Today’s concall summary (Recording is available on research bytes)

About the journey so far…

- Not interested in re-inventing the wheel, this year evaluate about 70 prop tech based companies and choose to that are going to value to do the Auruum Proptech eco system, one was sell.do and other one is Integrow)

sell.do (K2V2) helps in demand generation (lead generation, lead tracking , virtual viewing of the property etcc… ) where as Integrow addressed the property management (revenue) side in the eco system.

-

They already did a prototype based on block chain technology that helps in building eco system of shared / partial ownership of real estate (this is very popular in the west, one of the investment class for investors, for customers who cannot afford to buy they buy in shared ownership and pay the rent for other half of the property owned by the investee company )

-

End goal is to build a super app that has all these building blocks which are decoupled and then well integrated into the ecosystem

-

There were interesting questions raised by Mr. Varinder Bansal from Omkara Capital , the current tech players magic bricks etc… none of them hardly made any profit nor reached to revenue of 200 crore, how confident you are to reach about 500 cr revenue ? The response was very generic, one silver lining is they don’t want to acquire company that is not generating any earnings.

-

K2V2 (sell.do) the target that they have set is to generate revenues of 40 crore (at the moment it is generating 18.8 crore a year on this EBITDA is 3 crore) - this needs to be tracked

-

Integrow - Appears to be generating profits but not many details were given

-

K2V2 on boarded so far 485 B2B customers , their B2C solutions that are about to be launched are going to generate substantial revenues

-

Not interested in burning cash for customer acquisition

-

Integrow a company for corporate’s like AIF companies which are into big real estate projects, integrow help them to acquire and manage the asset

-

Aurum is launching two new products soon

-

They are managed to buy 21% in open buy back offer from the secondary market and 14% from Majesco so their total holding now is 35% , they will evaluate in future how to increase their stake

-

Have 100 crore in cash plush two real estate assets, these will be sold once they find a good value.

3 Likes

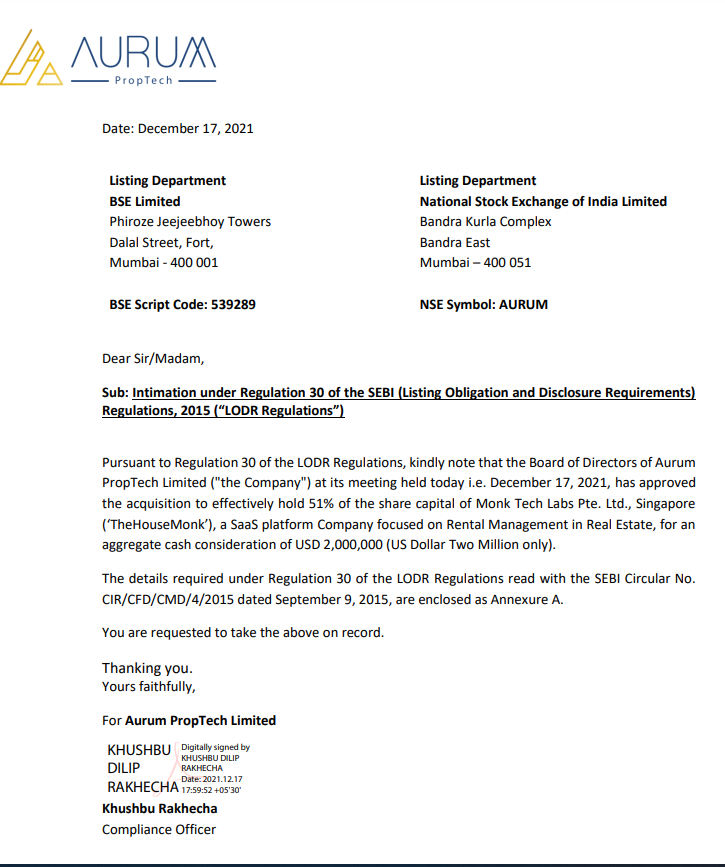

For a 51% stake they paid 20x to sales

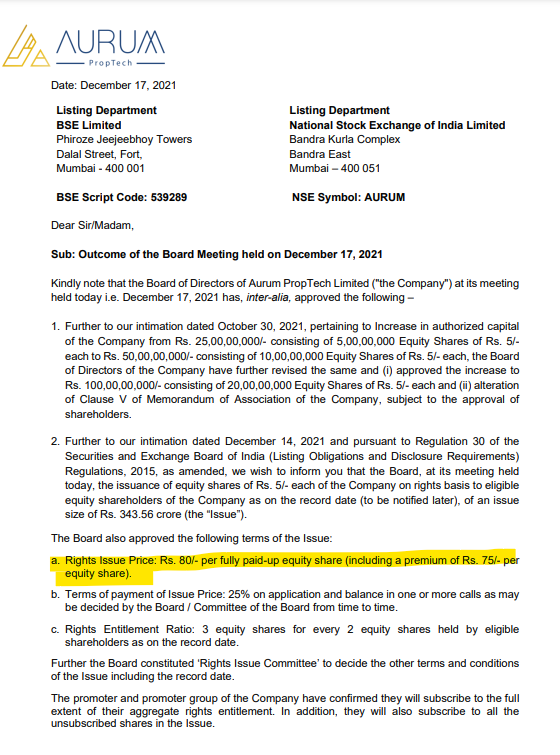

Rights Issue

Currently trading at 145 , they did acquired Majesco at 77 rupees a share

1 Like

How do you read this news hope it is positive

Setup two new subsidiaries

Aurum Softwares and Solutions Private Limited

Aurum Softwares and Solutions Private Limited (‘ASSPL’) is incorporated as a wholly owned subsidiary of Aurum PropTech Limited. As per the certificate of incorporation dated January 7, 2022 issued by Registrar of Companies, Ministry of Corporate Affairs, the date of incorporation is December 1, 2021. Line of Business contemplated – It is contemplated that ASSPL shall carry on the business of consultancy and development of computer software and other information technology enabled services.

Aurum RealTech Services Private Limited

Aurum RealTech Services Private Limited (‘ARSPL’) is incorporated as a wholly owned subsidiary of Aurum PropTech Limited. As per the certificate of incorporation dated January 7, 2022 issued by Registrar of Companies, Ministry of Corporate Affairs, the date of incorporation is December 6, 2021. It is contemplated that ARSPL shall carry on the business of providing workspace solutions, incubation, business planning services and so on through usage of information technology.

Edited : 7/2/22

One more acquisition

2 Likes

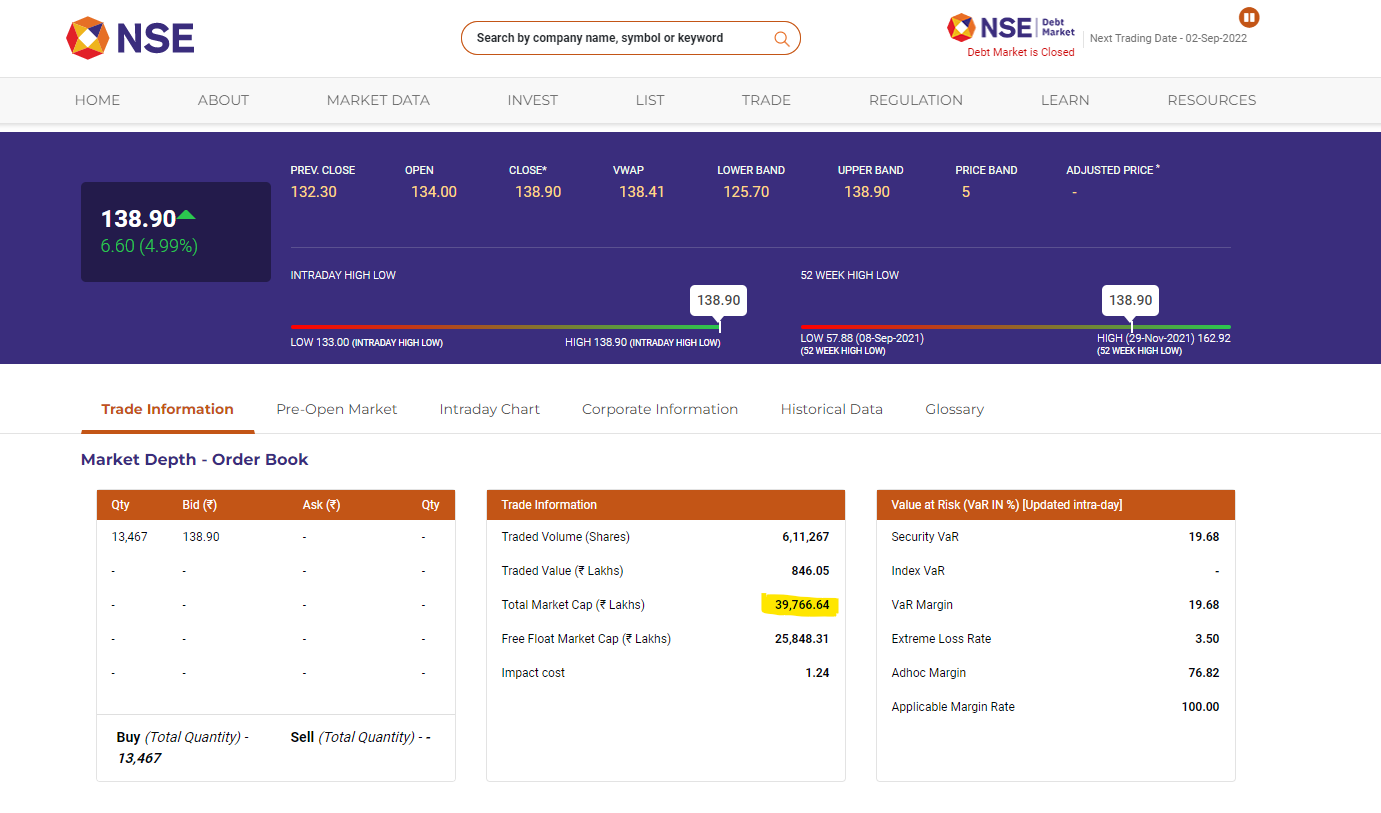

I have a few doubts. Aurum Platz acquired its stake at Rs 77 per share in 2021. What was the market cap of the company?

Today the free-float market cap is Rs 418cr at Rs 90 per share as per BSE website. This means the market cap at Rs 77 per share would have been 418*77/90 crore, that is, around Rs 360 crores.

The total assets of the company as per Q2 results is around Rs 185 crores. For this value of assets, I find it difficult to justify the acquisition price. Shouldn’t it have been around Rs 35?

Disclosure: Tracking position.

3 Likes

Regarding my question, either the assets of the company are understated in the balance sheet or Aurum Platz overpaid for its stake. What is the truth? The company seems to be on the right path but this question is making me wary.

I think I have found the answer to my question. The total number of shares is around 2.86 crores as per the latest Shareholding Pattern (checked on both BSE and NSE). The market cap should be around Rs 90.6 (CMP) x 2.86 crores, that is, around Rs 260 crores, which is same as the market cap shown on Screener.in.

The market cap shown on BSE website is much higher—around Rs 650 crores. I was able to solve this mystery too. There is a huge ongoing rights issue. It will add 4.3cr new shares, making the total to around 7.16cr shares. The market cap on BSE reflects the contribution from the new shares too.

[Earlier I remarked about “free-float” market cap. Free-float is irrelevant here. I learnt later that free-float refers to the non-promoter portion of the market cap (“freely” trading).]

The company notified a couple of days back that it has “committed” investments of around Rs 230 cr. It is unclear if this Rs 230 cr is already reflected in the balance sheet or some of this amount will come from the rights issue. As per the latest balance sheet, the company has around Rs 150 cr of assets (after subtracting liabilities). Given this information, there appears to be quite a lot of margin of safety. The rights issue will give a huge war chest to the company and increase the promoter holding from around 35% to above 50%.

2 Likes

Market value of property in Navi Mumbai was around 200 Cr.

1 Like

Here are my recent notes on the company.

Overview and History

- Before change of promoters in March 2021, the company was named Majesco.

- Majesco’s main business was in the US. In early 2021, Majesco sold its US business and distributed the proceeds as dividend. After the record date, the share price crashed to below Rs 10, but then recovered to around Rs 50.

- On March 21, 2021, Aurum, a Mumbai based Real Estate group, signed a definitive share purchase agreement with erstwhile Promoters to acquire the 14.78 per cent promoter stake in Majesco, through its subsidiary Aurum Platz IT Private Limited (now renamed to Aurum Real-Estate Developers Private Limited) for Rs 32.58 crore at Rs 77 per share. Aurum also made an open offer to acquire 26% more at the same price.

- Two buildings, one of them under construction, were inherited from Majesco. One has been leased out and the other has been completed. They are worth around 100-120 cr in the current market. At that time, Majesco additionally had a cash balance of over Rs 100 cr. Majeso’s market cap at Rs 77 was around 220 cr.

- Since then the company was renamed as Aurum Propech. They acquired and are still acquiring multiple proptech IT companies. Rs 230 cr has been committed into these acquisitions.

- The share price has been very volatile, touching a high of around Rs 160. CMP is around Rs 88.

- Company came up with a Right of Issue recently at Rs 80 that will increase Aurum’s holding to more than 50% and infuse around Rs 340 crore into the company. The market cap at CMP of around Rs 88 will be around Rs 630 cr after dilution.

- Objects of the issue as per the Rights Issue

document:

- Product Development: 37.5 cr

- Product Marketing: 31 cr

- Identified Investments 156.7 cr

- Funding inorganic growth initiatives and general corporate purposes: 113.86 cr

- Net Proceeds (total): 339.07 cr

- Very less institutional investors. Close to 49% shares are with public shareholders.

- Strategy overview is detailed in the Rights Issue

document pp. 108-115.

Segments

-

30 May 2022 concall: Our vision of PropTech ecosystem has four segments:

- invest and finance: typically takes care of the wholesale and retail investments for developing and possessing real estate assets.

- enterprise efficiency: deals with bringing an efficiency in the business of developing and setting and monetizing real estate.

- consumer experience: deals with purchase and renting of real estate, consumption of real estate essentially

- connected living: deals with utilization and enhancing the experience of utilization of real estate assets including renting and resale and monetizing.

Each of the above have been classified into two segments: SaaS (Software as a Service) and RaaS (Real-Estate as a Service). SaaS are typically B2B-oriented whereas RaaS are typically B2C-oriented.

Acquisitions

- 30 May 2022: We are developing an integrated PropTech Ecosystem for consumers and creators of real estate.

- 30 May 2022: A recent report by CII had estimated that PropTech investment will double to USD one billion in 2025 as technology is infiltrating every aspect of real estate.

- 30 May 2022: In span of just 10 months, we have been able to build operation and generate revenues in the company with a hybrid strategy. We now have two SaaS and four RaaS products in the market. Our talent pool has increased from just 5 to 400 as on March 2022.

- 30 May 2022: Operating revenue of Rs 8.2cr in March 2022 quarter. This is from in-house product called CREX.

- 30 May 2022: After the rights issue, the company has an aggregate amount of approximately Rs. 500 Crores plus of cash, real estate and cash equivalent which can be deployed towards the integrated PropTech ecosystem. From the notes in the results of March 2022, I conclude that the aggregate amount above does not include the existing subsidiaries:

- K2V2 (‘Sell.do’ and ‘BeyondWalls’, investment of Rs 40 cr): CRM and Broker aggregation tech for real estate.

- Aurum Realtech Services Pvt Ltd (invested Rs 5cr),

- Aurum Softwares & Solutions Pvt Ltd (invested Rs 16cr),

- Monk Tech Labs Pte Ltd (“TheHouseMonk”, investment of Rs 37cr): SaaS platform for Rental Management

- Integrow Asset Management Private Limited (‘Integrow’, 49% holding–currently not a subsidiary, investment of Rs 25cr): Tech driven real estate asset management company.

- Summary of acquisitions until now: Apart from the above, also includes the following prospective investments:

- Grexter Housing Solutions Private Limited (‘Grexter’, investment of Rs 27cr): Premium Co-living company.

- HelloWorld Technologies India Private Limited (‘HelloWorld’, investment of Rs 56cr): One of the largest Co-living Companies in India.

- Blink Advisory Services Private Limited (‘CareerSocially’, investment of Rs 45cr): A data analytics company focused on real estate sector.

- 30 May 2022: Visibility of Annual Revenue Run-Rate of Rs 95 crores from the acquisitions.

Pros and Cons

Pros

They have Rs 500+ cr cash and cash equivalents now, which means they are ready to play the long game.

Cons

- The management seems untested in Proptech even though they may have experience in real estate through Aurum. [One has to remember the fragmented nature of real estate sector—probably very few people have diverse experience in Proptech.]

- Some of their recently-added subsidiaries were acquisitions at high valuations (the acquisitions provide growth capital to the acquired companies).

- So far their business seems asset-light but not sure how asset-light their business is going to be in the future. Also, misallocation of capital is a possibility in the future.

Overall, the company has an interesting diversified, Saas-based business model and a war chest of capital to sustain growth for the next few years. The current valuations are reasonable. However, the company is in initial stages and the developments in the company need to be monitored.

Disclosure: Not invested.

10 Likes

Based on this the present mcap is 995 cr (630*139/88=995)

what is the market cap of the co now? screener showing 398 cr, google showing 1300 cr, money control showing 565, groww showing 1254 cr…

1 Like

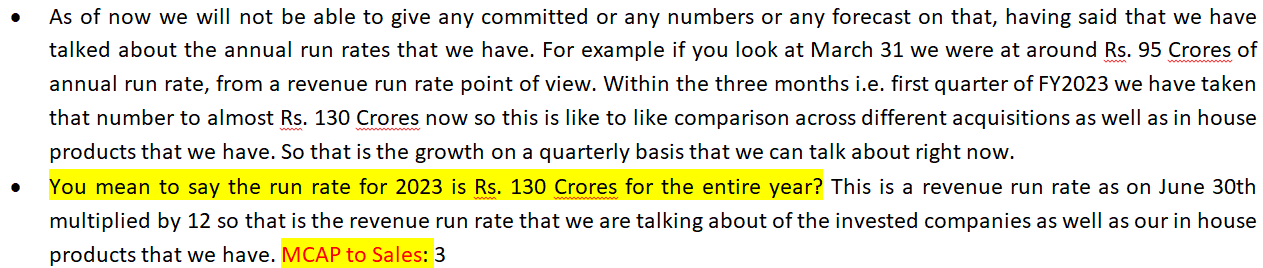

Then based on lates concall the co is available at mcap to sales ratio of 3

Is it cheap? Compared to other platform business like policybazar making -60% EBITDA margin available at mcap to sales of 13.

On Profitibility:

I don’t know the comparison with PB Fintech is correct or not.

Disclosure: Studying

there is no clear idea what exactly they do , no IP nor they bother to explain what is that so called "property market platform eco system " that they are building. They are still burning cash.

2 Likes

If you include the rights issue, then the market cap of Rs 993 cr is correct—this is what is shown on the BSE website.

2 Likes

I opened the lates quarterly result. Divided the PAT with eps to get the no of shares and multiplied by present share price. The market cap as of today 05.09.22 comes to be 647 cr. is this correct??

Finally Investor Presentation .vvvvvvv

Where can I check their real estates that have come along with Majesco acquisition ? Could someone please help me on this ?

I am trying to understand where exactly Aurum prop. tech building blocks fit in ? With whom they are competing with .

https://www.earnnest.me/

https://www.propertyshare.in/ (Fractional Buying )

https://myrecapital.com/

I am just saving my thoughts here.

1 Like

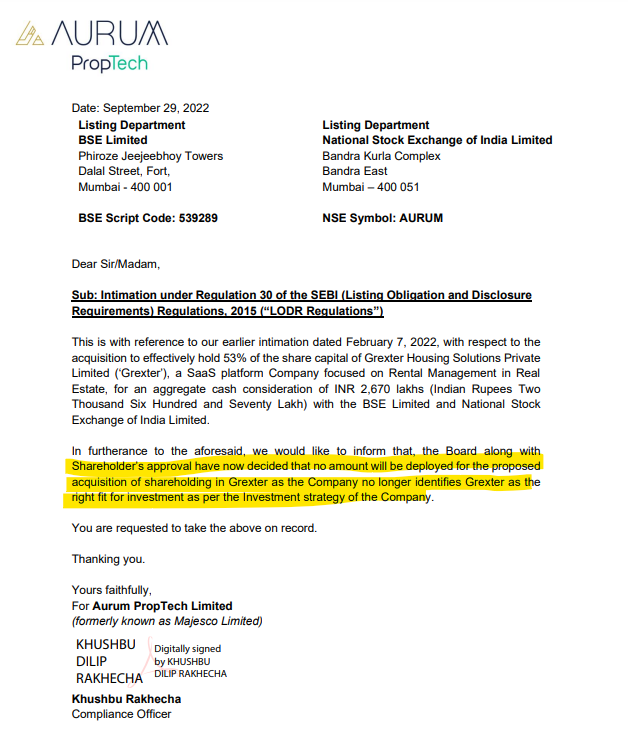

Would like more information on why this fell apart. Hope they put out a press release.

Even though they have not stated their reasons for the reversal, actually I am slightly relieved that they did not acquire Grexter, given their commitment towards developing an asset-light business.

I would welcome any studies on how asset-light their other acquisitions are.

Disclosure: Not invested. Tracking.

1 Like