FY23 sales were 50Cr. Management has a really ambitious plan of reaching 1000 Cr in 7 years. At full capacity the company can make 65-70 Cr. Therefore, the management would have to put up significant capex in the coming years to meet its target of 1000 cr. topline.

The bathroom faucets and allied items business segment is expected to make 100 cr. at full capacity. Management’s ability to scale up this segment is a key variable to watch going forward.

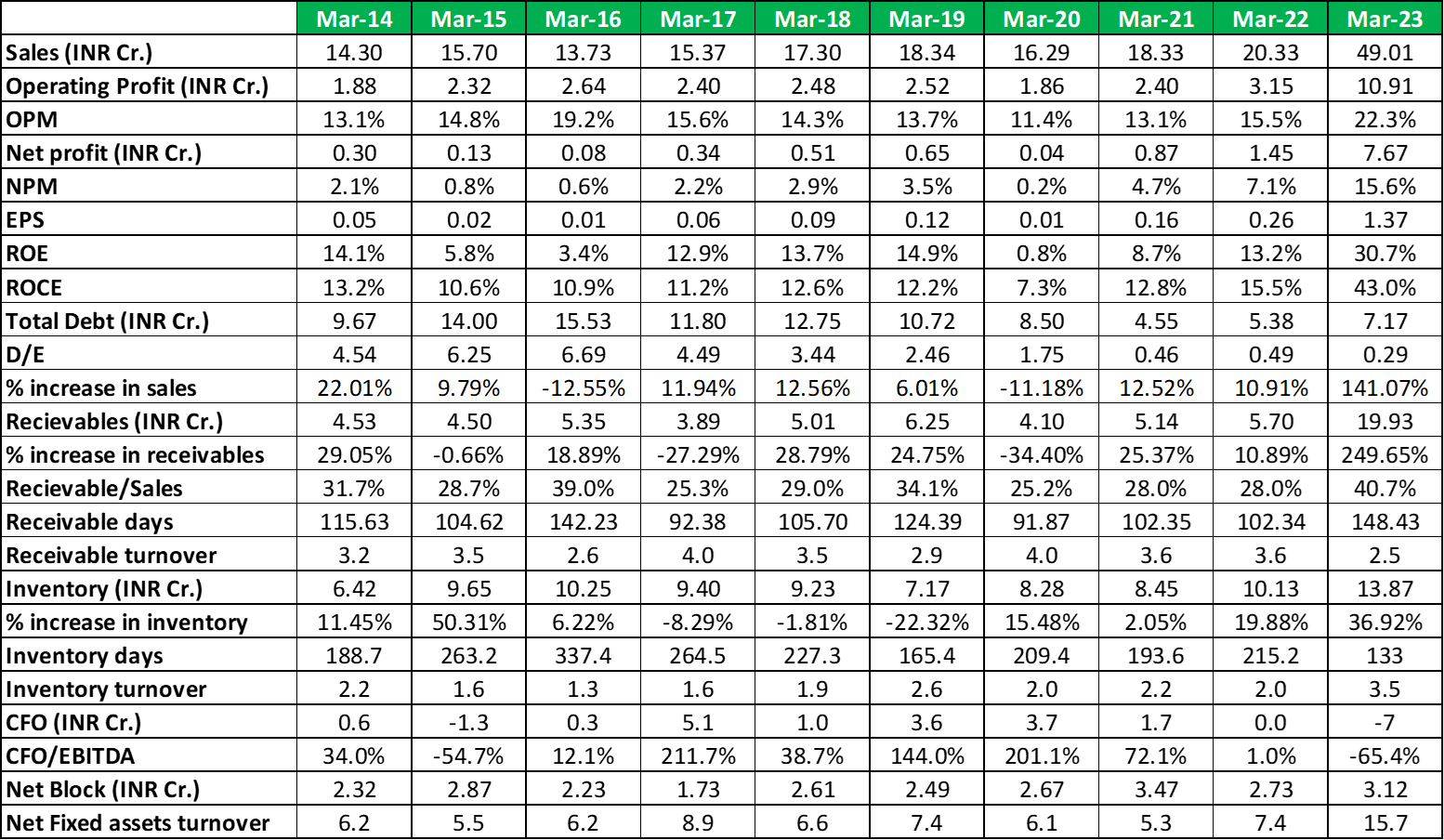

Receivables have become 3.5 times the previous year. Post a short recovery receivable days and receivables as a % of sales have increased.

CFO has become negative while sales, receivables & inventory have increased significantly.

Cumulative 10Yr CFO is also less than cumulative 10Yr PAT.

Deteriorating CFO/EBITDA in the past 3 years, indicate the company is not able to translate its profits into cash profits.

Atam Valves Limited: A leading manufacturer of industrial and plumbing valves.

Wide range of products including gate, globe, check, ball, butterfly valves, steam traps, boiler mounting, and accessories.

Key industries served: oil and gas, refineries, petrochemicals, chemicals, pharmaceuticals, marine, mining, water and wastewater, textile, sugar, and HVAC.

2. Company Structure

Company’s facilities span 63,000 square feet.

Three foundry shops for different materials.

35-year-old entity with three generations working towards becoming a leader in the industry.

500 SKUs, 300 clients, and 500 employees.

Strong pan-India dealer network with plans to expand to 1,000 dealers.

Key clients mentioned.

3. International Presence

Current international presence in South Africa, USA, UK, and Indonesia.

Expansion plans in the United Arab Emirates, Saudi Arabia, Tanzania, Kenya, and Russia.

4. Revenue Breakdown

Revenue contribution from different business verticals: Boilers (30%), Domestic (40%), Hydro projects (10%), Other products (20%).

5. Expansion Announcement

Introduction of a new business vertical: bathroom faucets and allied items.

Planned investment of INR 30 crores in the first or second quarter of FY 2023-24.

Expectation of a positive impact on overall revenue and growth.

6. Financial Performance

Q4 FY23: Revenues of INR 19.82 crores (193% increase), EBITDA of INR 4.50 crores (369% increase), PAT of INR 3.30 crores (432% increase).

FY23: Revenues of INR 49.25 crores (141% increase), EBITDA of INR 11.16 crores (246% increase), PAT of INR 7.67 crores (460% increase).

7. Bathroom Fittings Launch

Planned launch of bathroom fittings range in the first and fourth quarters of FY 2023-24.

8. Margins and Bill Receivable Trends

Sustainable margins due to network expansion and product range growth.

Constant increase in bill receivables YoY, typically 90 to 120 days for payments.

Plans to introduce cash and turnover discounts to encourage early payments and reduce bill receivable days.

9. Top Customers and Business Concentration

Top 10 customers collectively contribute 40%-50% of total revenue.

Faucet business managed as a separate entity with dedicated network and sales teams, mitigating the risk of concentration in the core valve business.

10. Turnover and Seasonality

Anticipation of INR 25 crores in revenue from the new business.

Last quarter traditionally the best due to customer demand fulfillment.

11. Property, Plant, and Equipment

Concern regarding the high ratio of property, plant, and equipment to turnover.

Assurance that almost everything is manufactured in-house.

12. Working Capital Cycle and Cash Flow

Plans to improve working capital cycle with cash discount schemes and turnover discounts.

13. Expansion Plan for Bathroom Fittings

INR 30 crores to be spent on the new factory with trading initially and an in-house facility ready by the end of the third quarter.

Source of funds: Equity.

14. Top Line Guidance and New Business Capacity Utilization

Anticipating 25% revenue growth year-on-year.

INR 30 crores capex expected to generate up to INR 100 crores at 100% capacity utilization, approximately three to four times asset utilization.

15. Margins Profile

Expected margin profile around 15% to 20% at the EBITDA level.

16. OEM Business

Initial focus on selling the own brand in the new segment, potential consideration of OEMs.

17. Expansion Plans for Existing Facility

Consideration of expansion plans for the existing facility.

18. Unorganized Market in Valve Business

Unorganized market significant, with numerous regional manufacturers.

Atam Valves’ market share in the organized market around 5% to 6% in India.

19. Contribution of Exhibitions

Participation in exhibitions contributes to showcasing products and connecting with potential customers, particularly in the boiler manufacturing industry.

20. Product Pipeline and Revenue Potential

Ongoing product innovation in the valve business, with a focus on new products for nuclear power projects.

Faucet business is expected to have a higher revenue potential at full capacity utilization compared to the valve business.

21. Future Vision

Aspires to become the biggest brand known all over India with a presence in major cities, aiming for a revenue target of INR 1,000 crores by 2030.

22. Strategic Move into Faucet Business

Decision to enter the faucet business led by the third generation.

Faucets are considered more mass-market and known among the masses.

Aim to expand the distribution network and take advantage of the prominent growth in the faucet business.

23. Equity Funding for New Business

Considering preferential equity funding for the new business.

24. Reasons for Sales Growth

Sales growth attributed to the expansion of the sales network, increased salespeople.

Introduction of new products, including stainless steel pipe fittings and high-pressure valves.

Enhanced business relationships with existing clients contributed to sales growth.

Management team, if you go through the investor presentation, as of Aug 23, it looked like the family members mostly run the business, while yes, an owner-operator model is good, the management looks like it lacks the drive and probably the capacity of delivering on their lofty expectations.

Their entry into highly competitive B2C bathroom fittings segments seems like a distraction from their core competency. Seems like family decision to give next generation some experience in new area, but at the cost of minority shareholders. So exited completely post last concall

Delays caused by MSME norms and 45-day payment system, resulting in held-back orders.

Optimistic outlook for Q1 FY '25 with anticipated improved performance from pending orders.

Impact of MSME conditions notable, affecting credit periods and leading to order hold-ups.

EBITDA margin dip for FY '24 attributed to increased expenditure on exhibitions and expansion efforts.

FY '25 margin guidance aims to maintain existing margin with slight improvement, expected range between 20% to 25%.

Market Update and Inventory Status:

Pursuing entry into Saudi and U.S. markets through API certification.

Inventory: approximately 10 crore in finished products, remainder in work-in-progress and raw materials. Anticipating 70% liquidation in Q1 FY '25 post MSME resolution.

Capacity and Expenses:

Current capacity: 96,000 pieces per day, 85% utilized.

30% increase in employee expenses due to expansion efforts.

Delay in CAPEX execution for bathroom faucets due to API focus.

Initial plan to import faucets from China, gradual utilization of CAPEX as market develops.

API Certification and Orders:

API compliance expected in Q1, certification by August/September.

Early-stage talks ongoing for $2 million orders. Anticipate orders upon API compliance.

Collaborating with Canadian partners for API products.

Competitors and Market Positioning:

Competitors in API-related valves include Parveen Industries, Oswal Industries, and Hawa Valves, with revenues ranging from 400 to 700 crore.

ATAM is relatively new in this segment, aiming for significant growth in the next six to seven years.

Competitors in Existing Product Range:

Rotovalve and Centro Valves are competitors in plumbing and firefighting markets.

Rotovalve’s revenue exceeds 300 crore, while Centro Valves’ revenue is around 100 crore.

Export Security:

ATAM Valves does not currently utilize ECGC for export security.

Most exports are on an advanced payment basis, but ECGC may be considered as exports grow.

Impact of MSME Issues on Revenue Projection:

Initial revenue projection of 80 crore for FY '24 included sales of bathroom faucets, which were deferred due to focus on API valves.

Unforeseen MSME issues emerged in late February, leading to a shortfall in revenue.

Expectation of liquidating 70% of finished stock in Q1 to address the revenue shortfall.

Revenue Forecast for Q1 and MSME Issue Resolution:

Forecast for Q1 revenue is approximately 7 crore, aiming to compensate for the Q4 shortfall.

MSME issue resolution expected by the end of Q1, following recent comments from the Finance Minister indicating a potential adjustment period.

Current Order Book and FY '25 Guidance:

Current order book stands at 25 crore, with projects on hold due to market uncertainties.

FY '25 revenue target set at 70 to 75 crore.

Long-Term Revenue Growth and Market Expansion:

Confidence in increasing revenues twentyfold over the next five years attributed to entering the API valves market for oil and refinery industries.

Expansion plans include manufacturing larger valve sizes, aiming to capitalize on a sizable market opportunity.

Export Contribution and Cumulative CAPEX:

Anticipation of exports contributing at least 50% to the projected 1,000 crore topline over five years.

Cumulative CAPEX estimated at around 40 crore for machinery and equipment required for expansion.

Faucet Division Strategy and Revenue Expectations:

Faucet foray currently on hold to focus on building a brand in the plumbing valve range.

No expectation for the faucet division to contribute to the projected 1,000 crore topline by 2030.

Operating Margin and Profit Expectations:

Anticipation of improving operating margins as scale of operations increases, particularly in the larger valve sizes segment.

Expectation of increasing EBITDA and PAT with entry into the larger valve sizes market.

Business Model and Tender Business:

Primarily engaged in direct client business and dealer network, with no involvement in tender business.

No current plans to enter the PSU or oil marketing company markets due to regulatory approval requirements.

Timeline for Faucet Business:

Skeptical about timeline due to API focus.

Importing from China to understand market before manufacturing.

Decision expected by Quarter 4, possibly to begin in the future.