The Atul Auto CFO says the Rs. 115 cr will be used for repaying debt, working capital requirements and general corporate purposes. There’s something more to this?

I went back to the last upcycle from 2012-2015. A few observations:

1. The stock was rising exponentially during this period.

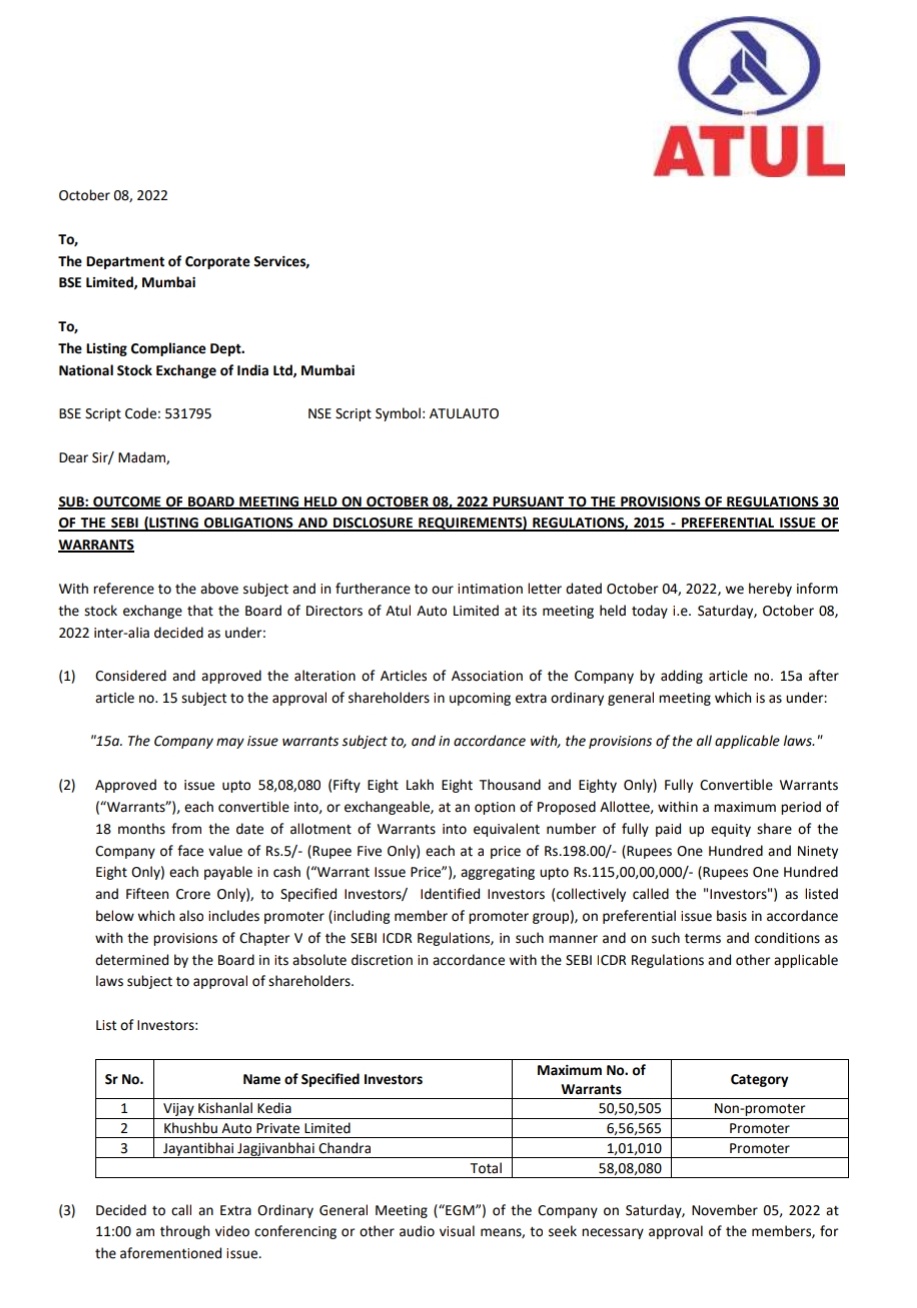

2. Mr. Vijay Kedia’s stake in FY 13, FY 14 and FY 15 was 18.86%,16.3%, 1.16% respectively.

3. Multiple bulk deals in 2013 and 2014 - Mr. Kedia sold shares worth around Rs. 18.5 crores to HDFC MF at Rs. 615 and a lot more shares in the Rs. 360-Rs. 430 range to institutional players like Birla MF, Birla Sun Life MF, Goldman Sachs India Fund. He also sold 1.75 lakh shares at Rs. 260 to Mr. Ramdeo Agrawal and Osag Enterprises (owned by Mr. Ramdeo Agrawal and Mr. Motilal Oswal).

4. In FY 12, promoter holding increased by 1.5% (there was a rights issue at Rs. 30). In FY 13, FY 14 and FY 15, promoter holding reduced by 4.2%, 1.55% and 2.39%. Promoters sold shares worth around Rs. 21.7 crores through bulk deal, most of which at Rs. 610 to institutional players - Goldman Sachs India, Goldman Sachs Asset Mgmt. and India Investment Partners.

5. Noticeable change in annual report from FY 10 to FY 13: More attractive to look at - colourful, better design and font, more pictures, more details about the company and bullish commentary by management.

6. Many interviews by Mr. Kedia (in the capacity of Director of Atul Auto) on the company and bullish outlook.

7. Gave this interview in the capacity of an investor during the time he was selling Atul Auto shares: Management of a company my first priority before making investment: Vijay Kedia, Kedia Securities - The Economic Times

I found this old comment by @ashwinidamani in this VP thread instructive:

"A. How many people know Ramdeo Agarwal vs. Vijay Kedia (purely meaning who commands more glamour following and publicity)

B. By transferring 5% of his shares he has suddenly attracted more visibility/publicity for the stock

C. By transferring 5% of his shares he has attracted more value for every balance share which he holds.

Net Net he has created more value by transferring merely 5% of his holding. Isn’t it a win-win deal for him.

You need to unlock value someway–he is doing it the smart way."

Based on the above, could these be some possibilities behind Mr. Kedia looking to increase his stake to almost 20%?

1. Something similar to the 2012-2015 cycle repeats as he converts warrants in the coming months? This article from Business Standard mentions: “One possibility could be contract manufacturing for an upcoming electric 3-W player domestically.” Is he timing it right to ride the coming tailwinds for Atul Auto?

2. Sell out to a strategic investor and get a great exit or something along these lines?