Thanks @cabunny for initiating the thread. You have covered most of the important points.

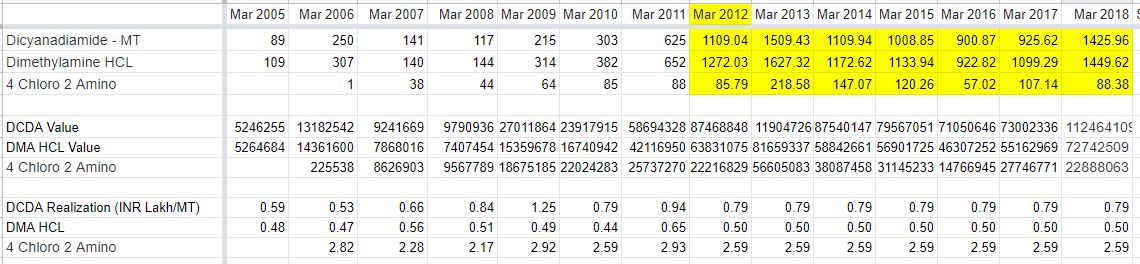

My primary reason for investing in Balaji Amines was the fact that it was the market leader in DMA HCL, key intermediate for Metformin.

| (in MT) | Production Capacities | |

|---|---|---|

| Aarti | 14400 | 20.06% |

| Granules | 14000 | 19.50% |

| USV | 10100 | 14.07% |

| Wanbury | 9000 | 12.53% |

| Harman Finochem | 6000 | 8.36% |

| Smruthi Organics | 4800 | 6.69% |

| Farmhispania | 4000 | 5.57% |

| IOL CP | 4000 | 5.57% |

| Vistin Pharma | 3100 | 4.32% |

| Sohan Healthcare | 2400 | 3.34% |

| Total | 71800 |

Above table indicates the Supply side capacity while actual global consumption would be around 40,000 MT.

Of the 71,800 MT not all of it would be under FDA/EMA regulatory compliance.

The major trigger for me looking into Auro Labs was the fact that Metformin contribution is >90% of revenues, which makes it a pure play unlike Aarti Drugs/Granules.

Like you, the key trigger to initiate position was the fact that they are going for a massive capacity expansion. The capex cost seems reasonable when compared to IOL CP capex for metformin.

Greenfield capex of 2880 MTPA: INR 10 Crores

Incremental capex from 3000 to 4000 MTPA: INR 2.4 crores

Major risk is 2 fold:

- Failure to execute on capex plan

- Change in capex plans to shift away from Metformin to other APIs against the original proposed plan

Some of the analysis I had done earlier:

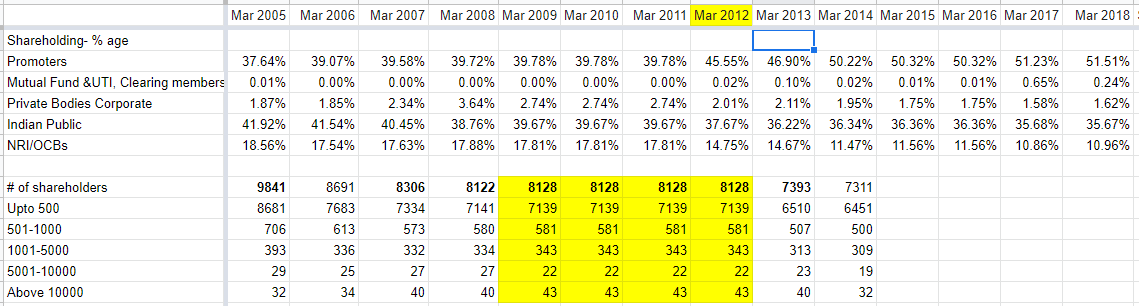

Steady accumulation by Promoters:

Key question to ask from mgmt:

- What is the insight they have about Metformin that made them go for this big capex relative to their existing capacity?

- Do they have assured offtake agreements in place which gives them the confidence?

Received huge help from @hrfacebuk who tipped me off on the capex plans.

Disc: Have been invested since late Jan. Makes up 20% of my portfolio. Not a SEBI registered advisor/analyst. Not a buy/sell/hold reco. Please do your own due diligence.