Generally speaking yes, there are all sorts of promoters in the market. But have you come across past instances of the said promoter acting against minority interest in the past? If yes, that info. will be helpful, if no then we can’t infer much anyway

Just google “Ashank Desai” in google. He is one of the (out of 4) Majeso promoter, and I have observed Mastek promoter over decades and could not find any fault. I would tend to believe what they say, unless for some reason the transaction does not complete, but I personally would not doubt their integrity.

Ashank Desai has a spotless track record as fas as corporate governance goes.

Today majesco closed short of circuit and high volume continues. From tomorrow, looks like the moves may not be so strong after all. I’m still puzzled as to why people are selling, unless they need money for emergency or pledge related.

I suppose the Merger will be investigated and litigated : -

The Legal firms are quite active in US it seems. So for buyers in 180-250 range, selling now is better as they’ll get good returns rather than wait for the last 20% which might not come by.

These kind of litigations are pretty common in US and there is nothing to worry for investors who can stay put, as there is no explicit fraud here… infact, it may even drive up the price and that is precisely what these law suits intend to go after

In fact I was considering a position now - an arbitrage with IRR 20% I jst mentioned a possibility which led to selling in last 2-3 days.

Also the worry factors are always present - in fact, that risk is wat makes an investment worthy - The factors here are : -

The base of Litigation is that a very low price is being paid for the acquisition, when in fact, the price being paid is high relative to the avg mkt price and valuation-wise as well. Yes, all the tech stocks are being valued high right now so the promoter might have initiated a sale, bt by any sensible yardstick $13 is also a high price

Wat’s important to note is the legal accessibility available to investors in the U.S. ( wish the same wd have been the case in India ) Now once these 2-3 firms put up something like this, the one who isn’t interested initially vl also join.

The litigation as you correctly mentioned, are common in U.S because they are mostly settled out-of-court wid money considerations. Hence, it might happen, that a part of deal money is used to pay and settle wid these law firms. This will reduce the per share amount value available to shareholders here to some extent.

All-in-all, the arb here is weighing the risk-reward in light of above facts.

Can you elaborate on point 3 further? I can think of two scenarios:

Out of court settlement results in PE agreeing for a higher price say 10% but Majesco SH only get 5% additional as remaining goes to lawyers - so net-net gain to shareholders

PE doesn’t pay up as $13 ends up being the final price… in this case, will the expense will be so large that it impacts price say by ~ INR 200?

So, can’t 1 still lead to some gain and scenario 2 doesn’t have major downside unless someone litigates as it was too pricey. Am I missing something here?

Disclosure: Invested for more than three years, no transactions in last three months

The surprising and concerning part is that the shareholders resolution for voting on the transaction was circulated even before clearing the payout methodology

I think @vagator10 has raised the core issue, investor should be mindful that instead of a very loose promise to pay company should have entered into an agreement with shareholders that all the money received from sale of US subsidiary will be paid by such and such means till a fixed date to shareholders.

This agreement is totally absent and make the stock a binary event risk.

From one perspective, I blv the valuation paid for the acquisition is already in the high range. Law firms can approach it 2 ways - 1) the litigation lingers in which case the argument comes up as a change of valuation based on changed circumstances. 2) The PE firm wont pay more but Majesco settles by paying part of these proceeds only to the law firms. In dat case, the shareholders will get wat they were getting eventually bt with a cut given to law firms.

As @vagator10 pointed out abt shareholder agreement, I suspect mgmt somewhr knew these sort of legal issues can come up, hence, no commitment given in the form of agreement.

The company having similar revenue as Majesco ($170 million in Fy 2019) and operating in the pretty much the same segment (Majesco is more diversified being present in P&C and Life and Annuity) segment is coming up with an IPO valuing the firm at $2.8 billion. This is in contract to Majesco who is being valued at $600 million. In the US it Guidewire is the leading company followed by DuckCreek, and Majesco most likely at a third place.

Considering Guidewire valued at $10 billion and DuckCreek at $2.5 billion, Majesco valuation looks a steal even at $600 million. Covid-19 is playing in the hands of insurances as they are propelled to invest in digital technologies, so there will be great tailwind to Insurance companies providing products to insurance companies.

As an investor, I feel the comparative prices of Majesco on the lower end, so won’t be surprised (and wishfully hope) that another suiter join the fray to take over Majesco.

So then what happens if the shareholders of majesco hv voted in favor of the deal (promoters pledge indicated they want to get the sale done) but the case ruling in US diverges from the shareholders vote?

Is this sign of some sort of a price war amongst potential bidders if price indeed seems low based on other competitors? Or legal firms pounding on them?

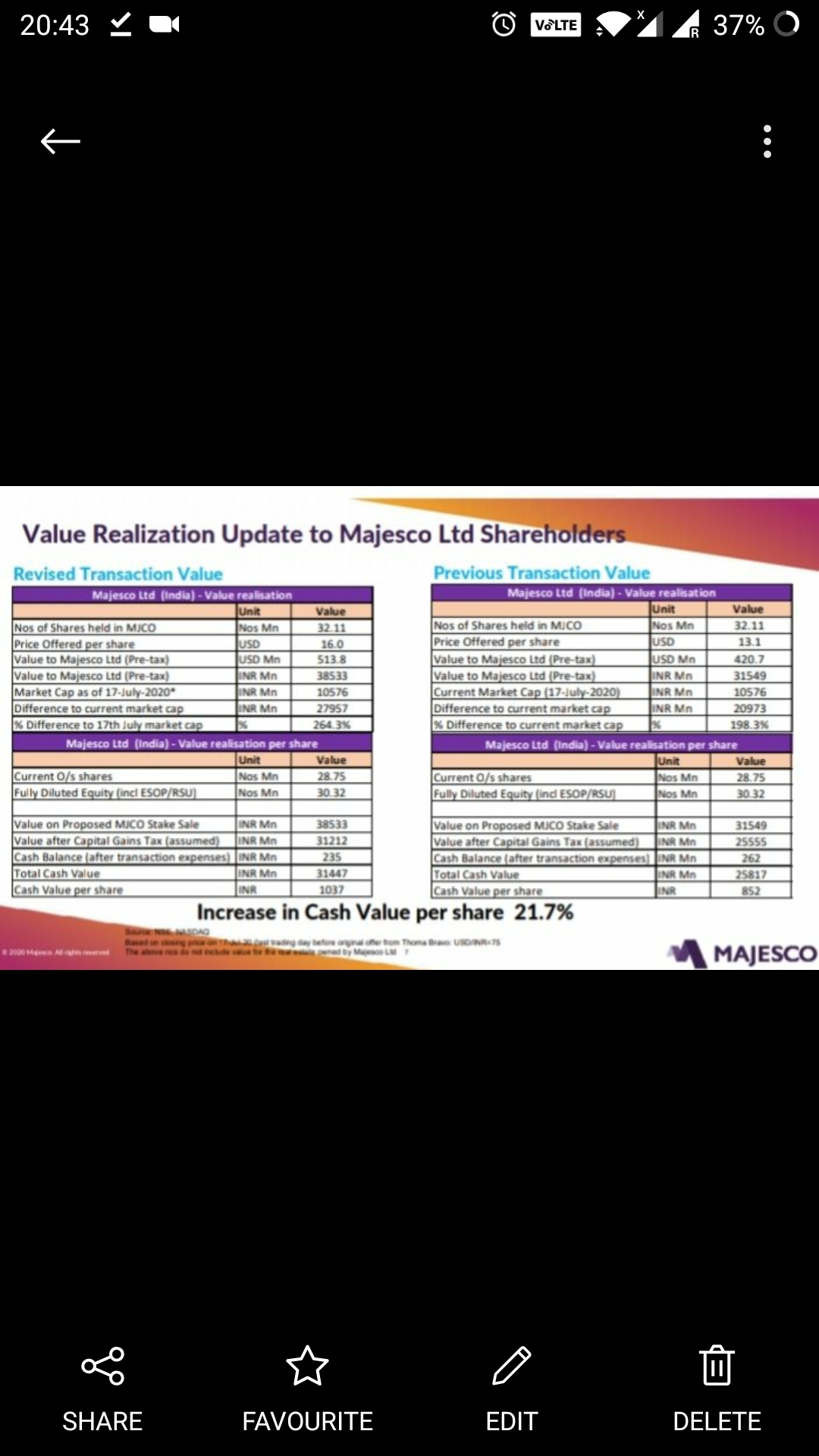

Before I cd reply to this, @Divyanshu_Taneja reported another new development in this whr the price has been increased by Thoma Bravo by $3. This has 2 implications : -

For investors who already hold shares, thr expected returns might increase nd again the decision for thm is the net gain in hand today vs. the expected gain 6-9 months down the line.

For Arbitrs like me, who are not yet invested, the legal battles might hae made the risk-reward ratio unfavorable and I would hv passed. However, Risk reward ratio vis-a-vis IRR is again worth investigating now. Nd price movement next week vl play a part in it. Dis might go to hit UC filters again, bt that’s purely my speculation.

I vl watch the price movement next week and compare the same with other arbitrage optns in the mkts presently. Vl make a call accordingly.

The increased offer from Thoma Bravo and the amendment followed Majesco’s receipt of an unsolicited acquisition proposal from an unaffiliated third party.

Completion of the merger is not subject to a financing condition but is subject to the accuracy of the representations and warranties, performance of the covenants and other agreements included in the Merger Agreement and customary closing conditions for a transaction of this type, including regulatory approvals in the US and India. Assuming satisfaction of those conditions, the Company expects the merger to close by the end of 2020.

I think the action will be in Nasdaq and how the DuckCreek IPO plays out in the next few weeks. DuckCreek current valuation is $2.8 billion, and if it increases further to say $ 3.5 (just for argument sake), Majesco’s valuation will look dirt cheap at $710 million (approx 20 % ) with more or less same capabilities.

Additionally, if you are a PE player, Majesco offers unique capabilities and ready to roll, profit-making platform that can be accelerated further going ahead. I see the current bidding war has a lot of legs and I will be surprised if this is the last revised offer on the table for the investor of Majesco Limited.