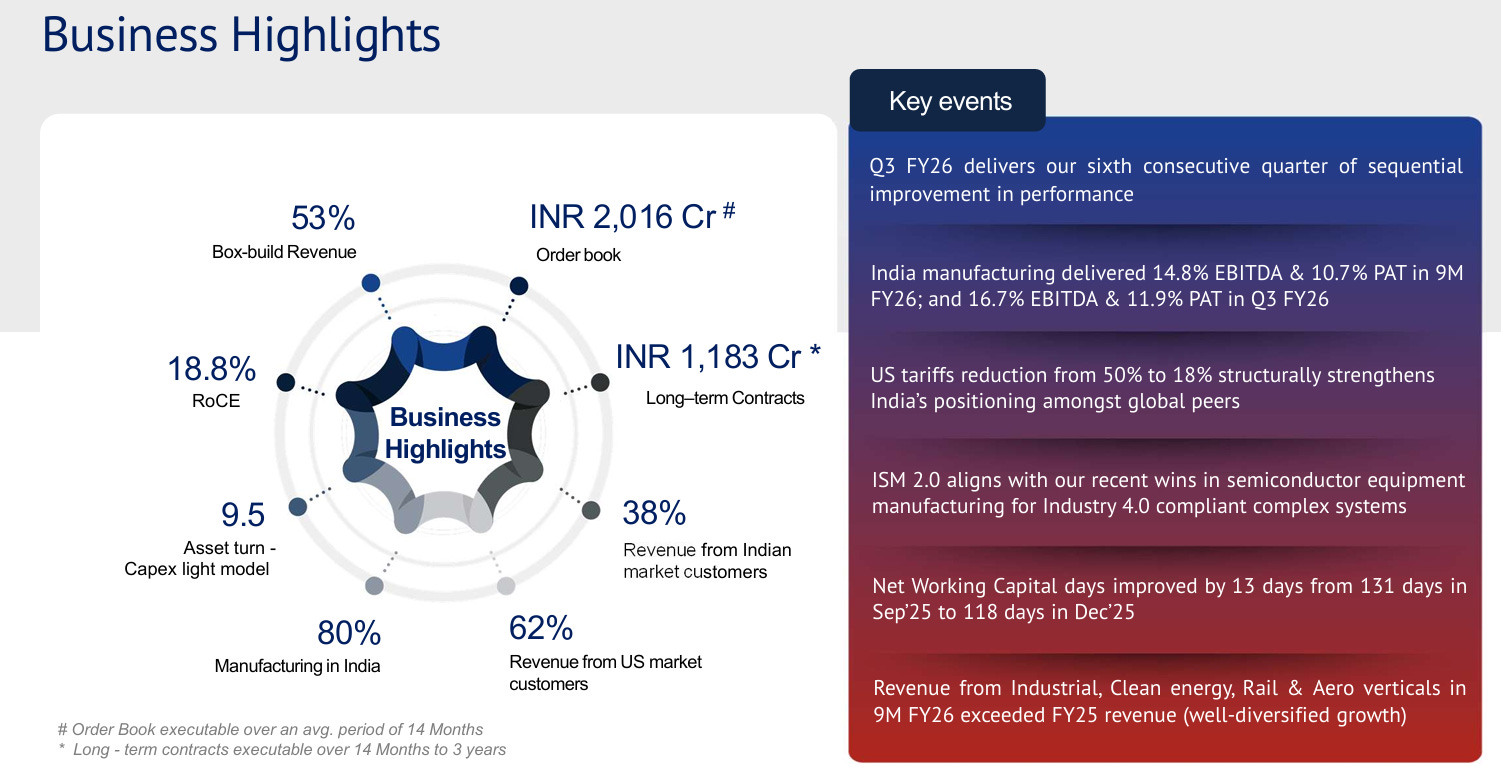

Avalon reported its strongest quarterly performance to date in Q3 FY26, marking its sixth consecutive quarter of sequential growth.

-

-

Guidance Update: Due to improved visibility and project ramp-ups, management significantly revised its FY26 revenue growth guidance upward to ~40%, compared to the earlier revised guidance of 28%–30%.

-

Order Book: The order book reached ₹2,016 Cr as of December 31, 2025, with an average execution period of 14 months. Additionally, long-term contracts (15–36 months) stand at ₹1,183 Cr.

2. Vertical Growth & Segment Highlights (9M FY26)

Growth was well-diversified across high-margin industrial and mobility sectors:

-

Industrials (35% of Revenue): Grew 67% YoY.

-

Rail (16% of Revenue): Grew 70% YoY, driven by braking and signalling systems.

-

Aerospace (8% of Revenue): Grew 64% YoY.

-

Clean Energy (19% of Revenue): Grew 35% YoY, with strong traction in battery energy storage systems (BESS).

-

Box Build Contribution: Improved to 53% of revenue, reflecting the successful shift toward fully integrated system assembly.

3. Working Capital & Cash Flow Management

The company showed significant structural improvement in operational efficiency:

-

Net Working Capital (NWC) Days: Improved to 118 days in December 2025 (down from 131 days in September 2025 and 150 days in December 2024).

-

Trade Receivables: Reduced sequentially to 72 days.

-

Cash Flow from Operations (OCF): Successfully turned positive with ₹51 Cr generated in Q3 FY26.

-

Asset Turnover: Improved to 9.5x in Q3 FY26 from 7.5x in FY25, maintaining a capital-light model.

-

Return on Capital Employed (ROCE): Reached 18.8%.

4. US Tariffs & Dual-Shore Dynamics

A major tailwind emerged with the reduction of US tariffs on imports from India from 50% to 18%.

-

Impact: During the high-tariff period, Avalon recovered 99% of costs from customers, showing high customer stickiness. The lower 18% rate now makes Indian manufacturing for US customers even more competitive against other Southeast Asian nations and China.

-

US Operations Profitability: While the US facility still operates at a loss (~₹7 Cr PAT loss in Q3), the losses are narrowing as energy storage systems and new programs ramp up.

-

5. Future Prospects: Semiconductor & New Programs

-

Semiconductor Equipment: Avalon completed the project readiness phase for a global major to manufacture Industry 4.0-compliant complex subsystems. This is expected to contribute meaningfully to revenue starting in FY27.

-

Satellite Communications: Completed prototypes for control units in satellite antenna systems; volume orders are expected in FY27.

-

Aerospace Expansion: Bidding on advanced metal cockpit assemblies and landing gear components, moving further up the value chain.

-

Energy Storage (BESS): A significant long-term growth driver in the US, particularly as demand for power rises due to data center expansion.

6. Red Flags & Risk Updates

-

Labour Code Impact: New Indian Labour Codes (effective November 21, 2025) resulted in a non-material incremental impact of ₹33 lakh in Q3.

-

Product Mix Margins: While India margins are high (16.7% EBITDA), group margins are currently diluted by US operational losses and a higher mix of Indian domestic revenue.

-

Inventory Levels: Although improved, inventory remains at 97 days, which requires continuous monitoring to prevent cash traps during rapid scaling.

----------------------------------------------------------------------------------------------------------------

Disclosures:

-

-

Compiled Notes from here & there, No Buy/Sell Recommendation. I have a tracking position, still studying & waiting for the price to cool down. The idea to study this company came from @kbsekhar who is an inspiration.

-

Disclaimer: These notes are for educational purposes only and should not be considered as an investment advice. Always conduct your own research or consult with sebi registered financial advisors before making investment decisions.

-

-