Source: Business Standard

Disclosure : Invested

2 Likes

Marcellus “Kings of Capital” Webinar with Sanjay Agarwal, MD & CEO of AU Small Finance Bank:

4 Likes

What is ONAN pool in Au bank? Why they are reporting even 1+dpd accounts as NPA

I was exploring an investment opportunity but after reading through thread i am bit concerned because of promoter selling and auditor resignation. Moreover NPA’s in the last quarter is highest ever. I am still trying to understand why this bank commands such high valuation with P/BV of 7, Prices/Sales of 6.2 , PE of 30 compared to Bandhan bank 3.1, 3.85 and 21 respectively.

While i really like the way they have grown sales and profits I believe there is lot of mystery around corporate governance but looks like FII’s and DII’s aren’t worried much. They have been increasing stake QoQ while retailers keep selling.

Can some one through some light on promoter sell off and the auditor resignation. Did management provide satisfactory answer?

Disclosure: Tracking

1 Like

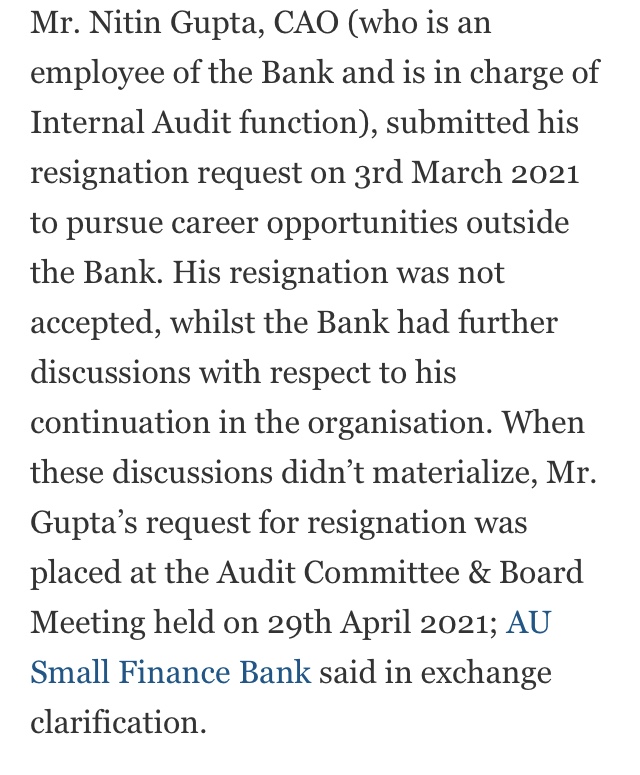

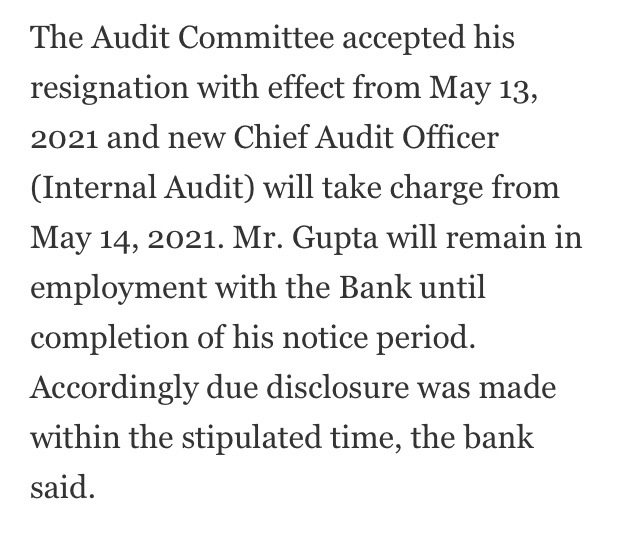

Regarding resignation, According to bank, this is internal auditor, he submitted his resignation but firm didn’t accept his resignation since they wish to retain him. But he insisted on moving, firm hired new guy and accepted his resignation and reported post accepting his resignation. He is still in firm serving notice period.

I personally find no red flag here as he is internal auditor.

Disc: invested, may be biased

1 Like

Au small finance bank is a great company. If you want to know some business updates of this bank for Q4&FY21. Then check out this link - https://stockanalyst1.blogspot.com/2021/07/au-small-finance-bank-share-q4-business.html

1 Like

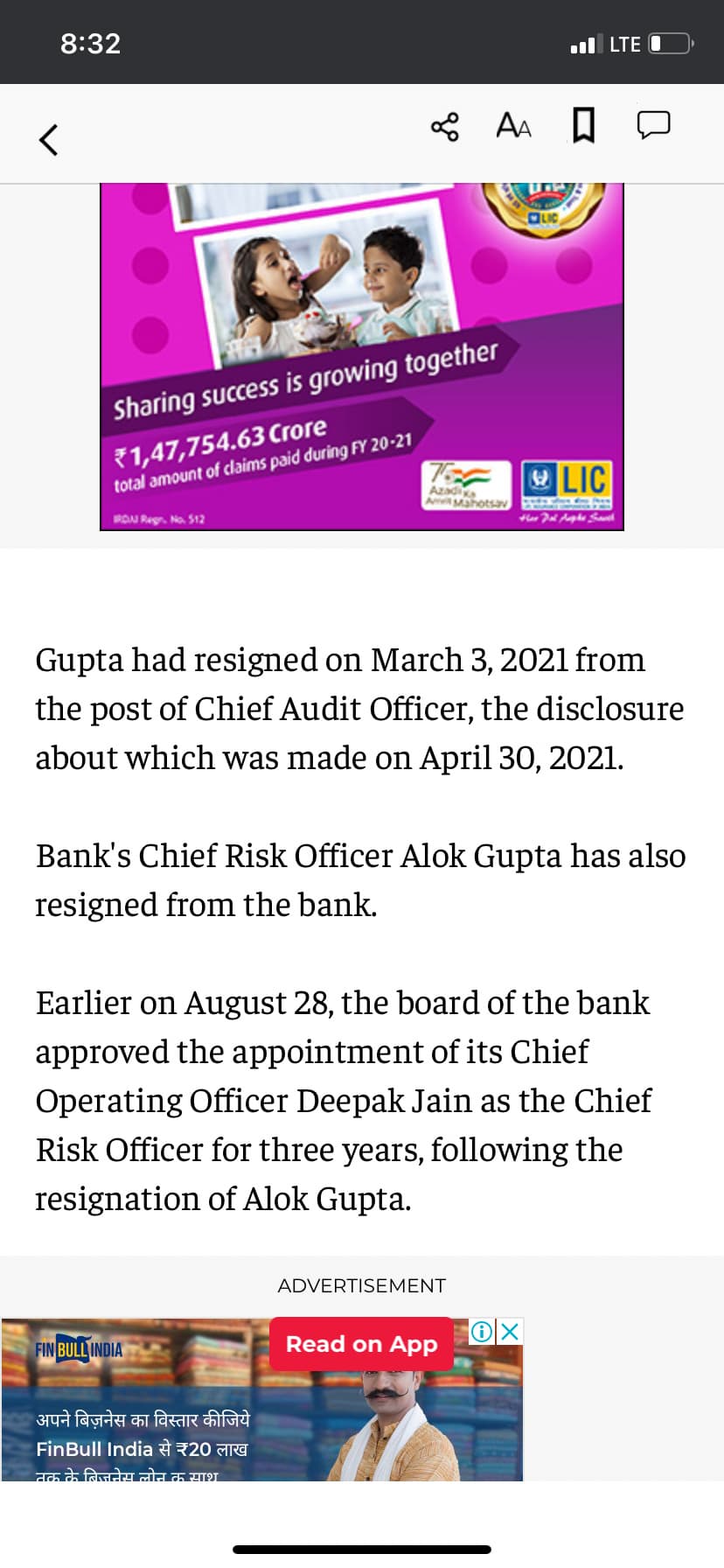

Sonia Shenoy tweets - “Alok Gupta, Chief Risk Offer, resigns citing personal reasons

Deepak Jain to take over as CRO from 1st Sept’21 for 3 years

this is the 2nd exit in last couple of months, post chief audit officer leaving his post on 14th May’21”

What does the community make of this ? I was mostly invested here because of the growth story, at the risk of some of the growth coming at the cost of some lapses in asset quality, but what does one make of multiple resignations happening in a short period of time ? Is this a normal occurence in aggressive banks ?

5 Likes

If you are refering to this, I don’t see anything that jumps out as a red flag unless I am missing something.

Talking to a businessman in Raipur who shifted his current account from AU SFB to Kotak for the simple troubles he had due to attrition in the bank. Resolving a simple issue took months as 2 officers replaced the first and all three had to brought to speed about the issue. Relationships with bank officials maybe a thing of the past but such employee turnover has immense economic and social costs. Moreover reporting such issues after two months ! (March 3 he resigned and April 30 the disclosure was made). Red flags in banking sector from my naive experience are subtle until you bleed red all over.

2 Likes

Talking to a businessman in Raipur who shifted his current account from AU SFB to Kotak for the simple troubles he had due to attrition in the bank. Resolving a simple issue took months as 2 officers replaced the first and all three had to brought to speed about the issue. Relationships with bank officials maybe a thing of the past but such employee turnover has immense economic and social costs. Moreover reporting such issues after two months ! (March 3 he resigned and April 30 the disclosure was made). Red flags in banking sector from my naive experience are subtle until you bleed red all over. Must scuttlebutt more widely.

4 Likes

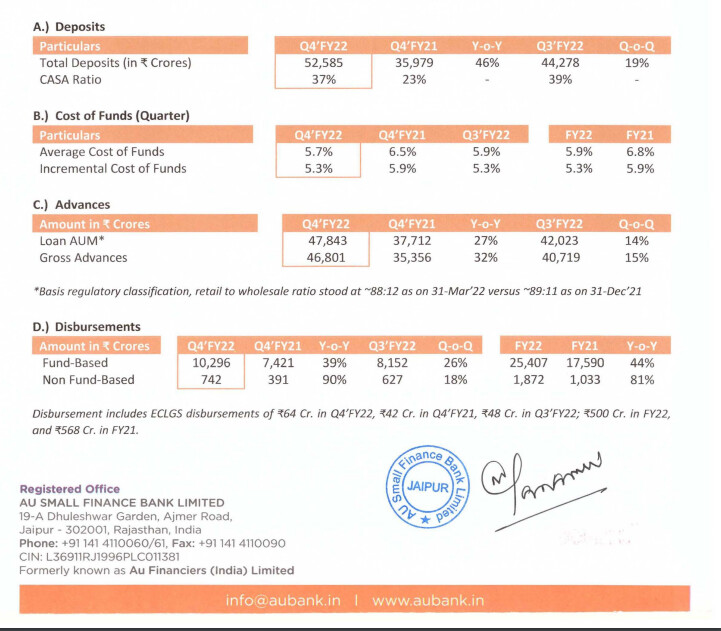

Q4FY22-investor-presentation.pdf (3.6 MB)

Has anyone been tracking this bank?

Above link is behind payment wall.

Useful info about whats going on.

Disclosure: invested.

The bank has stated weeks ago that it is applying for universal banking license. Why isn’t the markets reacting to that in a positive way?

Applying and getting a license are 2 very different things.

4 Likes

FY25 Q4 Concall points:

- The bank experienced strong deposit growth, with an underlying growth of 30% plus after replacing higher-cost Fincare deposits.

- Significant improvement in branch profitability, with 49% of branches becoming profitable in Q4 compared to 25% a year ago.

- The cost-to-income ratio reduced from 64% in FY24 to 57% in FY25

- Plans to expand its presence by opening 70 to 80 new branches in top cities and enabling 75 existing asset centers to take deposits in FY26.

- The unsecured book, particularly microfinance, faced deleveraging, with the MFI book declining by 17% YoY, 10% QoQ

- Almost 100% of Q4 disbursements under the CGFMU scheme raised overall portfolio coverage to ~36%, going forward coverage on the overall book will increase to more than 75%.

- The credit card business expects to break even by FY 26-27 and start contributing positively from FY 27-28 onwards.

- Anticipates pressure on NIMs in the near term, although credit costs are expected to reduce.

- Credit‑card credit cost expected to fall from ~11-12% this year to ~6-7% in FY26, while MFI charge‑offs should ease from ~11% to ~3-3.5%.

- Issuance of credit card will ramp from ~10,000 cards/month to ~20,000 cards/month post‑September

- Maintain it’s unsecured portfolio, with unsecured not exceeding 15% and MFI not exceeding 10% of the overall book in the next few years.

- Over the medium to long term, they can sustainably deliver an ROA of around 1.8% with business growth of 2x to 2.5x of nominal GDP

Management didn’t give any kind of guidance.

Disc: Tracking

8 Likes

Disc- not invested

4 Likes