Hi Parag,

Very sound analysis. No wonder, Majesco has hit 52 week low recently.

1 Like

Any news on metlife going live in concall?

Metlife has said they will be live in 2020 but no specific answer that is exact date

2 Likes

Thnku… What is the source

Download metlife December 2019 presentation from there website under investor relations

2 Likes

Thanku so much…

Article on USA listed arm of majesco

1 Like

Hey thanks for the article…looks like others are also patiently waiting for the counter to rerate

Concall transcript held on 11 feb

The concall when compared to that of 2-3 quarters back clearly shows the transition going on and reflects well on the management’s strategic efforts. Key point was that only ~20% players are on cloud yet so the addressable opportunity is still huge.

The company needs to sustain the growth rates to command a higher market cap. Currently the counter is clearly undervalued.

What caused today’s fall?

q4 reults: YOY

277cr vs 261cr revenues

23cr vs 9cr net profit.

fy2020: 1040cr vs 988cr revenues

69 vs 54 Net profits

Any thoughts?

1 Like

Good result. Will wait for next wave of correction, if any to add

1 Like

The company is currently at a market cap of 1000 cr. It has net cash of 417 cr. So that means that the entire company is available at less than 600 cr. Also it generated a net profit of 90 cr. this year. Which means it is available at a meagre 7.5 times profit. Add to that the fact that it operates in a sector with a huge runway (Cloud based insurance). To me it looks like a steal. Any thoughts?

2 Likes

Absolutely, looks good with a long runway for growth from recurring revenues.

On the valuation front, Looks reasonable. It is a holding company so it will trade at a discount. Personally, I think the growth gives us a the margin of safety at these levels.

I used to own few yrs back and escaped with a small loss after good 18 months of no performance. I was disappointed by the way their outlook was never achieved what they committed at the time of demerger. I will not go into the details about the past but current numbers do not suggest such a rosy picture either. Cash generation remains weak as for FY20 --> ~80% of (PAT + Depreciation) got locked in receivables while consolidated sales growth was hardly 5%. It means that they are using working capital to flog the horse and generate meager sales growth. Let me know if my analysis is wrong as I have not been tracking it for the last few years.

1 Like

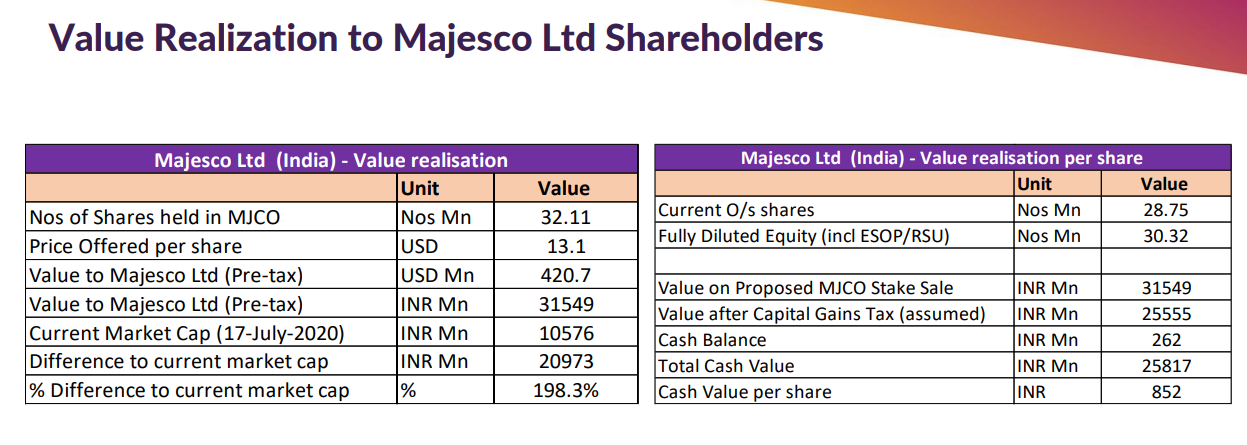

Majesco US has been acquired by PE player for $594 million dollars.

Majesco India is planning to distribute cash of Rs 852 to each shareholder of Majesco, which is more than double the current price- it may take some time to materialise though.

4 Likes

Very disappointing news. I thought this will become a very big story. Alas we hv to settle for this.